$LITE may control the one chokepoint Jensen Huang can’t ignore

When NVIDIA’s CEO publicly complains about photonics capacity, he’s telling you which suppliers have pricing power—and which ones he’s coming for

The pitch

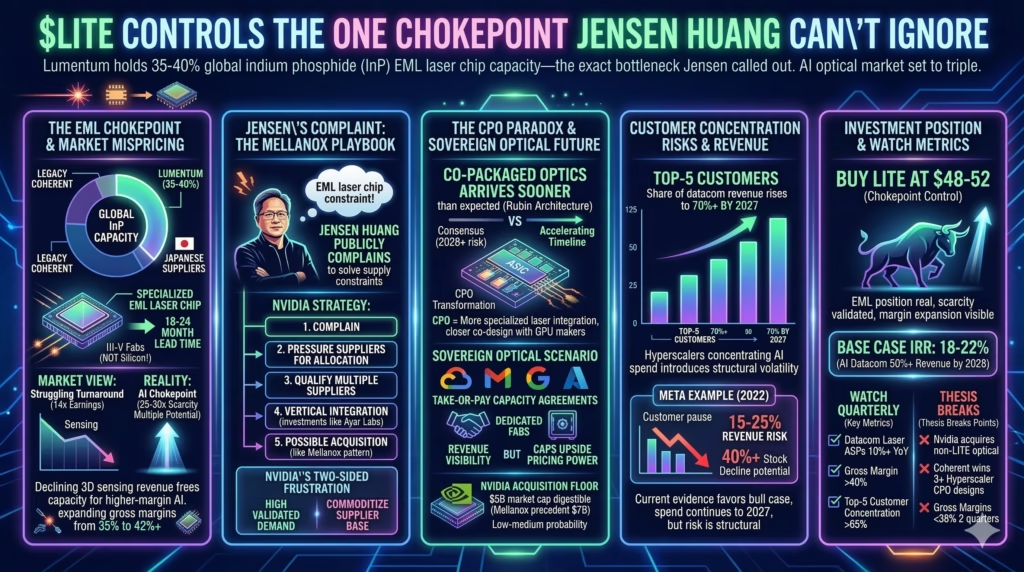

Lumentum controls roughly 35-40% of global indium phosphide EML laser chip capacity. That’s the exact bottleneck Jensen Huang called out—not “optical components” broadly, but this specific constraint. The stock trades at approximately 14x forward earnings while the AI datacenter optical TAM is set to triple over the next three years.

The market is pricing LITE as a struggling telecom turnaround. It’s actually a chokepoint supplier in the hottest infrastructure buildout in decades.

Here’s what’s being missed: declining 3D sensing revenue looks like a headwind, but the mix shift is expanding gross margins from 35% to 42%+ while freeing resources for higher-margin AI opportunities. The “problem” is actually the solution.

The friction

Jensen’s public complaint is also a warning shot. NVIDIA has never flagged a supplier constraint without simultaneously moving to solve it through multi-sourcing, vertical integration, or acquisition. That’s just how they operate. Coherent’s integrated platform—spanning lasers, transceivers, and silicon photonics—offers full-stack solutions that LITE cannot match as a pure component supplier. The maximum pricing power window may be 18-24 months before capacity additions and co-packaged optics transitions compress the opportunity.

Here’s what the numbers actually reveal.

The chokepoint nobody is pricing correctly

The market treats LITE as one of several optical suppliers benefiting from AI tailwinds. This fundamentally misreads the supply chain.

The constraint Jensen referenced isn’t transceivers broadly—it’s specifically indium phosphide EML laser chips, which cannot be manufactured on standard silicon fabs. These require specialized III-V semiconductor facilities with 18-24 month lead times for new capacity. Lumentum’s only competitors with meaningful EML capacity are Coherent’s legacy II-VI assets and a handful of Japanese suppliers (Sumitomo, Mitsubishi) who face their own constraints.

Chokepoint suppliers in constrained markets historically command 25-30x earnings during scarcity periods. LITE trades at roughly half that. If quarterly results show datacom laser ASPs rising 15%+ year-over-year while volumes also grow, the chokepoint thesis validates and the multiple should re-rate accordingly. The absence of major competitor capacity announcements with 2027+ online dates would extend this scarcity window further than current models assume.

The bear case though: customer concentration is accelerating dangerously. As AI spend concentrates among five to seven hyperscalers, LITE’s top-five customers could reach 70%+ of datacom revenue by 2027. A single customer pause—as Meta demonstrated in 2022—creates 15-25% revenue risk and potential 40%+ stock decline. Diversification across telecom carriers historically provided stability; datacenter concentration introduces earnings volatility that may justify a lower multiple even with higher growth.

Current evidence favors the bull case. LITE’s EML position is genuinely scarce, competitor capacity additions remain 18+ months out, and hyperscaler spend shows no signs of pausing through 2027.

Why Jensen’s public frustration cuts both ways

When has Jensen Huang ever publicly complained about a supplier constraint without telegraphing NVIDIA’s intent to solve it?

This is the Mellanox playbook. NVIDIA identified networking as a constraint, complained publicly, then acquired the solution for $7 billion. The same pattern played out with TSMC (leading to Samsung and Intel diversification efforts) and HBM memory (leading to aggressive multi-sourcing). Jensen calling out photonics publicly means NVIDIA is actively qualifying multiple suppliers, exploring vertical integration through investments like Ayar Labs, and pressuring optical suppliers to prioritize NVIDIA allocations—potentially at margin expense.

The bullish read: LITE sits at the center of validated, explosive demand. The cautious read: NVIDIA is simultaneously working to commoditize its supplier base. Both readings are correct. The investment question is whether LITE can capture enough value in the 18-24 month scarcity window to justify current entry, and whether they can transition to co-packaged optics co-development that maintains relevance beyond pluggable transceivers.

Watch for NVIDIA optical supplier qualification announcements and any NVIDIA investments in or acquisitions of photonics companies. If NVIDIA drops below 20% of LITE’s revenue while hyperscaler direct purchases grow, successful diversification is already occurring—and LITE’s pricing power window may be shorter than the bull case assumes.

The risk is real but timing-dependent. LITE’s maximum pricing power is likely now through late 2027. A 5-year investor should model margin compression in years three through five even as volumes continue growing.

The 3D sensing “headwind” is actually funding the pivot

Apple 3D sensing revenue decline was priced in 18+ months ago. What the market misses is that 3D sensing was a lower margin, higher capital intensity business than optical communications. Its decline is freeing engineering talent, manufacturing capacity, and management attention for higher-margin AI opportunities.

Gross margin expansion from roughly 35% in 2023 to 42%+ projected for fiscal 2026 is substantially driven by this mix shift. The “headwind” is enabling margin expansion.

Additionally, the predictable decline of 3D sensing gave management two-plus years to reorient R&D and capacity toward datacom. They saw this transition coming and prepared for it—unlike competitors caught flat-footed by the AI demand surge. This reminds me a bit of how Intel’s foundry struggles inadvertently positioned TSMC, though that’s probably a different piece entirely. Investors anchored on “declining revenue” metrics miss that earnings and free cash flow profiles are actually improving even as headline revenue stays flat.

The bear case: execution risk is real. Transitioning from consumer electronics cycles to hyperscaler qualification cycles requires different sales motions, engineering capabilities, and customer relationship management. LITE’s historical telecom distribution network may not translate to the concentrated hyperscaler procurement environment. Watch for design win announcements with GPU and switch makers for co-packaged optics applications—these signal successful transition, while their absence signals potential disintermediation.

Gross margin trajectory is the key metric. If LITE maintains 42%+ gross margins while AI datacom grows 40%+ annually, operating leverage emerges that the “turnaround” narrative completely misses.

Co-packaged optics is nearer than models assume

The consensus treats co-packaged optics transition as a 2028+ risk. The timeline is likely accelerated.

NVIDIA’s Rubin architecture and Blackwell Ultra already incorporate optical interconnect designs moving toward CPO, not away from it. Jensen’s public pressure on photonics suppliers is partly about accelerating this transition. The thing is, the market assumes CPO commoditizes optical components when the opposite may be true.

CPO requires even more specialized laser integration, tighter specifications, and closer collaboration with ASIC designers. Suppliers who can co-design lasers with GPU and switch makers gain share; those who can’t become commoditized. LITE’s strategic question is whether they’re positioned as a CPO co-design partner or a legacy pluggable supplier. Recent announcements about silicon photonics integration partnerships suggest they understand this—but execution is unproven.

The bimodal outcome: LITE either becomes a deeper, stickier supplier with higher switching costs, or gets disintermediated as hyperscalers and NVIDIA vertically integrate optical components. The middle ground of “component supplier at arm’s length” is the shrinking outcome. Hiring patterns matter here—are they adding silicon photonics packaging engineers or relying on legacy InP expertise alone?

The hyperscaler sovereign optical scenario

Just as hyperscalers vertically integrated custom silicon—Google TPUs, Amazon Graviton, Microsoft Maia—they will vertically integrate optical components. But not through internal manufacturing. Instead, through long-term capacity agreements with dedicated fabs, similar to how Apple structured its TSMC relationship.

Microsoft, Google, and Amazon each run $50 billion-plus annual capex programs with AI infrastructure consuming 40%+ of that spend. At this scale, optical component availability is existential.

Take-or-pay agreements would transform LITE’s revenue visibility and reduce cyclicality, potentially justifying SaaS-like revenue multiples of 4-6x revenue rather than cyclical hardware multiples of 1-2x. They would also cap upside pricing power during scarcity and create customer concentration risk. Meta’s recent capacity agreements with optical suppliers and Microsoft’s strategic investments in photonics startups suggest this pattern is already emerging.

There’s also a wildcard: NVIDIA acquisition. LITE’s current market cap around $5 billion is digestible for NVIDIA, which acquired Mellanox for $7 billion and carries a $2 trillion-plus market cap. An acquisition at 40-50% premium gives NVIDIA captive optical capacity for NVLink interconnects. Probability is low-medium—NVIDIA’s preference is multi-sourcing rather than full vertical integration outside core compute—but it provides a floor on downside while capping long-term compounding upside.

The bottom line

The EML laser position is real. The capacity scarcity is validated by Jensen’s public comments. Gross margin expansion from mix shift toward AI datacom is already visible in the numbers.

For a 5-year investor, the risk-reward skews bullish: base case IRR of 18-22% as AI datacom grows to 50%+ of revenue by 2028, with acquisition optionality providing downside protection.

Key metrics to monitor quarterly: datacom laser ASPs (need to see 10%+ year-over-year growth), gross margin (must stay above 40%), and customer concentration (watch if top-five customers exceed 65% of datacom revenue). Design win announcements with NVIDIA or hyperscalers for co-packaged optics applications are the bullish catalyst; their absence by mid-2027… well, that changes the story.

Thesis breaks if: NVIDIA announces a major optical acquisition that isn’t LITE, Coherent wins three-plus hyperscaler co-packaged optics design wins while LITE wins none, or gross margins fall below 38% for two consecutive quarters indicating competitive pricing pressure. The 18-24 month scarcity window is the critical period. LITE needs to convert pricing power into design wins and customer lock-in before capacity additions and CPO transitions reshape the market. That’s the bet.