$IAI at the crossroads: why the chaos trade is misunderstood

Wall Street’s infrastructure play wins in more scenarios than the market appreciates

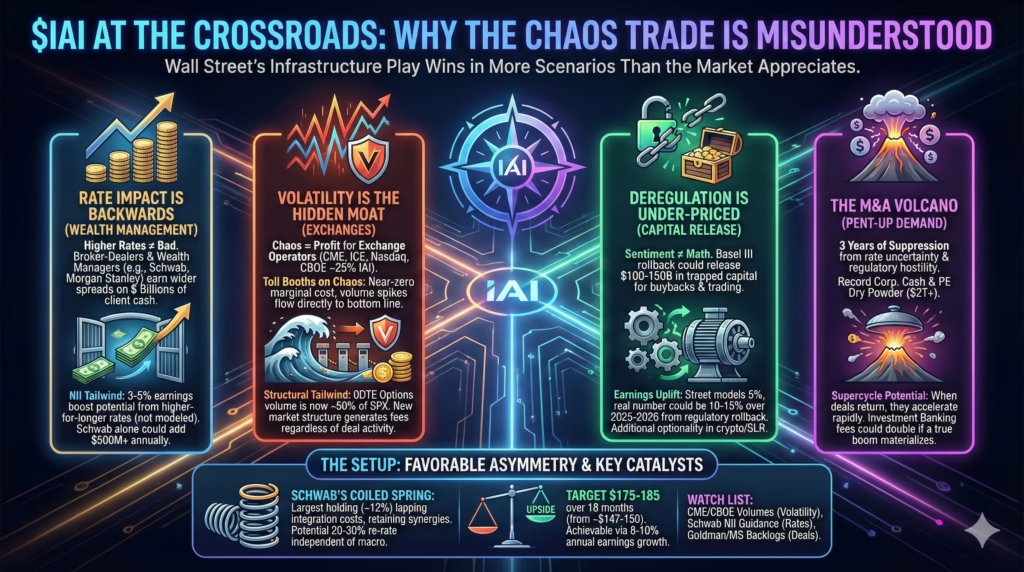

The pitch

IAI offers exposure to capital markets infrastructure at a moment when the market is pricing in deal-freeze risk while ignoring that 30-35% of holdings are effectively long volatility through exchange operators like CME, ICE, and CBOE. The deregulation upside from Basel III endgame rollback could release $100-150 billion in trapped capital at major banks—translating to 10-15% earnings uplift that sell-side models have largely missed. Schwab’s cash sorting headwinds are 90%+ complete. The ETF’s largest holding looks like a coiled spring heading into 2025.

The friction

Concentration risk looms large. The top five holdings represent roughly 45% of the ETF, with Goldman Sachs alone at 11%+. A Goldman-specific blow-up—trading loss, legal settlement, management crisis—would hit IAI hard regardless of sector trends. And if Trump’s tariff escalation triggers genuine systemic stress rather than tradeable volatility, the “chaos benefits trading” thesis breaks down entirely.

IAI drew down over 70% in 2008-2009. Worth remembering.

Time to examine what really drives this.

The market has the rate impact backwards

Consensus holds that the Fed’s hawkish December pivot—signaling only two cuts in 2025 versus four previously expected—hurts financials broadly. This applies bank-centric logic to a capital-markets-centric ETF. Gets the transmission mechanism exactly wrong.

For broker-dealers and wealth managers, higher rates directly benefit net interest spreads on client cash balances. Schwab earns wider spreads on its $80-85 billion in transactional cash. Morgan Stanley’s wealth management division benefits from higher rates on $400+ billion in client deposits. If rates stay at 4%+ through 2025, that’s an earnings tailwind of 3-5% for the wealth management components that almost nobody is modeling explicitly.

The Street is anchored on lower rates being good for deal activity, but the NII benefit at Schwab alone could add $500 million+ annually in a higher-for-longer scenario. This isn’t speculation—it’s math that shows up quarterly in supplementary leverage ratio disclosures and net interest income guidance.

The risk here is that sustained high rates eventually do freeze deal activity long enough to overwhelm the NII benefit. But the market has already priced significant deal pessimism while ignoring the offsetting tailwind. Watch Schwab’s and Morgan Stanley’s wealth management NII guidance through Q1 2025 for confirmation.

Volatility is the hidden moat everyone ignores

The consensus bear case assumes tariff-driven uncertainty freezes capital markets activity broadly. This conflates investment banking—which yes, suffers from uncertainty—with trading and market-making, which benefits massively from volatility.

Q4 2024 proved the point: Goldman’s trading revenue surged 32% while M&A advisory stayed flat. CME volumes hit records. The VIX spiked and exchange operators printed money.

Exchanges like CME, ICE, Nasdaq, and CBOE—roughly 25% of IAI’s holdings—operate with near-zero marginal cost per trade. Volume spikes flow directly to profits through operating leverage. These are effectively toll booths on chaos. The bear case requires both a deal freeze and a volatility collapse. Historically, you don’t get both simultaneously. If Trump creates chaos, trading revenues surge. If Trump creates stability, deals come back. IAI wins in more scenarios than the market appreciates.

Here’s the thing—the structural tailwind is even more compelling. 0DTE options volume has grown from essentially nothing in 2019 to roughly 50% of SPX options volume in 2024. Retail traders who discovered options during the meme stock era have become permanent derivatives users. This isn’t cyclical—it’s a new market structure that generates exchange fees, clearing fees, and market-making spread capture on every trade. CBOE and CME are the primary beneficiaries, and that revenue doesn’t depend on deal activity or CEO confidence. Reminds me of how payment networks quietly became the most profitable businesses in finance while everyone focused on lending—though that’s probably a comparison for another time.

The risk is that a true systemic event—not volatility but counterparty stress—freezes everything including trading. That’s the 2008 scenario. The market is pricing in 2008 probability while ignoring that most “chaos” scenarios are actually tradeable volatility.

Schwab’s coiled spring setup

The largest holding at roughly 12% of IAI, Schwab has been treated as dead weight due to cash sorting headwinds and TD Ameritrade integration costs.

This narrative is stale.

Cash sorting—where clients moved deposits to higher-yielding alternatives—is 90%+ complete. Deposit outflows have stabilized and client cash as a percentage of assets has normalized to pre-2020 levels. The “Schwab is broken” story was accurate in 2023, questionable in 2024, and likely wrong in 2025.

What the market is missing: Schwab is about to lap the worst of TD Ameritrade integration costs while retaining the revenue synergies. Management guides to $1 billion+ in incremental cost savings realized through 2025. Their dominant position in RIA custody gives them structural exposure to the $84 trillion generational wealth transfer accelerating over the next two decades. This is a subscription business with AUM-linked fees that doesn’t care about quarterly GDP prints.

If Schwab executes on integration—which they historically do, having successfully integrated Ameritrade, OptionsXpress, and others—the ETF’s largest holding could re-rate 20-30% independent of macro conditions. The risk is execution stumbles or renewed deposit flight if rates spike further. But the setup is asymmetric: downside scenarios are well-understood while the integration payoff remains underappreciated.

Deregulation is under-priced, not over-priced

The consensus view holds that IAI’s 35% YTD gain already reflects deregulation optimism. This confuses sentiment with mechanics.

The market has priced in good feelings about a Trump SEC. It hasn’t priced in the actual regulatory math. Basel III endgame rollback—now nearly certain with Trump’s regulatory appointees—could release $100-150 billion in trapped capital at major banks. For Goldman and Morgan Stanley, this translates to potentially 15-20% increases in buyback capacity and trading desk expansion.

The Street is modeling perhaps 5% earnings uplift from deregulation; the real number could be 10-15% over 2025-2026. Additional optionality exists in SLR Treasury exemption reinstatement, crypto ETF approvals beyond Bitcoin, and reduced capital requirements for market-making activities. Each represents incremental earnings potential that doesn’t appear in base case models.

Risk is implementation disappointment—regulatory change moves slowly even with political will. But the current price assumes the easy money has been made. If the regulatory calendar actually delivers, IAI has another 15-20% of multiple expansion potential that isn’t in current price targets, separate from any deal recovery.

The M&A volcano nobody’s timing correctly

Deal activity has been suppressed for three years—not because deals don’t make strategic sense, but because of rate uncertainty, antitrust aggression, and valuation disconnects. Corporate cash piles sit at record levels. Private equity holds $2+ trillion in dry powder with fund lives expiring. Strategic acquirers have watched competitors strengthen while they’ve waited.

The bottleneck was regulatory hostility and rate uncertainty. Both are clearing.

When deal activity recovers, it doesn’t recover gradually. M&A volume tends to accelerate rapidly as boards realize waiting is no longer an option and competitive pressure to deploy capital intensifies. 2021 showed what a boom looks like; current activity runs at 40-50% of that level with more pent-up demand. Investment banking fees at Goldman and Morgan Stanley could double from current run rates if a true M&A supercycle materializes. At roughly 15% of IAI exposure, this would add 10-15% to ETF earnings.

The risk is that uncertainty persists and the dam never breaks. CEO confidence surveys remain depressed. Boards may stay cautious despite regulatory green lights. The consensus has already priced in a prolonged freeze though—any acceleration represents upside surprise.

The bottom line

Key metrics to monitor quarterly: CME and CBOE daily trading volumes for volatility thesis confirmation; Schwab net new assets and NII guidance for the wealth management recovery; Goldman and Morgan Stanley investment banking backlog commentary for deal activity signals. The earnings growth required to justify current valuation is 8-10% annually—achievable through a combination of trading revenue stability, deregulation uplift, and even modest deal recovery.

Look, thesis breaks if: systemic credit event materializes rather than tradeable volatility; Basel III endgame rollback stalls or reverses under political pressure; Schwab integration costs accelerate or deposit flight resumes; or Goldman faces a major idiosyncratic blow-up that drags the concentrated ETF lower. The asymmetry favors bulls—downside scenarios are well-telegraphed and partially priced, while multiple upside catalysts remain underappreciated. Not a slam dunk. But the risk-reward tilts favorable for patient capital willing to ride the volatility.