The great rotation trade has a problem: everyone already bought it

Capital moved from AI to value months ago—now what?

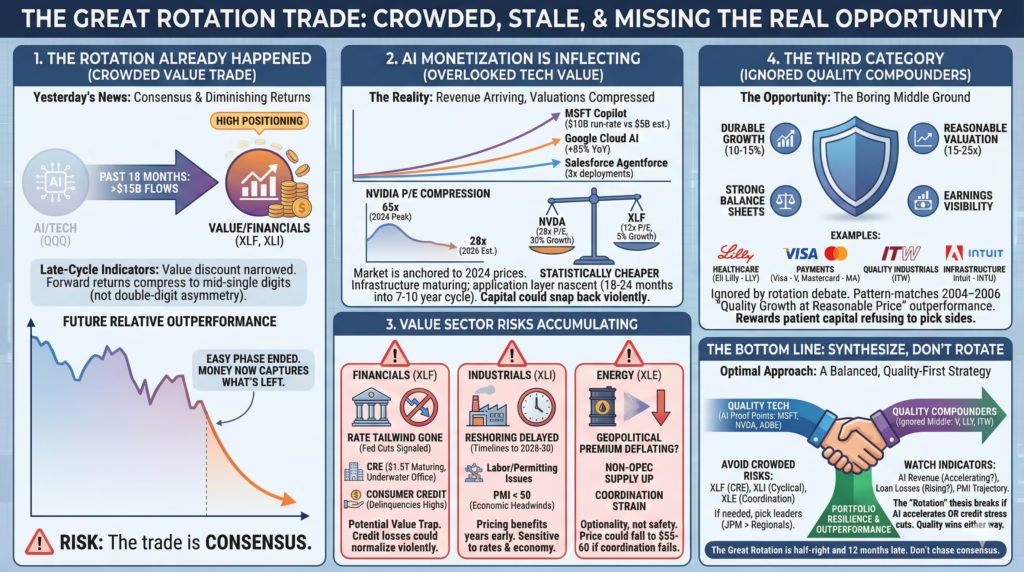

The pitch

The rotation from AI to value isn’t beginning—it’s already consensus. Over $15B flowed into financial ETFs over the past 18 months. Hedge fund positioning in cyclicals sits at multi-year highs. The real opportunity lies not in picking sides but in recognizing that AI monetization is accelerating faster than skeptics admit while value sectors face backward-looking tailwinds that may already be priced.

Smart capital should target the synthesis: quality compounders ignored by both camps and AI application layers where the next leg of value creation happens.

The friction

Financials face $1.5T in commercial real estate loans maturing through 2027 with 30%+ of office properties underwater. Consumer credit delinquencies? Twelve-year highs. Industrials are pricing reshoring benefits that won’t hit earnings until 2027-2029 based on actual project timelines. Energy’s “supply discipline” thesis depends on OPEC+ coordination that’s already fraying—UAE and Kazakhstan are exceeding quotas while non-OPEC supply grows 1.5M barrels per day annually.

Here’s what the rotation narrative gets wrong and right.

The rotation trade is no longer early innings

Wall Street loves declaring the start of something that already happened.

XLF saw massive inflows throughout 2024-2025. Industrial ETFs trade at 3-year high positioning. The “value is under-owned” thesis was accurate in late 2022—it’s stale in December 2025. When every strategist publishes the same “Great Rotation” deck, the asymmetric upside has been arbitraged away.

Look at the data: Russell 1000 Value’s discount to Growth has narrowed substantially from its 2023 peak. Sell-side upgrade ratios for financials versus technology have flipped positive for six consecutive quarters. These are late-cycle positioning indicators, not early-cycle entry signals. The money that moved from QQQ to XLF in early 2024 captured 20-30% relative outperformance. Money moving now captures whatever’s left.

This doesn’t mean value collapses. It means forward returns compress to mid-single digits from here rather than the double-digit asymmetry the thesis promises. The “easy money” phase of any rotation ends precisely when it becomes consensus. Watch for three consecutive weeks of outflows from XLF and XLI as the signal that even the rotation trade has grown crowded enough to reverse.

AI monetization is inflecting while everyone looks away

The contrarian bullish case for technology isn’t that AI hype returns—it’s that AI revenue is actually arriving while the market remains anchored to 2023-2024 skepticism. Microsoft’s Copilot hit a $10B revenue run-rate in Q3 2025 versus $5B expectations. Google Cloud’s AI-specific revenue grew 85% year-over-year. Salesforce’s Agentforce deployments came in 3x above guidance.

The market treats AI as “priced for perfection,” but NVIDIA’s forward P/E compressed from 65x at the 2024 peak to roughly 28x on 2026 estimates. That multiple compression already happened.

Here’s the thing—NVIDIA at 25-28x forward earnings with 30% growth is statistically cheaper than XLF at 12x with 5% growth when you adjust for quality and duration. The rotation narrative forces investors to mentally categorize NVIDIA as “expensive AI” based on prices from 18 months ago. Which, fair enough, was true then. It’s not true now.

More critically, the infrastructure phase of AI is maturing while the application layer remains nascent. This reminds me of the internet buildout in 1999-2000—everyone focused on the pipes while the real value emerged in applications years later. Enterprise AI adoption cycles typically run 7-10 years; we’re 18-24 months in. Agentic AI, autonomous systems, and vertical software represent the next leg of value creation—and this layer is under-hyped relative to chips and hyperscaler capex. If 2026-2027 shows accelerating AI revenue rather than just spending, capital snaps back to growth with violence.

Watch Q1-Q2 2026 hyperscaler earnings for AI revenue disclosures, enterprise attach rates at Adobe and ServiceNow, and robotics deployment metrics.

Financials’ rate tailwind is a rearview mirror

Net interest margin expansion is a rate-rise phenomenon, not a rate-plateau phenomenon. Major banks already captured 150-200 basis points of NIM expansion from 2022-2024. Further expansion requires rates to go higher—which isn’t the base case with the Fed signaling cuts in 2026. The “financials benefit from higher rates” thesis describes what happened, not what happens next.

The risks are accumulating. Commercial real estate presents a slow-motion problem: $1.5T in loans maturing through 2027, with vacancy rates in office above 20% nationally and 30%+ of properties underwater. Consumer credit delinquencies hit 12-year highs while auto loan serious delinquencies reached records. The excess savings buffer is exhausted for the bottom 60% of households. Deposit competition intensified as money market yields continue pulling funds away from bank accounts.

The sector trades at 12x earnings, which looks cheap until you model credit losses normalizing. Loan loss provisions would need to increase 40-60% from current levels to match pre-2020 historical averages. If unemployment rises even modestly from 4.1% to 5%… well, consumer credit losses could spike 50-70%.

Financials may be a value trap masquerading as a value opportunity. JPM at 13x is probably fine. Regional banks with heavy CRE exposure warrant far more skepticism.

Reshoring benefits are real but delayed and narrow

The gap between announced reshoring investment and actual capital deployment is enormous. Over $400B in CHIPS Act and IRA commitments have been announced, but only 35% of semiconductor fab projects have broken ground. Construction timelines extend to 2028-2030 for most facilities. Labor shortages and permitting delays remain systemic constraints.

Even when spending flows, benefits concentrate narrowly. Construction and engineering firms capture 60-70% of near-term spending. Equipment manufacturers and industrial suppliers see benefits with 3-5 year lags. Industrial ETFs pricing broad tailwinds from narrow, delayed deployment will likely disappoint in 2026.

The cyclical reality makes this worse. Manufacturing PMI spent most of 2025 below 50, indicating contraction. Industrials carry sensitivity to both economic activity and interest rates—in a slowdown scenario, they suffer on both fronts. The “reshoring + higher rates = buy industrials” equation assumes policy spending arrives faster than economic headwinds. History suggests otherwise.

Track actual capex deployment versus announced figures through company disclosures. The lag will likely frustrate industrial bulls for another 18-24 months.

Energy’s geopolitical premium could deflate

Energy equities have traded with an embedded “geopolitical risk premium” since 2022. But insurance premia decay when the insured event doesn’t occur. If 2026 brings de-escalation in Ukraine under Trump administration pressure, continued Saudi-Iran détente, and OPEC+ coordination continuing to fray, that premium deflates rapidly.

Non-OPEC supply growth creates structural pressure. Guyana, Brazil, and the Permian add 1-1.5M barrels per day annually. UAE has systematically exceeded quotas. Kazakhstan’s Tengiz field brings 260k barrels per day of new supply online. The cartel’s pricing power depends on coordination that shows increasing strain.

The market prices Brent at $70-75 while marginal cost of US shale production runs $40-50. If coordination fails, oil could fall to $55-60.

Energy’s “torque” works in both directions. A global GDP slowdown combined with normalized geopolitics could trigger 30-40% declines in exploration and production equities. The sector offers optionality, not safety. Position sizing should reflect that energy is a tactical trade dependent on geopolitical risk—not a strategic rotation destination with durable tailwinds.

The barbell compression scenario nobody’s discussing

Pattern-match to 2004-2006, when both the tech recovery and value rotation simultaneously disappointed while quality growth at reasonable price dramatically outperformed. Crowded positioning in both AI mega-caps and value cyclicals creates a setup where marginal sellers exist on both sides. Capital doesn’t rotate between them—it flows to a third category.

That third category includes companies with 10-15% durable revenue growth, 15-25x valuations, strong balance sheets, and earnings visibility: healthcare leaders like Eli Lilly, payment networks like Visa and Mastercard, quality industrials like Illinois Tool Works, and infrastructure software like Adobe and Intuit. These get ignored in the rotation debate because they fit neither bucket.

Look, the historical base rate for narrow “theme versus theme” debates resolving in favor of a third option is surprisingly high. The 2000-2002 cycle ended not with tech recovery or value rotation but with dividend aristocrats dominating 2003-2007. The stocks that outperform may be neither AI darlings nor value turnarounds but boring compounders both camps neglect while debating rotation.

This frustrates bulls and bears alike. And rewards patient capital that refuses to pick sides in a crowded trade.

The bottom line

The Great Rotation thesis is half-right and 12 months late. Value sectors already absorbed significant inflows; financials face credit deterioration that challenges the NIM narrative; industrials are pricing reshoring benefits years before they arrive. AI monetization accelerates while investors remain anchored to 2024 skepticism—and multiple compression has already made quality tech far cheaper than the “priced for perfection” narrative suggests.

The rotation trade itself became consensus. Positioning for it now captures diminishing returns.

For a 5-year growth investor, the optimal approach is a barbell: maintain core positions in quality technology where AI revenue proof points are emerging (Microsoft at 30x, Adobe at 24x, even NVIDIA at 28x with 30% growth), while selectively adding quality compounders ignored in the rotation debate (Visa at 26x, Lilly at 35x justified by pipeline, ITW at 22x). Avoid the crowded expressions of rotation—XLF broad exposure carries CRE risk; XLI carries cyclical risk before reshoring benefits arrive; XLE carries coordination-failure risk.

If you must own financials, stick with JPM and BAC at current prices rather than regionals. If you want industrial exposure, wait for manufacturing PMI to cross above 50 for three consecutive months.

Key metrics to monitor quarterly: AI revenue disclosures from hyperscalers (need 30%+ growth to sustain multiples), loan loss provision trends at major banks (any upward revisions signal credit stress), and manufacturing PMI trajectory. The thesis that value beats growth from here breaks if AI monetization accelerates faster than expected—watch Copilot and Agentforce adoption rates as leading indicators. The thesis that growth reasserts dominance breaks if credit stress forces Fed cuts that reflate everything.

In either scenario, quality compounders in the middle outperform. Don’t rotate—synthesize.