Iridium (IRDM): The Monopoly the Market Keeps Pricing Like It’s Dying

The only network that works at the poles trades like it’s already obsolete

Why This Little Orbital Oddity Deserves a Second Look

Iridium Communications is one of those businesses that sound made up.

A single company, running the only satellite network that covers every point on Earth — poles included — with its own spectrum, global licenses, inter-satellite links, and long-term government contracts. Roughly $790 million in annual revenue (2023), EBITDA margins north of 75% on service revenue, and free cash flow that’s finally gushing after a $3+ billion constellation rebuild.

And yet the stock trades like a half-broken gadget in a bargain bin.

Starlink headlines, direct-to-phone demos, and a dead Qualcomm deal have pushed Iridium into the market’s penalty box. The narrative is simple and lazy: “Old narrowband player doomed by new broadband kings.” That narrative is also wrong in important ways — and still uncomfortably right in others.

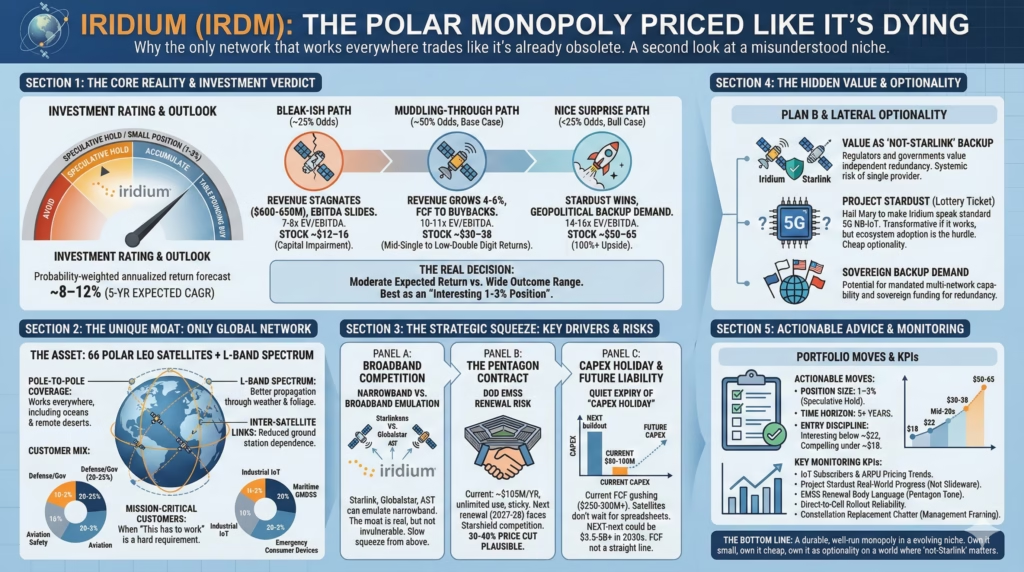

The core reality:

- Iridium is a high-quality, niche monopoly

- Sitting in the middle of a messy, slow-moving tech transition

- Where the distribution of outcomes is unusually wide and asymmetric

At current levels, IRDM screens as a speculative hold / small position, not a table-pounding bargain and not a clear short.

- Rough, probability-weighted expectation: ~8–12% annualized over 5 years

- With a 5-year base case IRR closer to 5–10%

- Bull case: 18–22% annualized if a few low-odds things break right

- Bear case: permanent capital loss in the -15% to -25% range

The real decision isn’t “good company or bad company.” It’s whether the trade-off — moderate expected return, very wide range of outcomes — is worth tying up capital when the S&P 500 exists… or if that capital is better off in something that doesn’t need a five-year explanation.

For most portfolios, IRDM belongs in the “interesting 1–3% position” bucket, not the “retirement depends on this” bucket.

It’s a more subtle story than either its fans or detractors usually bother to tell.

The Only Network That Actually Works Everywhere

Iridium’s asset is simple to describe and almost impossible to recreate.

- 66 operational low Earth orbit satellites (plus spares) in polar orbits

- Global L-band spectrum licenses, in a band that handles weather and foliage extremely well

- Inter-satellite links, so traffic is routed in space without depending heavily on ground stations

- Coverage from pole to pole, oceans, deserts, remote infrastructure — everywhere

It is the network of choice when “This has to work” isn’t marketing copy but a hard requirement.

That leads to a very specific customer mix:

- U.S. and allied defense and security agencies

- Maritime operators needing compliance and safety services (GMDSS)

- Aviation safety, cockpit comms, ADS-B backup

- Industrial and logistics IoT: shipping, mining, heavy equipment, oil & gas

- Consumer devices that pretend to be fun gadgets but exist for when things go really wrong (Garmin inReach, etc.)

The numbers on the page look tolerable for something trading at “disruption victim” sentiment levels.

- 2023 revenue: ~$791 million (Iridium 10-K)

- 2023 operational EBITDA: ~$618 million

- Service revenue is the bulk, equipment is the smaller, lumpier piece

- Government revenue is roughly 20–25% of the total

- Capex has collapsed from $400M+ per year during the Iridium NEXT buildout to ~$80–100M in recent years

On paper, that’s a free cash flow machine: $250–300M+ in annual FCF is reasonable through this decade if nothing explodes, figuratively or literally.

This is what the bulls mean by “capex holiday” — the network is done, paid for, and now mostly maintained, not rebuilt.

Of course, “holiday” implies it will end.

Narrowband vs Broadband: A Real Difference, Slowly Fading

Iridium lives in narrowband land: low data rates, small messages, rugged reliability. Starlink and its cousins live in broadband land: high data, video, consumer internet.

That distinction once looked like a moat.

Iridium’s L-band frequency:

- Works better through clouds, rain, foliage, and even some building materials

- Uses low power, perfect for small sensors and battery-powered devices

- Is licensed globally, and there is not more of it being printed

Starlink, OneWeb, Kuiper and others fly Ku/Ka-band: higher frequency, more data, worse propagation.

So for critical safety-of-life and industrial IoT, Iridium has been the default choice.

Here’s the uncomfortable bit: broadband systems can easily emulate narrowband. The reverse is not true.

Sending a 160-character SOS message, or a tiny telemetry packet, is trivial for Starlink or AST SpaceMobile. Yes, the physics of power budgets and antennas still matter. Yes, handset integration details matter. But directionally, the world is moving from:

- “Iridium or nothing”

to - “Iridium or Starlink or Globalstar or AST… depending on politics, price and paranoia”

The moat is real, just not invulnerable. It is being nibbled at from above.

Evidence of the nibbling:

- Apple / Globalstar: iPhone satellite SOS launched in 2022, now rolled out across multiple countries. Hundreds of millions of people have been conditioned to expect “free” satellite backup.

- Starlink / T-Mobile: Direct-to-cell tests already sending texts from standard phones over modified Starlink birds, with commercial rollout sketched for 2024–2025.

- AST SpaceMobile: In 2023, its BlueWalker-3 satellite completed the first 5G voice call via an unmodified Samsung phone (partnered with Vodafone and AT&T).

This is the backdrop for Iridium’s strategic headache. Not instant doom — more like a slow squeeze.

The Golden Handcuffs of the Pentagon Money

The U.S. Department of Defense is Iridium’s biggest, most important, and most double-edged customer.

- Under the Enhanced Mobile Satellite Services (EMSS) contract, DoD and allies get unlimited usage of Iridium’s network for a fixed annual fee.

- The 2019 renewal was worth $738.5 million over 7 years (per DoD release), or roughly $105M per year.

- That flows largely as high-margin service revenue.

For a company of this size, that’s a solid, bond-like anchor. Canceling this overnight would be operationally and politically messy, so it is usually described as “sticky.”

Sticky, however, is not “forever.”

Since that 2019 contract, the landscape has shifted:

- SpaceX Starshield is deploying militarized Starlink capacity, focused specifically on government and defense use.

- Starlink has already been battle-tested in Ukraine, for better and worse, which gives defense planners both confidence and anxiety.

- Geopolitical risk around depending on a single, privately controlled broadband network is a now open debate inside Western governments.

The next meaningful EMSS renewal cycle (around 2027–2028) happens under vastly different competitive conditions than the last one.

Full cancellation seems unlikely — redundancy still matters — but a 30–40% price cut is completely plausible if the Pentagon wants to make a point and spread the love.

For a business this levered to one big, high-margin contract, a haircut of that size would sting:

- Government revenue down

- Margins compressed

- Narrative flips from “bond-like floor” to “shrinking anchor”

The market mostly knows this, but still talks about the contract like it’s some eternal annuity. It isn’t.

Project Stardust: A Lottery Ticket Masquerading as Strategy

After Qualcomm walked away from the Iridium 5G handset partnership in 2023, Project Stardust appeared as the new shiny thing.

The stated idea:

- Make Iridium’s network speak standard 3GPP 5G NB-IoT protocols

- So that future chipsets and modules can connect without custom, proprietary silicon

- Turn Iridium into background infrastructure for millions of devices, not a bespoke niche protocol

Conceptually, Stardust is smart. Proprietary stacks are a strategic tax in a world marching toward standardization.

The blunt reading, though, is that it’s a hail Mary:

- If Stardust works: Iridium becomes a critical, standards-based, narrowband satellite leg for global IoT and possibly some handset use. That’s transformative.

- If it fails or is too late: Iridium becomes a permanently niche, increasingly marginalized provider to segments that are very price sensitive.

The market behavior suggests it assigns something like 25% probability of actual success. That’s not far from reality:

- The engineering challenge is non-trivial but not insane.

- The real dependency is on ecosystem adoption — chipset vendors, module makers, operators.

- Those players already have multiple suitors (Starlink, AST, Globalstar, terrestrial operators) pitching different NTN (non-terrestrial network) visions.

So Stardust is best treated as cheap optionality for equity holders, not as the core of the thesis. There’s a huge difference between “possible” and “predictable.”

The “Capex Holiday” With a Quiet Expiry Date

Bulls love to point out that Iridium’s monster capex cycle are over.

Fair enough:

- Iridium NEXT satellites were launched 2017–2019

- Total bill: more than $3 billion

- Designed life: ~15 years

- Realistic replacement planning has to begin well before theoretical end of life

From now through roughly the end of this decade, the existing constellation should support:

- Modest capacity enhancements

- New services layered on top

- A relatively low capex regime (tens of millions per year, not hundreds)

That translates into very attractive free cash flow and has enabled:

- Debt reduction

- Share buybacks

- A small but symbolic dividend

The market likes that kind of story. Or used to.

What often gets hand-waved away:

- Satellites don’t politely wait for the spreadsheet to say “Year 15” before failing. Failures will stagger in.

- Replacement costs will not be 2010s dollars. Inflation in launch and satellite manufacturing is real.

- A full NEXT-next constellation could run $3.5–5B in nominal dollars, depending on architecture, launch costs, and how much flexibility is built in.

Some of the current capital return behavior looks less like supreme confidence and more like:

“Return as much cash as possible to shareholders while the system is in its cash-gushing middle age, before the next rebuild has to be funded.”

That isn’t necessarily bad. It just means the spreadsheet line labeled “normalized free cash flow” is probably not a straight line into the 2030s.

When the Monopoly Becomes Plan B

One under-discussed angle: Iridium might actually be more valuable as Plan B than Plan A.

In many critical systems — defense, aviation, maritime — regulators and governments are waking up to the fact that:

- Over-reliance on a single provider (say, Starlink) is a systemic risk

- Space weather (big solar storms), cyberattacks, and debris can cause correlated failures

- Some capacity needs to be physically and politically independent

In that setting, Iridium’s quirks become virtues:

- Completely separate spectrum

- Different orbital architecture

- Proven, boring reliability

- Not controlled by Elon Musk, which increasingly matters inside governments nervous about single points of failure

If Starlink has a major, publicized outage or politically driven restriction, the value of “not-Starlink” goes up dramatically.

No one can responsibly model this in a DCF. But the optionality is real:

- A mandatory backup requirement for certain global systems

- Sovereign funding for additional redundancy capacity

- Regulatory mandates for multi-network capability in critical infrastructure

These are unlikely events in any given year and easy to wave away in a single budgeting cycle; over a decade, though, those low-probability tailwinds start to matter in ways that only become obvious after they’ve already reshaped the playing field.

The Scenario Spread, in Plain Language

Instead of a neat table, here’s what the world could look like by 2030 for IRDM.

Bleak-ish Path (say 20–25% odds)

Direct-to-handset becomes normal. Starlink/T-Mobile own a big chunk of consumer messaging and some emergency. Apple/Globalstar expand coverage and quietly grab the “premium emergency” niche. AST SpaceMobile or similar players light up full broadband to regular phones for airlines and ships.

Satellite messaging and IoT pricing gets hammered. Cheaper, more flexible options exist. Iridium still sells capacity to defense and rugged industrial users, but:

- Revenue stagnates around $600–650M

- EBITDA slides into the $280–320M band

- EMSS renewal takes a 30–40% pricing cut

- The market grants a 7–8x EV/EBITDA multiple to a no-growth, pre-replacement-cycle asset

Result: Stock somewhere in the $12–16 zone. Down 35–50% from mid-20s. Not a zero, just slow-burning capital impairment.

Muddling-Through Path (base case, maybe 50% odds)

Iridium remains the “reliable backup” and the default for a bunch of industrial IoT, maritime safety, and defense niches. Direct-to-phone services expand, but networks and regulators realize a second, independent option is handy.

- Revenue grows 4–6% annually

- EMSS is renewed with a 10–15% trim

- IoT subs grow at a healthy clip, ARPU flat to slightly down

- Free cash flow goes mostly to buybacks and some debt reduction

- Share count shrinks 3–4% annually

- The market eventually values the company at 10–11x EV/EBITDA as a reliable, if somewhat threatened, cash cow

Result: Stock in the $30–38 range in 5 years. Roughly +20% to +55% total from mid-20s, which works out to mid-single to low-double digit annualized returns.

Nice Surprise Path (bull, maybe 25% or less)

A couple of low-odds things line up at once:

- Project Stardust actually ships and gets real adoption in the 3GPP NB-IoT ecosystem

- Some geopolitical scare or major outage forces regulators to explicitly mandate independent backup networks

- Iridium wins expanded or multi-layer government contracts, not just DoD but allied sovereigns

- A strategic buyer (Amazon Kuiper, a European consortium, or a sovereign wealth fund) decides that buying Iridium is cheaper and faster than building a truly independent second network

In that world:

- EBITDA grows solidly

- Perceived strategic value of L-band + polar coverage + in-orbit assets spikes

- Market or acquirer pays 14–16x EV/EBITDA

Result: Equity value in the $50–65 region, implying +100% to +165% upside over 5 years.

Blend those paths with reasonable probabilities, and the math lands near ~8–12% expected CAGR. Not lottery-ticket territory. Not dead-money either.

This matters more than it sounds for valuation: the range between “normal meh” and “ouch” is wider than the spread between “normal meh” and “euphoria.”

What the Crowd Is Missing, Both Ways

Markets rarely get the whole story wrong. Usually they just obsess over one chapter.

On Iridium, they’re roughly:

- Overstating: the idea that Starlink = instant death

- Understating: the fact that technological transitions are messy, slow, and often leave durable niches intact

- Ignoring: the lateral tail risks and tail opportunities that don’t fit in a quarterly slide deck

A few specific mispricings:

- Starlink Expands the Pie and the Risk

Starlink normalizes the idea that everything should be connected, everywhere. That grows the addressable market for satellite connectivity and makes satellite dependence a bigger systemic risk. The bigger Starlink gets, the more valuable backup becomes, especially for governments. - Defense Planning Is Conservative, Not Trend-Following

U.S. and allied militaries will absolutely test, buy, and deploy Starlink-based and AST-based solutions. But they won’t happily bet critical comms on a single, fragile orbital architecture. Embedded, battle-tested systems like Iridium tend to lose share slowly, not overnight. - The Capex Question Is Real, Not Fatal

Bearish arguments often jump straight from “replacement cycle is coming” to “equity is doomed.” That’s lazy. The outcome will depend heavily on:

- How much FCF is harvested between now and the decision

- What the revenue base looks like by 2028–2030

- Whether new architectures (rideshares, cheaper buses) lower rebuild costs

The equity story could survive a rebuild. It might not enjoy it, but it can survive.

- Lateral Optionality Is Weirdly Cheap

Regulation around climate monitoring, global distress systems, neutral humanitarian communications, and sovereign-controlled backup networks is evolving. Iridium sits in the right place to benefit if any of those shift from “nice to have” to “must have.” Most of these processes lives in obscure working groups and subcommittees, the kind of meetings where time seems to slow down and acronyms quietly multiply on every slide.

Financial models, by design, ignore those scenarios. The option sits unpriced in the tail.

Management: Skilled Operators Standing on a Clock

Matt Desch has run Iridium since 2006, spanning:

- The messy aftermath of the original Iridium bankruptcy

- The whole Iridium NEXT rebuild

- The shift to recurring, profitable operations

Under his watch, the company:

- Completed a multi-billion-dollar space program on budget — almost unheard of in this industry

- Secured critical certifications (like maritime GMDSS)

- Built out a robust partner ecosystem (Garmin, Caterpillar, and many others)

Capital allocation has been, on the surface, shareholder-friendly:

- Paying down debt

- Implementing buybacks

- Starting a dividend

The subtler read is that management likely sees:

- Limited high-return reinvestment options within the current architecture

- A finite window before the next capacity or replacement decision looms

- Political and technological uncertainty that makes big new bets look risky

There’s also the succession timer. Desch is mid-60s. A new CEO can mean:

- Strategic review and potential sale

- Or, less charmingly, empire-building and value destruction

That’s not knowable ahead of time, yet it is still material.

The Move If Tempted to Hit “Buy”

For practical portfolio construction, IRDM sits in a very specific bucket:

- Type of asset: High-quality, narrow moat, facing disruptive pressure and meaningful tail optionality

- Rating: Speculative hold / small position

- Position size: 1–3% for those comfortable with volatility and technology risk

- Time horizon: 5+ years or don’t bother

Entry discipline matters.

- Shares become interesting below ~$22

- Genuinely compelling under ~$18

- In the mid-20s, the stock already assumes a reasonably smooth base case and some non-disastrous EMSS renewal.

Things worth watching more closely than the quarterly circus:

- IoT subscriber numbers and ARPU

Not just growth, but pricing. Aggressive discounting to fend off Swarm-type competitors would signal margin risk. - Project Stardust real-world progress

Actual announcements with chipset or module vendors matter more than slideware. Presence in 3GPP releases and operator trials is critical. - EMSS renewal body language

RFP hints, Pentagon comments, competing offers from Starshield or others — even tone changes can flag new pressure. - Direct-to-cell rollouts

Especially reliability in real-world conditions. Handset satellite connectivity that only works on clear days in Kansas is one thing; robust, all-weather performance is another. - Constellation replacement chatter

The moment management starts hinting at “preliminary planning” for NEXT replacement, the market will run ahead with worst-case numbers. Listening for how they frame it will matter.

Hard thesis-breakers:

- Two or more consecutive quarters of declining service revenue with no clear, temporary explanation

- EMSS renewal at deeply below current annual levels (say, <$80M per year)

- Clear, public failure or abandonment of Stardust and no alternate IoT strategy

- Equity issuance to plug operational cash holes — a bad sign for a supposed FCF machine

The Reluctantly Grounded Takeaway

Iridium is not a melting ice cube, and it’s not a growth compounder. It’s something more annoying to analyze:

- A durable, well-run monopoly in a shrinking-but-evolving niche

- Sitting at the intersection of genuinely hard physics and overfunded new competitors

- With as much to gain from geopolitical paranoia as from pure product innovation

Its best years of “easy story, rising multiple” are probably behind it. The easy bears are also likely too confident in smooth, flawless disruption by the new kids.

What’s left is a very specific kind of trade:

- Own it small

- Own it cheap

- Own it as optionality on a world where “not-Starlink” quietly becomes a line item in sovereign risk models

And be prepared for long periods of boredom, broken up by sudden spikes in attention whenever something blows up in orbit, literally or politically.

The ice cube may be melting. But it’s still the only ice cube floating over the Arctic, and for certain customers, that still counts for more than any glossy launch video.