$GUNR: The capital discipline thesis no one is stress-testing

Resource equities may have structurally changed—but the market is pricing the old playbook

The Pitch: GUNR offers exposure to a potential regime shift in resource company behavior. After a decade of value destruction through reckless capex, management teams have spent four years returning cash instead of chasing production. If this discipline persists through the next downturn—historically when it breaks—through-cycle returns could resemble tobacco stocks from 2010-2020. The market still prices GUNR as commodity beta. It’s increasingly a capital allocation bet.

The supercycle is older than you think

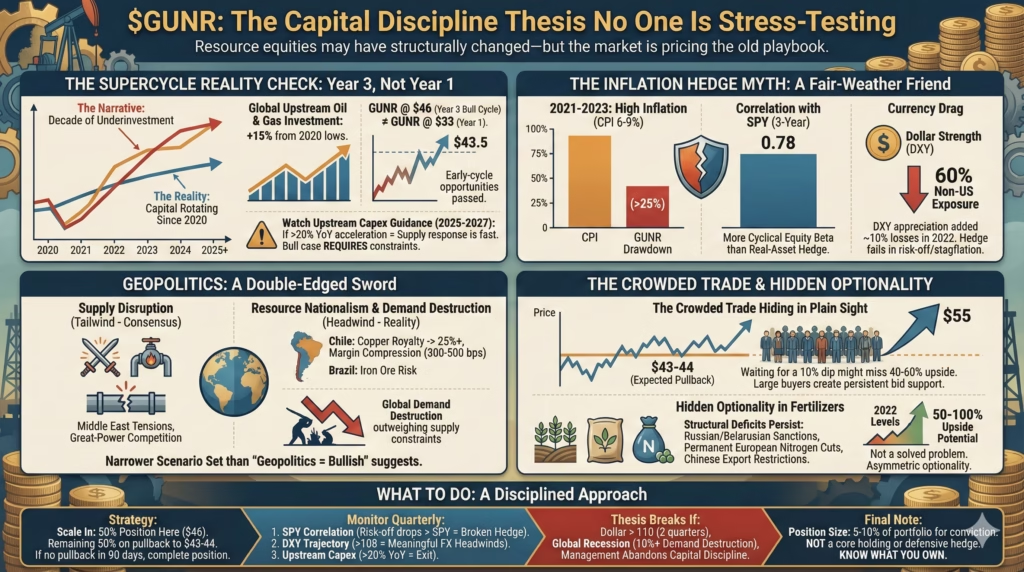

The mainstream narrative positions 2020-2024 as the first leg of a multi-decade commodity outperformance. The contrarian reality: capital has been rotating into this thesis for three years already.

Global upstream oil and gas investment has risen roughly 15% from 2020 lows. Copper concentrate pricing and LNG export capacity constraints are already in valuations.

The “decade of underinvestment” story is increasingly historical, not predictive.

GUNR at $46 pricing Year 3 of a bull cycle offers fundamentally different risk/reward than GUNR at $33 pricing Year 1. The technical breakout above $43.5 confirms the trend—but it also confirms that early-cycle positioning opportunities have passed.

Watch upstream capex guidance from majors for 2025-2027. If capex accelerates more than 20% year-over-year, supply response is faster than bulls model. The bull case requires supply constraints to persist; the data suggests they’re easing.

The inflation hedge that isn’t

Asset allocators position GUNR as real-asset protection against persistent 3-4% inflation. The empirical record tells a different story.

From 2021-2023, CPI inflation ran 6-9% while GUNR experienced a drawdown exceeding 25%. The mechanism: upstream equities carry equity beta layered on commodity exposure. During risk-off environments—even inflationary ones—correlations converge toward 1.0 with broad markets.

GUNR’s 0.78 correlation with SPY over three years suggests it functions more as cyclical equity than real-asset hedge.

The fund’s 60% non-US exposure compounds the problem. Dollar strength during risk-off episodes adds currency drag. In 2022, DXY appreciation contributed roughly 10% additional losses on top of commodity weakness.

The hedge works only under narrow conditions: demand-pull inflation with stable or weakening dollar. Stagflationary or risk-off scenarios—precisely when investors need protection—produce losses in both dimensions. Anyone positioning GUNR as portfolio insurance is buying a fair-weather hedge.

Geopolitics cuts both ways

The consensus frames Middle East tensions and great-power competition as supply-disruption tailwinds. This analysis is incomplete.

GUNR holds significant Latin American mining exposure—Chilean copper, Brazilian iron ore—both facing rising resource nationalism. Chile’s pending copper royalty legislation could lift rates to 25%+, compressing margins 300-500 basis points.

Resource nationalism accelerates precisely when commodity prices make extraction most profitable.

True supply-shock scenarios—Strait of Hormuz closure, Taiwan conflict—would trigger global recession dynamics where demand destruction overwhelms supply constraints. GUNR benefits only if disruptions remain moderate enough to support prices without cratering demand.

This is a narrower scenario set than “geopolitics equals bullish” framing suggests.

The crowded trade hiding in plain sight

The technical playbook recommends waiting for a pullback to $43-44. Sound discipline. Also potentially the most crowded positioning in the trade.

When everyone waits for a pullback, bids materialize at expected support, preventing the dip. Investors waiting for $43 miss a move to $55. Frustration causes capitulation buying at higher prices.

With roughly $4.5 billion in assets and average daily volume around $32 million notional, large buyers must scale in over time, creating persistent bid support.

The strategic question supersedes the tactical one. If the macro thesis proves correct, waiting for a 10% pullback to save 3-4% on entry is suboptimal relative to 40-60% upside.

Six months spent waiting for a better entry that never materializes? That’s a bearish call investors refuse to admit they’re making.

The hidden optionality in fertilizers

Most investors view GUNR’s fertilizer exposure—Nutrien, Mosaic, CF Industries—as played out after the 2022 spike. The structural deficit tells a different story.

Russian and Belarusian potash exports face ongoing sanctions friction. European nitrogen production has been permanently reduced. Chinese phosphate export restrictions continue. The 2022 crisis was papered over by inventory releases and demand destruction—farmers using less fertilizer, accepting lower yields.

This is not a solved problem.

If weather creates a major crop failure, if Chinese export restrictions tighten, or if European natural gas spikes again, fertilizer prices could re-spike to 2022 levels. This creates 50-100% upside in GUNR’s fertilizer holdings—asymmetric optionality the broader “commodity ETF” framing obscures.

What to do with this

GUNR at $46 offers legitimate exposure to capital-disciplined resource producers. But this is Year 3 of a recognized bull cycle, not Year 1. The supercycle narrative is consensus, not contrarian.

Scale in rather than full allocation: 50% position here, remaining 50% on any pullback to $43-44. If no pullback materializes within 90 days and the thesis holds, complete the position. Don’t wait indefinitely for an entry that may never come.

Monitor three metrics quarterly. Correlation with SPY during risk-off episodes—if GUNR drops more than SPY, the hedge thesis is broken. DXY trajectory—above 108 creates meaningful FX headwinds. Upstream capex guidance—if 2025-2027 spending accelerates 20%+ year-over-year, exit.

The thesis breaks if dollar rallies above 110 for two quarters, global recession triggers 10%+ demand destruction, or management teams abandon capital discipline.

GUNR works as 5-10% of a portfolio for investors with genuine conviction in real-asset outperformance. It doesn’t work as a core holding or defensive hedge. Know what you own.