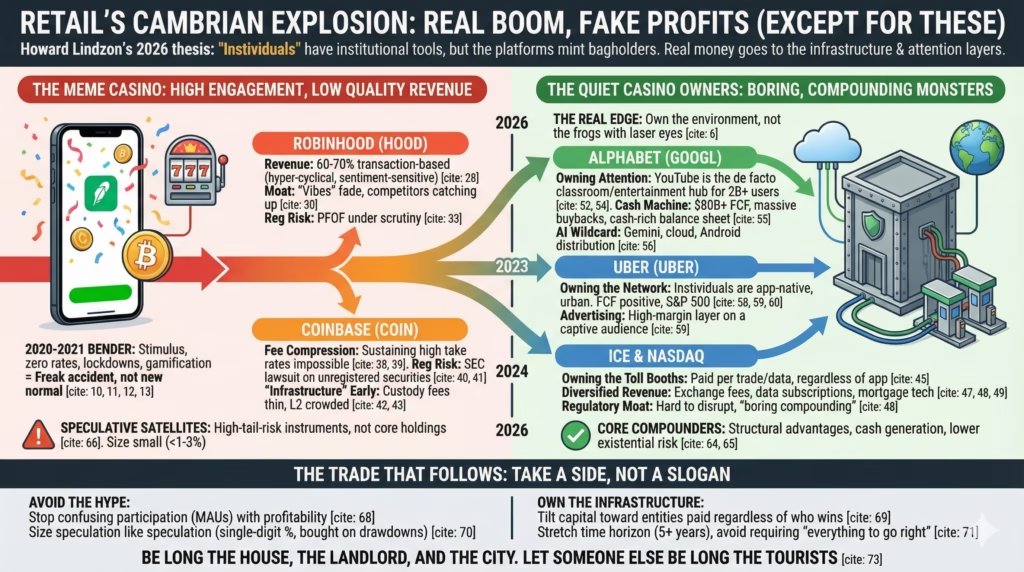

Retail’s “Cambrian Explosion” Is Real. The Profits Mostly Aren’t (Except for These Few Names)

Robinhood and Coinbase are the meme. Alphabet, Uber, and the exchanges are the money.

Why This Gold Rush Still Mostly Mints Bagholders

Howard Lindzon calls it the “Cambrian explosion” of retail investing = Howard Lindzon’s 2026 Retail boom thesis.

In Howard Lindzon’s framing, “the Cambrian explosion of retail investing” is a biological metaphor applied to financial markets.

Cambrian explosion (biology): a period (~540 million years ago) during which, in a relatively short span of time, a vast number of new species appeared abruptly. Many emerged; very few survived over the long term.

Applied to markets: the simultaneous arrival of a large wave of new retail participants, new tools, new behaviors, and new modes of participation.

Zero-commission trading, tokenization, prediction markets, mobile apps, real-time data feeds, Discord groups, TikTok gurus. The Instividual. Retail traders with institutional-grade tools.

The direction almost certainly right. Markets are more open, more global, more always-on than at any point in history. Retail order flow went from sideshow to meaningful chunk of daily volume; by some estimates, individual investors accounted for roughly 20–25% of US equity trading at the 2021 peak, up from around 10% pre-Covid (JPMorgan, Goldman).

But “directionally right” is very different from “this is a good way to make money in public equities”.

The popular trade is obvious: buy Robinhood (HOOD) and Coinbase (COIN) as pure plays on the Instividual era. If retail is the future, own the platforms where they trade. Easy story for a slide deck, great cocktail party narrative.

The problem: those companies don’t monetize retail existing. They monetize retail going nuts.

2020–2021 was a freak accident of macro, psychology, and boredom. Stimulus checks, zero rates, lockdowns, TikTok, WallStreetBets, SPACs, NFTs, meme stocks. The intensity of that moment was the business model. That’s what their valuations still quietly assume.

The better trade looks almost inverted:

- Own the information layer that educates and entertains retail (Alphabet / YouTube).

- Own the real-world network that captures their spending and attention (Uber).

- Own the regulatory-embedded toll booths that get paid whenever anything trades (ICE, Nasdaq).

- Treat HOOD and COIN as small, speculative options, not as the backbone of a portfolio.

The Cambrian explosion is real. Most of the new species die off. The trick is to own the environment, not the frogs with laser eyes.

The Instividual Narrative: Insightful, and Also Convenient

Howard Lindzon is not some armchair pundit discovering retail last week.

Stocktwits helped invent the modern “finfluencer” format. The cashtag. The idea that retail can talk markets in real-time, at scale, with some of the same data that used to sit only on Bloomberg terminals.

He was early, correct, and very well paid for that call.

So it’s no surprise that his latest framing—the Instividual with institutional tools—has become the narrative backbone for a whole ecosystem of products, funds, and startups.

The story goes roughly:

- Trading is cheap and always-on.

- Data is abundant.

- Retail now has access to derivatives, leverage, algo-style tools.

- Therefore, retail starts to behave more like institutions.

The trouble starts right there.

A pile of actual evidence says something closer to the opposite:

- Decades of work by Brad Barber and Terrance Odean on individual investors (using real brokerage data) show that the more people trade, the worse they do. One classic paper found active retail traders underperformed the market by around 5–6 percentage points per year before taxes and costs.

- Studies of day traders in Taiwan, Brazil, and the US repeatedly converge on the same depressing stat: roughly 1–2% of ultra-active traders make significant, persistent profits. Everyone else subsidizes them.

- A 2021 FINRA/NORC study on Covid-era new investors showed that a big chunk had poor diversification, high turnover, and very shaky risk understanding.

In other words, the “Instividual” owns institutional-grade tools but does not consistently use them like an institution.

That gap matters. Market makers and brokers make money off that gap.

If retail truly became institutionally sharp, the economics of payment-for-order-flow and spread capture would crater. Yet payment for order flow remains a multi-billion-dollar industry, and firms keep bidding aggressively for that flow. That says something uncomfortable about who is the prey.

2020–2021 Wasn’t the New Normal, It Was the Bender

The pandemic trading boom is being misremembered as “early innings”.

Look at the cocktail of conditions:

- US policy dropped roughly $800+ billion of stimulus checks straight into bank accounts.

- Short-term rates went to zero. Cash paid nothing. Risk felt free.

- Lockdowns trapped people at home. Sports and live entertainment vanished for long stretches.

- Brokers cut commissions to zero and gamified everything from options to crypto.

- Viral feedback loops formed: TikTok “stock tips”, Discord pump rooms, mass media covering GameStop like a revolution, not a short squeeze.

That level of focus and leverage on markets was less a starting point, more a contained hallucination.

The comedown is pretty obvious:

- Rates are now in the 4–5% range. T‑bills yield something. A default-risk-free 5% is surprisingly seductive once doing 60-hour weeks again.

- Stimulus checks are gone; fiscal support is tighter, not looser.

- Many 2020–2021 newbies learned about volatility the hard way in 2022’s drawdowns—especially in crypto and unprofitable growth.

Robinhood’s own numbers tell the story more honestly than the marketing:

- Funded accounts spiked into the tens of millions during 2020–2021.

- Monthly active users peaked during that frenzy, then drifted lower and stabilized.

- Crypto and options revenue surged with volatility, then sagged, then half-recovered with the next Bitcoin run.

Coinbase looks similar:

- At the 2021 crescendo, monthly transacting users were north of 11 million.

- In the following crypto winter, that number fell into the mid-single digits.

- Revenue whipsawed with volumes and crypto prices, because that’s what happens when the core business is volatile transaction skim.

The big lesson: these businesses are not primarily levered to the presence of retail. They are levered to the mood of retail.

Mood is not a durable asset.

Robinhood: When Your Product Is the Binge, Not the Habit

Robinhood is the archetypal Instividual platform: sleek mobile UX, options and margin one tap away, confetti (until regulators glared), push notifications that feel more like Instagram than Schwab.

Underneath the storytelling, the business is brutally simple:

- Make money when customers trade a lot (transaction revenues, especially options and crypto).

- Make money when rates are high (net interest on idle cash and margin).

- Try to layer on subscriptions, credit cards, and other “financial services” as a stabilizer.

Several awkward realities sit under the hood:

1. Transaction-heavy revenue is not quality revenue

Across recent periods, 60–70% of revenue has come from transaction-based activity—mostly options and crypto.

Those flows are:

- Hyper-cyclical.

- Highly sensitive to sentiment.

- Often dominated by a minority of users who churn accounts aggressively.

Net interest income looks gorgeous while rates are elevated. That won’t be a permanent state. Revenues that depend on the Fed staying at “fun” levels are not really diversification.

2. The moat is vibes, and vibes fade with age

In 2016–2019, Robinhood’s app was legitimately miles ahead of the big incumbents.

Flash forward:

- Fidelity, Schwab, and even some big banks now have clean, modern mobile apps.

- Transfers between brokers take days, not weeks. ACATS makes movement cheap and easy.

- As users move from $3,000 accounts to $300,000 accounts, the tolerance for outages, meme-like UI, and “oops” risk tends to drop.

Behavior in the wild suggests something unflattering: Robinhood is where a lot of people start, not where they finish.

3. Regulators can absolutely wreck the economics

Payment for order flow (PFOF) is the heart of the model.

When retail submits marketable orders, wholesalers like Citadel Securities and Virtu pay for that flow because it is—on average—predictable and profitable to trade against. That’s the point of best-execution debates.

The SEC has repeatedly floated tighter rules around tick sizes, competition for retail orders, and routing transparency. So far, the hammer hasn’t fully dropped. But the risk is not imaginary; it’s existential to margins.

4. Peak earnings may be backward-looking

Right now, numbers can look deceptively strong:

- Bullish equity tape → more options.

- Bitcoin cycles up → more crypto.

- High short rates → fat net interest spreads.

Any combination of:

- lower rates,

- lower volatility,

- stricter rules on PFOF,

…would expose how much of the “new Robinhood” is just rebranded exposure to the same old trading mania.

The market seems to understand this roughly, which is why the stock trades like a leveraged call on future retail excitement. The narrative sounds structural; the underlying drivers are not.

The math just doesnt fully line up with the story.

Coinbase: High-Margin Tollbooth… on a Very Wild Road

Coinbase is the canonical crypto blue chip.

Dominant US retail exchange. Institutional custody for giants like BlackRock. The Base L2 chain. Staking, subscription products, a brand that’s survived multiple crypto winters.

If the bet is “crypto integrates into the financial system”, Coinbase looks essential. The question is not whether the business has a future — that part is basically settled — it is how much of that future is already priced, and how many mines sit in the regulatory field between here and there.

Several uncomfortable points:

1. Fee compression is not a forecast, it’s ongoing

At IPO, retail trading fees were often north of 1.5% on small orders.

Today:

- Fee tiers are substantially lower.

- Global competition from Binance, OKX, Bybit, and a swarm of smaller venues forces pricing down.

- Sophisticated users route size through lower-fee venues, OTC, or DeFi.

This is the same story that hit equity brokers over the last twenty years, just sped up. Sustaining sky-high take rates in a commoditized trading product is not a stable equilibrium.

2. Regulatory overhang makes this quasi-option, not plain equity

The SEC’s lawsuit against Coinbase (filed June 2023) goes to the core of the business: are many of the assets listed on the platform unregistered securities?

Depending on the final shape of regulation:

- In a hostile scenario, a big slice of revenue-producing tokens could vanish from the US platform.

- In a friendly or at least clear scenario, Coinbase becomes the default compliant gateway and wins big.

That payoff profile is binary enough that prudent sizing starts to resemble an options approach: small notional, accept the tails.

3. “Infrastructure” products are promising, but early

Custody for ETFs, Base L2, staking, subscription products: all pointed in the right direction strategically.

But:

- Custody fees for large institutional mandates are thin (0.05–0.20% annually is common).

- L2 economics are uncertain and fragile; competition from other Ethereum L2s and alternative chains is intense.

- Subscriptions and services grew quickly off a small base, then hit the law of large numbers and tougher comps.

From an equity-holder’s perspective, this is still a business dominated by trading fees and volatile cycles in retail activity.

Coinbase is what HOOD wants to be: a volatile, high-upside, high-tail-risk instrument on human speculation. That can have a place in a portfolio. Just not near the core.

The Boring Monsters That Quietly Own the Casino

Step away from the apps for a second and look at the legal plumbing.

Intercontinental Exchange (ICE) and Nasdaq (NDAQ) do not care who wins the meme war. They do not care which app a 24-year-old uses to YOLO weekly calls. They sell access to the venue, the data, and the indices.

Some basic context:

- ICE owns the New York Stock Exchange and a suite of futures, energy, and commodities exchanges, plus mortgage technology. In 2023, it generated around $9.9 billion in revenue with operating margins north of 50% on many exchange businesses.

- Nasdaq has evolved from “that tech exchange” into a broader data and technology firm. 2023 revenue was around $6+ billion, with a big slice coming from recurring data, analytics, and index licensing.

Key features of these models:

- Every time someone trades, somebody pays exchange fees or alternative venue fees. Volume is the tide that lifts them.

- Market data is sold on subscription to brokers, funds, algos, banks—recurring, high-margin revenue streams that don’t care whether retail outperforms or blows up.

- Regulation acts as a moat. Operating a major exchange is not something a scrappy startup spins up from a WeWork.

There are risks:

- Fee pressure on basic trade execution.

- Increased competition from dark pools, alternative trading systems, and direct listing venues.

- Political noise around “market data monopolies”.

Compared to HOOD or COIN:

- The revenue base is more diversified.

- The regulatory risk is around how much they earn, not whether they are allowed to exist.

- The downside scenarios look more like “boring single-digit compounding” than “-70% drawdown on one bad cycle”.

ICE in particular has done something quietly clever: using its strong cash flows to expand into mortgage tech, giving exposure to US housing finance workflows. That correlation almost orthogonal to speculative retail trading.

Boring. Profitable. Very hard to disrupt. Which is exactly what tends to work over 10–20 years.

Alphabet: Owning the Retail Investor’s Brainspace

Google’s relevance to retail investing isn’t just “people search for stock tickers”.

YouTube has become the de facto classroom, entertainment hub, and echo chamber for retail:

- Finance YouTube channels range from CFA-level deep dives to “I turned $200 into $2 million” fantasy.

- Algorithmic recommendations help form narratives: AI booms, Tesla cults, option-selling “income” strategies.

- According to Google, YouTube reaches over 2 billion logged-in users monthly. Even if a small fraction watches finance content, the absolute number is enormous.

The crucial piece: Alphabet gets paid regardless of whether viewers learn anything useful.

- Ads run in front of the YOLO options video and the sober asset-allocation explainer.

- Creators who pump trading, or critique it, all drive engagement in the same machine.

- If Instividuals need an infinite content firehose to justify their activity, YouTube is right there, charging tolls.

Financially, the story is almost insultingly strong:

- Alphabet generated about $80+ billion in free cash flow in 2023.

- The balance sheet holds more cash than debt.

- The company is running tens of billions in annual buybacks, quietly reducing share count.

AI is the wild card:

- Gemini, plus deep internal models, plus custom silicon (TPUs), plus cloud, plus Android distribution.

- If AI assistants become the main interface to information—including investing and trading tools—Google sits at a privileged choke point.

At ~low-20s multiples of earnings with that level of cash generation, this is, absurdly, the conservative way to express the Instividual trend.

Everyone chases the casino operators; Alphabet owns the strip mall where all the casino workers eat lunch.

Uber: The Instividual Still Needs a Ride

There is a softer, less obvious link between retail investing and Uber.

The Instividual tends to be:

- Urban or near-urban.

- Smartphone-native.

- Comfortable with app-mediated everything: rides, food, payments, side gigs, trading.

Talk to a few rideshare drivers in any big city and many will mention hearing endless chatter about crypto, options, or side hustles from the back seat; it’s a tiny, anecdotal datapoint, yet it matches the broader sense that financial speculation has become just another lifestyle topic squeezed in between podcasts and food-delivery orders.

Uber sits in that same behavioral lattice:

- Ride-hailing is the default mobility option in many cities.

- Uber Eats captures a chunk of discretionary spending from the same demographic that dabbles in options and crypto.

- Growing in-app advertising lets merchants and brands target exactly these spenders.

The business has quietly grown up:

- Uber produced positive free cash flow in 2023, finally graduating from “permanent cash furnace” to “real company”.

- It joined the S&P 500, forcing benchmarked funds to own it.

- Operating leverage started to show: as scale grows, incremental rides are cheaper to serve.

Robotaxis used to be the big existential risk: what if Tesla or Waymo simply replace human drivers with fleets of autonomous cars?

That risk hasn’t vanished, but the market is now more realistic:

- Waymo and others have moved cautiously, with limited deployments.

- Full autonomy everywhere remains technically and politically messy.

- Uber has already started partnering (e.g., with Waymo in Phoenix), confirming the obvious: the demand network—knowing where, when, and how people want to move—has value even if the car is a robot.

The Instividual thesis says affluent, tech-comfy consumers will keep integrating more of life into apps. Uber already owns several of those use cases, with more monetization knobs left to turn.

Not a pure play on trading. A pure play on the users of trading apps actually having money and places to be.

Tesla and the Meme-Asset Mirage

Tesla lives at the center of retail investing culture.

- One of the most widely held retail names in the world.

- Massive presence on Reddit, X, YouTube, TikTok.

- A CEO who tweets more than many influencers.

Yet the connection between “retail mania” and “Tesla as a business” is often misunderstood.

Retail doesn’t buy Tesla cars because they trade Tesla stock. In many cases, it’s the other way around.

At recent rich valuations:

- The stock embeds high expectations for EV growth, margins, energy storage, self-driving, and robot labor.

- Competition from BYD, Chinese EV makers, and legacy automakers is accelerating.

- Automotive margins have already come under pressure as price cuts chase volume.

There is genuine technological ambition here, no doubt. But from a portfolio construction perspective, Tesla is something retail trades, not something that profits from trading.

That distinction matters. Exposure to “assets retail likes to touch” is not the same as exposure to “systems that extract rent from retail activity”.

Where the Actual Edge Hides

The seductive move in any “new paradigm” is to overpay for purity.

- Want EV exposure? Buy the hottest EV stock at 60x earnings.

- Want AI exposure? Buy the small-cap AI name mentioned on every podcast.

- Want Instividual exposure? Buy the apps they screenshot.

Purity feels like conviction. It usually prices like it.

A more cynical—read: realistic—view of the Cambrian retail boom suggests a different hierarchy.

Rough sketch, for a five-year+ horizon and an acceptance that nothing is guaranteed:

1. Core Compounder: Alphabet (GOOGL)

- Owns the attention and education rails (Search + YouTube) where retail investors live.

- Generates staggering cash, buys back stock, carries optionality in AI, cloud, and other bets.

- Valuation still sits closer to “quality stalwart” than “story stock”.

2. Growth Engine: Uber (UBER)

- Tied to the same global, mobile, app-native cohort as Instividuals.

- Now solidly free-cash-flow positive, with scale economics still playing out.

- Advertising inside Uber is a high-margin layer very few small investors are modeling properly.

3. Structural Toll Booths: ICE and/or Nasdaq (ICE / NDAQ)

- Get paid when things trade. Stocks, futures, options, indices, data feeds.

- Have regulatory licenses that aren’t going away.

- Probably never 10x from here; very likely still exist and pay dividends when today’s hot brokers are footnotes.

4. Speculative Satellites: HOOD and COIN (tiny sizing, high tolerance)

- Treat them as leveraged tickets on future episodes of mania.

- Position them at “fun money” levels that can go to zero without wrecking anything.

- Only buy after violent drawdowns, not when CNBC starts doing Instividual segments again.

Portfolio construction is not about finding the coolest story. It’s about letting the least amount of stupidity leak into the compounding machine.

The Instividual revolution is real enough; order books look different, market microstructure shifted, cultural attitudes toward owning equities and crypto changed, especially for people under 40, and digital speculation in everything from sports bets to meme coins has become just another normalized way to feel “in the game” without necessarily moving any closer to actual wealth.

The whales that win long term are, predictably:

- The platforms that sell picks, shovels, data, and distraction.

- The exchanges that sit in the middle.

- The global networks that move people and payments around.

The Instividual mostly supplies volatility, fees, and screenshots.

The Trade That Follows

For anyone trying to turn this into something practical instead of another fintech bedtime story, a few blunt moves stand out.

1. Stop confusing participation with profitability

- High app downloads, MAUs, or signups at a broker do not equal durable earnings.

- Look for how a business makes money: spreads, take rates, recurring fees, ad revenue, subscriptions.

- If 70%+ of revenue is tied to short-term trading activity, assume earnings are on a roller coaster.

2. Tilt capital toward entities that get paid regardless of who wins

- Alphabet, ICE, and Nasdaq don’t care whether HOOD beats Schwab or COIN beats Binance.

- They monetize the broad existence of the ecosystem: attention, listings, data, and transactions.

- Where there is deep, ugly competition, try to own the referee, not one of the fighters.

3. Size speculation like speculation

- If HOOD or COIN absolutely must be in the portfolio, ring-fence them:

- Single-digit percentage allocations at most.

- Bought after big drawdowns, not at fresh highs.

- With a mental model closer to LEAP options than to “core holdings”.

- Use boring, cash-generating monsters as the spine, not the garnish.

4. Stretch the time horizon, but not the narrative

- Five years is a reasonable window: long enough for fads to die, short enough that regulation and macro are still guessable.

- Avoid building theses that require everything to go right: flawless execution, friendly regulators, eternal mania.

- Instead, prefer setups where multiple things can go a bit wrong and the equity still muddles through.

5. Accept that most Instividuals will underperform—and position accordingly

- Retail will, on average, continue donating alpha to market makers and high-speed firms. History screams this; nothing about TikTok has changed it yet.

- That isn’t a moral judgment, just arithmetic.

- The opportunity is to own the systems that quietly clip a slice of that donation: the YouTubes, the exchanges, the infrastructure.

If the Cambrian explosion of retail investing keeps going, Alphabet, Uber, ICE, and Nasdaq should grind higher, throwing off cash and occasional upside surprises.

If it fizzles, they still have other engines—search, cloud, advertising, real-world logistics, mortgage tech—to fall back on.

Robinhood and Coinbase, by contrast, live or die by the next wave of gambling disguised as financial self-actualization. That can kind of of work for a while. It just rarely ends with the gambler rich and the house broke.

The side to take is simple, if slightly less glamorous:

Be long the house, the landlord, and the city they operate in. Let someone else be long the tourists.