Everyone’s Chasing LUNR, PNG and MDA — The Real Money’s Hiding in the Wreckage

When the space trade fits on one slide, someone is already the exit liquidity

Why This Crowded Space Trade Matters Now

The space / drones / defense basket has quietly become the same trade on repeat.

Different YouTube thumbnails, same portfolio: big slug of Intuitive Machines (LUNR), fat position in Kraken Robotics (PNG), anchor in MDA Space, maybe a bit of CAE for respectability. Everything else? “Broken.” “Garbage.” “Uninvestable.”

When three independent analysts land on almost exactly that same mix, that is not insight. That is crowding.

And crowded trades have a very specific habit:

The sexy names broadly disappoint, while the ignored, slightly embarrassing holdings do the heavy lifting.

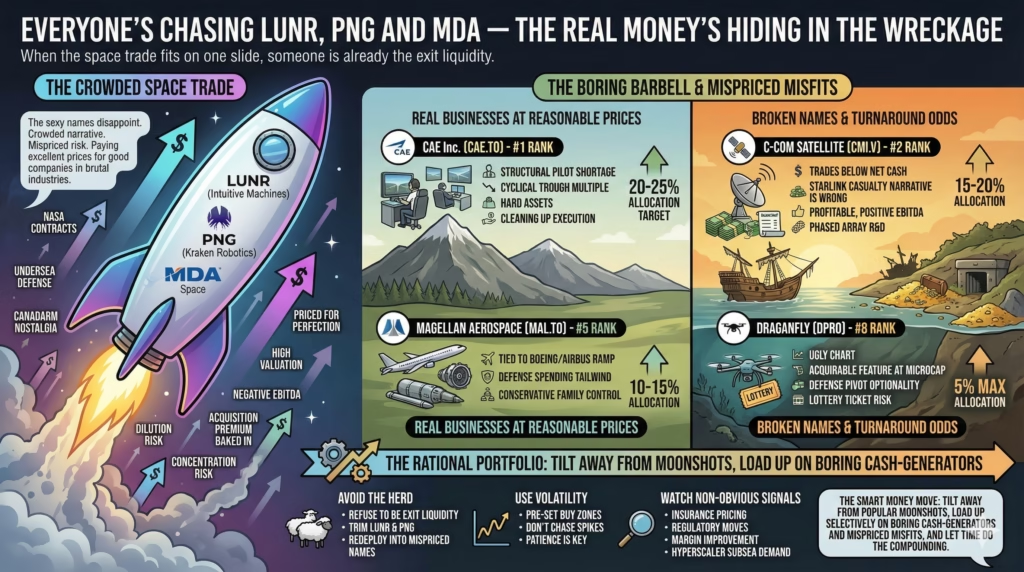

Across this small Canadian‑heavy universe — CAE, MDA, Kraken, C‑COM, Magellan, FTG, the drone misfits — the best risk‑adjusted five‑year outcome does not come from maxing out LUNR and PNG. It comes from a boring barbell:

- On one side, real businesses at reasonable prices (CAE, Magellan, even MDA at a sane size)

- On the other, ugly, written‑off “broken” names with non‑zero turnaround odds (C‑COM, Draganfly)

The cislunar economy is real. Undersea defense is real — and still weirdly underappreciated outside a few NATO planning rooms. NATO budgets are not going down; Boeing and Airbus are not scrapping their order books.

Prices matter more than slogans. Right now the obvious winners are priced like the future is guaranteed, while a couple of ignored tickers trade below what a mildly irritated liquidator would accept in a fire sale.

This isn’t a story about “space stocks”. It’s a story about crowded narratives, mispriced risk, and why the unloved tickers might quietly eat the consensus darlings’ lunch over the next five years.

How This Turned From Discovery to Groupthink in One Market Cycle

The original pitch was fresh.

- Russian tanks hit Ukrainian minefields

- Quadcopters become artillery spotters

- Starlink shows up in every war room PowerPoint

- NASA actually lands private hardware on the moon

Suddenly, three niche corners — space infrastructure, subsea robotics, defense drones — stop being hobby topics and become “the future of warfare and connectivity.”

Fast forward one year:

- LUNR becomes the de‑facto “SpaceX proxy” for public markets

- Kraken turns from obscure microcap to “every defense fund’s cute small‑cap”

- MDA is the responsible boomers’ pick: growth, backlog, Canadarm nostalgia

The portfolio many “advanced retail” and small funds now run looks like:

- 30–40% LUNR

- 25–35% Kraken

- 15–20% MDA

- A dash of CAE or Magellan as ballast

- Everything else ignored or mocked

That pattern is the tell. When the same three tickers dominate every deck, the marginal buyer is no longer early. The marginal buyer is the last one in.

There is a reason old‑school portfolio managers still remember who crowded into Nortel or pot stocks; the muscle memory of everyone loving the same thing at once tends to linger longer than the charts.

The danger isn’t that these are bad companies. They’re mostly good. The danger is paying excellent prices for good companies in brutal, cap‑intensive industries, while ignoring decent companies priced like they’ve already failed.

The Market’s Favorite Toys: LUNR, PNG and MDA Under the Harsh Light

LUNR: A Moon Landing, an IDIQ, and a Valuation Floating in Low Earth Fantasy

The LUNR bull case practically sells itself:

- Successful (ish) lunar landing

- NASA contracts with headlines like “up to $4.8B”

- The only pure‑play cislunar infrastructure company most investors can actually buy

Underneath the marketing:

- That “up to $4.8B” Near Space Network award is an IDIQ contract

- Indefinite Delivery, Indefinite Quantity

- NASA is obligated to almost nothing; real call‑offs will be a fraction

- The IM‑1 mission “success” was partial

- Soft landing? Yes

- Lander tipped over, limiting mission life and power

- Good enough for the stock; less good for insurers and risk models

At a share price around US$12–14 in mid‑2025, the market is paying something like:

- Roughly 15–20x trailing revenue

- Still negative EBITDA

- A capital‑intensive, government‑dependent business that will need fresh equity every time the moon blinks

Worse, the share count story is ugly:

- ~85M basic shares

- ~140M fully diluted

- Warrants, convertibles, recurring capital needs

- Over five years, another 50–100% dilution is not a wild scenario

So any “this could 5x” fantasy needs to be cut by a factor of 2 just on share count creep. And that’s before remembering that NASA can and will hand missions to multiple providers, and that SpaceX absolutely dominates launch economics and mindshare.

Risk is one‑sided:

- Downside: one failed mission, one funding wobble, one nasty secondary — very easy to see LUNR -60%

- Upside: mathematically capped by dilution and government margins

A spot in the portfolio? Yes. A 15% max position in an aggressive sleeve seems sane. The 35–40% allocations floating around look more like gambling than portfolio construction.

Kraken Robotics (PNG): When “Hidden Gem” Becomes House View

Kraken is genuinely impressive:

- Synthetic aperture sonar that can spot items the size of a soda can on the seabed

- NATO navies actually using it for mine countermeasures

- A sensible mix of product, services, and IP

The tailwinds is real:

- Post‑Ukraine, underwater mine hunting and port security budgets are up

- Denmark, Norway, the UK and others are leaning into unmanned naval systems

- NATO in 2024 said over 20 allies now meet the 2% of GDP defense spending target, up from only 3 in 2014 — that money goes somewhere, and underwater robotics is a trend, not a fad

But the stock did its move already.

From late 2024 into mid‑2025, Kraken roughly doubled. At C$3.50–4.00, investors are paying:

- 5–6x trailing revenue

- 25–30x on early EBITDA

That’s not “discovery stage”. That’s priced‑in enthusiasm.

The real risk is concentration:

- Denmark is about 40–50% of revenue

- One delayed tender, one election, one procurement “re‑baseline” and earnings can cave in

Acquisition fantasies don’t rescue this. Big defense primes often buy niche tech at 3–4x revenue. Kraken is already trading above that. An acquirer overpaying the market would be doing shareholders a favor, not writing a check at a typical M&A premium.

Kraken still deserves a place, but as a 15–20% position at most, ideally bought on a bad headline, not at peak consensus excitement.

MDA Space: The Patriotic Compounder That’s Quietly Fully Valued

MDA is the opposite of “story stock”:

- Actual history: Canadarm on the Shuttle and ISS

- Real backlog: C$5B+, including Canadarm3 for the Lunar Gateway

- Involved in satellite constellations like Globalstar’s partnership with Apple’s emergency SOS

On paper, it’s the safe name:

- Canadian, strategic, politically important

- Wins in robotics, Earth observation, satellites

On price, it’s much less safe.

At C$25–28:

- P/E: ~35–40x trailing

- EV/EBITDA: ~20–22x

- EV/Revenue: ~4.5–5x

That might be tolerable for a software company with fat margins. MDA is a hardware and services contractor selling into governments who bargain like Soviet wholesalers.

And several icebergs sit just under the surface:

- Lunar Gateway delays keep sliding revenue recognition for Canadarm3

- Constellation price pressure from Starlink, Kuiper and others crimps returns

- Canada could easily designate MDA as a “strategic national asset”

- Helpful for downside — less chance of going bust

- Harmful for upside — acquisition caps, political interference, limit to how “hot” the story can get

This looks like a 10–12% annualized return stock from here — respectable, not thrilling. It anchors a portfolio, but the expectation should be “durable mid‑teens” not “10‑bagger.”

A 15–20% position makes sense for stability and optional upside, but not at the cost of starving cheaper ideas.

The Stuff Nobody Brags About Owning — Where the Mispricing Lives

C‑COM Satellite (CMI.V): The “Starlink Casualty” That’s Quietly Cash‑Rich

The market’s story about C‑COM is simple:

“Starlink makes their satellite antennas obsolete. Value trap. Next.”

The balance sheet disagrees.

Recent numbers roughly line up as:

- Market cap: C$35–40M

- Net cash: C$25–30M

- Enterprise value (EV): about C$5–15M

- Revenue: C$15–20M

- EBITDA: C$2–4M, solidly positive

So the market is valuing:

- A real business, with real clients, at 0.25–0.5x revenue and 2–4x EBITDA on an EV basis

- While more than half the market cap sits in cash and securities

According to the company’s own disclosures, C‑COM sells auto‑pointing satellite antennas used on vehicles, ships, and remote sites. These work with any compatible satellite system — GEO, MEO, or LEO. Starlink is not a direct competitor so much as an extra pipe that can run through C‑COM hardware.

Three key points the market glazes over:

- Starlink’s flat terminals hate motion

- They’re amazing for fixed sites, challenging on fast‑moving platforms

- Military and emergency users still want stable, multi‑orbit connectivity

- Governments like redundancy

- NATO and allied militaries rarely want a single‑vendor, single‑constellation dependency

- Having C‑COM‑style systems gives optionality they can point at different birds in different orbits

- Next‑gen phased arrays

- C‑COM has R&D underway on electronically steered antennas designed for the LEO world

- If that works, the business could be structurally more valuable; if it fails, the cash pile still exists

Even in a pessimistic scenario where revenue grinds sideways and the product never re‑rates, the cash acts like a floor. Permanent capital loss from current levels would require either overt capital destruction or outright fraud.

CMI is the rare situation where the balance sheet and cash flows fully justify the price, and any operational success is a free call option. That’s exactly what mispriced asymmetry looks like.

A 15–20% allocation in a diversified “space & defense” basket is very defensible.

CAE Inc. (CAE.TO): Hated, Boring, and Possibly the Best Setup of the Lot

CAE doesn’t tweet pictures of rockets or submarines. It just trains pilots.

According to Boeing’s 2023 Pilot and Technician Outlook, the world will need about 649,000 new pilots between 2023 and 2042. That’s not hype from CAE’s investor deck; that’s from a major aircraft OEM that desperately wants its planes to keep flying.

CAE is one of only two serious players in full‑flight simulators (the other being L3Harris). That’s a duopoly built on regulation, training standards, and capital intensity. People will absolutely argue about which drone to buy; nobody cares if their simulator is a quirky startup.

So why is the stock still down 50%+ from 2021 highs?

- Fixed‑price defense contracts hammered margins

- Healthcare simulation expansion fizzled

- Execution looked sloppy; institutions lost patience

New management has been cleaning this up:

- Exiting the underperforming healthcare segment

- Re‑basing defense contracts and chasing better‑structured work

- Riding the global airline recovery as traffic exceeds 2019 levels in many regions

Valuation around mid‑2025:

- P/E: ~12–14x forward

- EV/EBITDA: ~8–10x

- Price/book: ~1.2–1.4x

Historically, CAE has traded closer to:

- 20–25x earnings

- 12–15x EV/EBITDA

Nothing in the structural business has broken enough to justify a permanently lower multiple:

- The pilot shortage is baked into demographics and fleet data

- Simulators and training centers are hard assets; not vaporware

- Regulators are not suddenly allowing “YouTube‑trained 737 captains”

If CAE simply:

- Returns to historical margins, and

- Trades back to mid‑cycle multiples on 2027 earnings

…the stock can roughly double.

Downside likely sits around tangible book and replacement value of the asset base, in the low C$20s — maybe C$18–20 on real stress.

For a five‑year horizon, CAE looks like the best risk‑adjusted idea in the entire group, and arguably deserves 20–25% of the portfolio.

Target allocation for aggressive but sane portfolio: 20–25%.

Magellan Aerospace (MAL.TO): The Sleepy Supplier That Just Grinds Higher

Magellan is nobody’s favorite stock, which is fine. It quietly supplies components to Boeing, Airbus, and defense customers and lets the OEMs handle the drama.

Global commercial fleets are aging. Airlines stretched aircraft lives during COVID, then discovered passenger demand came back faster than expected. Airbus and Boeing have both laid out aggressive production plans through the late 2020s; they need supply chains that can actually deliver.

Magellan sits in that chain.

At C$11–12:

- P/E: ~12–14x

- EV/EBITDA: ~6–8x

- Pays a 2%+ dividend

The Furfaro family owns nearly 80% of the company, which keeps the story off CNBC and discourages activists — but aligns incentives for patient compounding.

This isn’t a rocketship. It’s a compounder tied to global aerospace build rates and defense budgets.

If:

- Boeing and Airbus hit even the low end of their narrow‑body production targets, and

- Defense stays elevated post‑Ukraine and Gaza

…it is not hard to see 50–75% total return over five years here, mostly through earnings growth and a modest re‑rating.

Magellan works nicely as a 10–15% “boring ballast” in a portfolio otherwise stuffed with moon shots and underwater robots.

Draganfly (DPRO): The Ugly Chart With Respectable Optionality

Draganfly has already done almost everything a stock can do to offend shareholders:

- Huge drawdown (down ~95% from early peaks)

- Reverse splits

- Serial dilution

- Churn at the top

That’s exactly why it’s interesting at a market cap of US$20–25M.

At this size, a few things start to happen:

- The seller base is exhausted

- Almost everyone who wanted out has left

- The equity becomes an acquirable feature, not a problem

- Any mid‑sized defense contractor wanting drone capability can buy the whole thing for what amounts to petty cash

- Existence itself has value

- Many government tenders require competitive bidding from multiple qualified vendors

- Being “Bidder #2” in small UAS, even if rarely the winner, can still generate orders and contracts

The macro backdrop helps. According to open‑source assessments, Ukraine has been losing thousands of drones per month in periods intense fighting. Western militaries are watching closely and re‑writing doctrine around small UAS and loitering munitions. Long term, that’s an industry tailwind.

An extremely rough expected‑value sketch:

- ~40% chance Draganfly keeps muddling along: stock roughly flat

- ~30% chance the defense pivot works: 3–5x from microcap base

- ~15% chance of a takeout at a 50–100% premium

- ~15% chance it simply runs out of cash and dies

The weighted outcome is still positive, even after assuming a non‑trivial bankruptcy probability.

Sizing is everything. This is a textbook 5% lottery ticket: totally okay to lose, meaningful if it works.

Risk Isn’t Volatility, It’s Narrative Fragility

The biggest risk across this universe is not “the stocks go up and down.”

The biggest risk is owning a story that can break overnight.

A few examples:

- LUNR and the NASA illusion

- Many retail holders truly believe the “up to $4.8B” headline is locked‑in revenue

- One clear NASA statement about lower task orders or a mission failure, and that misunderstanding gets repriced instantly

- Kraken and Denmark

- If Danish defense spending reprioritizes, the narrative shifts from “NATO mine‑hunting champion” to “company that over‑indexed to one fickle customer”

- MDA and political risk

- A Canadian government decision to treat MDA as untouchable domestic infrastructure simultaneously protects the downside and quietly kills the “get taken out at 20x EBITDA” exit fantasy

By contrast, some of the ugly names have much less narrative to destroy:

- C‑COM does not rely on retail enthusiasm; it relies on cash, contracts, and a small but coherent product niche

- CAE’s story is built on math: fleet sizes, training regs, pilot demographics

- Magellan’s depends on OEM build rates and defense budgets, both visible years ahead

Volatility is not risk. Paying 6x revenue for a government contractor whose customers can cancel or delay on a whim — that’s risk.

The Signals That Actually Matter (And Mostly Get Ignored)

Insurance Pricing: Quiet Verdicts on LUNR and Friends

Every lunar lander, every subsea robot, every aerial platform has to be insured. Not for Reddit, but for underwriters.

Specialty insurers at places like Lloyd’s of London look at:

- Failure rates

- Recovery records

- Engineering practices

- Operator track history

If Intuitive Machines can show:

- Multiple missions with clean telemetry

- Safe abort behaviors

- Clear improvements from IM‑1’s tip‑over

…underwriters eventually cut premiums or offer better terms.

Lower insurance cost is real, compounding competitive advantage — and it rarely shows up in slide decks. Conversely, a serious mishap that looks like a design flaw can spike premiums and crush economics even if NASA stays friendly.

Watching how mission insurance evolves over the next few flights will say more about LUNR’s long‑term edge than the next earnings call.

Hyperscalers Underwater: Kraken’s Odd but Real Optionality

Microsoft’s Project Natick proved something quietly important: subsea data centers work. They’re efficient, secure, and politically attractive because they don’t consume prime coastal land.

If hyperscalers start planting underwater compute pods at scale, a new problem appears: who inspects and protects those assets?

Kraken’s sonar is built to:

- Find small objects on the seafloor

- Survey infrastructure

- Identify threats like mines

That same tech can easily pivot to:

- Subsea data‑center perimeter sweeps

- Cable route inspection

- Infrastructure monitoring “as a service”

This isn’t in anyone’s base case. Kraken is priced as a defense and offshore‑energy tool. But the value of a detailed, proprietary map of seabeds near major cables and future infrastructure could be huge… and invisible on today’s P/E.

The SpaceX Umbrella Over LUNR

LUNR’s valuation floats partly on a simple fact: public investors cannot buy SpaceX.

So anything that smells like “moon”, “lunar”, “cislunar logistics” gets some of that trapped demand.

This has several implications:

- Every Starship success pumps enthusiasm for “space infrastructure” generally, and LUNR catches a sympathy bid

- Every spectacular Starship failure makes timelines look longer and heightens perceived risk

- A SpaceX IPO, or even a large secondary listing, would likely vacuum up that “space premium” and leave LUNR trading on more sober contractor multiples

Owning LUNR today is also a side bet on SpaceX staying private for longer than people expect.

Regulation as a Hidden Moat

Regulators can create or destroy moats overnight.

Some plausible moves to watch:

- FAA / international “licensed lunar operator” frameworks

- If early landers get quasi‑exclusive licenses or narrow technical certifications, latecomers face brutal catch‑up costs

- NATO underwater mine‑hunting standards

- If Kraken’s SAS gear ends up embedded in the reference standard, future tenders are written in its language

- Spectrum and satcom rules

- C‑COM’s ability to play across GEO, MEO, and LEO depends on evolving spectrum decisions and licensing practices

In all of these, the first few regulatory decisions can lock in advantage or obsolescence for a decade. Quarterly financials won’t show it until much later.

Ranked: 5‑Year Risk‑Adjusted Potential Across the Space & Defense Set

This is where everything above collapses into something blunt: who probably gives the best bang for the risk taken over five years?

CAE Inc. (CAE.TO) — Rank #1

- Base 5‑year IRR: 15–20%

- Bull case: 25–30%

- Bear case: -15%

- Attractive entry: ~C$25 or below

Why it ranks first

- Structural pilot shortage (Boeing’s 649k‑pilot estimate) = 20‑year tailwind

- Capital‑intensive, regulated duopoly = real moat

- Trading at a cyclical trough multiple with cleaning up in progress

- Hard assets (simulators, centers) underpin valuation

Key risk

Another execution stumble in defense would torpedo the “new regime” credibility and could delay the re‑rating by years.

Target allocation in an aggressive but sane portfolio: 20–25%.

C‑COM Satellite Systems (CMI.V) — Rank #2

- Base 5‑year IRR: 20–30% (from a very low base)

- Bull: 50%+

- Bear: -20%

- Attractive entry: sub‑C$1.60

Why it ranks second

- Trades at or below liquidation‑style levels once net cash is deducted

- Profitable, positive EBITDA, no existential cash crunch

- Market misunderstood: Starlink is a potential partner/pipe, not definitive executioner

- R&D in phased arrays gives upside beta to the LEO boom

Key risk

Execution on the tech pivot could fizzle, leaving a slowly shrinking legacy antenna business.

Size: 15–20%, especially in accounts that can tolerate micro‑cap illiquidity.

Kraken Robotics (PNG.V) — Rank #3

- Base 5‑year IRR: 12–18%

- Bull: 25%+

- Bear: -40%

- Attractive entry: ~C$3.00 or lower

Why it still ranks high

- World‑class synthetic aperture sonar and a real install base across NATO navies

- Structural subsea defense demand in a world that is suddenly obsessed with mines, cables, and underwater infrastructure

- Optional upside from non‑defense markets (offshore wind, subsea data centers, infrastructure monitoring)

Key problems

- Denmark is still uncomfortably large as a revenue share

- The stock has already re‑rated hard; multiple compression is a real risk if growth wobbles

- Acquisition premium mostly priced in

Positioning: 15–20%, but ideally built on dips or bad‑headline days, not at peak consensus euphoria.

MDA Space (MDA.TO) — Rank #4

- Base 5‑year IRR: ~10–12%

- Bull: 18–20%

- Bear: -30%

- Attractive entry: low C$20s

Why it sits in the middle

- C$5B+ backlog + Canadarm heritage = durable business, not a fad

- Exposure to multiple core themes: space robotics, Earth observation, constellations

- Reasonable chance of modest multiple compression but decent earnings growth

Key drags

- Starting valuation is rich versus other government contractors

- Lunar program delays and constellation margin pressure limit upside

- Potential “strategic asset” status caps takeover fantasies

Role: 15–20% “core” position for stability and real but not spectacular returns.

Magellan Aerospace (MAL.TO) — Rank #5

- Base 5‑year IRR: 10–15%

- Bull: 20%+

- Bear: -20%

- Attractive entry: ~C$10–11

Why it deserves more respect

- Tied into Boeing/Airbus production ramp, which is telegraphed years ahead

- Benefits from elevated NATO and allied defense spending

- Conservative family control supports long‑term, not quarter‑to‑quarter, thinking

Risks

- If aircraft delivery issues (like Boeing’s ongoing quality mess) turn into a deep, prolonged downturn, Magellan will feel it

- Illiquidity and low public float can exaggerate swings

Slot: 10–15% — the ballast that still compounds.

Intuitive Machines (LUNR) — Rank #6

- Base 5‑year IRR: somewhere around 8–15%, with wild paths to get there

- Bull: 3–4x from here if everything lines up and dilution is disciplined

- Bear: -70%

Why it isn’t higher

- Government contracts with misunderstood ceilings; real revenue will undershoot fan fiction

- Capital intensity + dilution = constant battle just to keep per‑share value flat

- Lunar access is strategic, but NASA’s incentives are to keep multiple suppliers alive

Where it still fits

- Real lunar flight heritage; learning curve advantage vs newcomers

- Strong optionality if a regulatory or technical moat emerges faster than expected

Sizing: 10–15% max, and only for capital that can stomach violent swings and real headline risk.

Firan Technology Group (FTG.TO) — Rank #7 (Honorable Mention)

Not deeply covered above, but worth a word.

FTG makes high‑reliability circuit boards and cockpit products for aerospace and defense. It’s small (~C$200–220M market cap), reasonably profitable, and benefits from:

- Increasing electronics content per aircraft and per platform

- Elevated defense electronics demand

Valuation has already crept up with the sector, keeping it out of the top tier, but it can still earn high single‑digit to low double‑digit annual returns with relatively moderate risk.

A 5–10% supporting allocation is reasonable for investors wanting more breadth in the aero/defense electronics niche.

Draganfly (DPRO) — Rank #8

- Base 5‑year IRR: conceptually 0–15%, but with a lottery‑like distribution

- Bull: 3–5x

- Bear: total wipeout

The math can work, but the path will not be fun. If there is room for a lottery ticket, it belongs here. If not, skip it with no guilt.

Suggested size: 5% or less.

Volatus Aerospace (FLT.V), Star Navigation (SNA.V), DEFSEC (DFSC)

These live in the “too illiquid / too structurally challenged” bucket:

- Thin float, wide spreads, operational questions

- Very hard to build or exit positions without being the market

- Even if the underlying idea is clever, the listed vehicle is flawed

Unless someone is running very small capital with very high tolerance for friction, these are better watched than owned.

The Trade That Follows

The comfortable move is to keep doing what everyone is already doing: overweight LUNR and PNG, sprinkle MDA on top, and call it the “New Space & Defense” sleeve.

Comfortable, but probably mediocre.

A more rational setup for a five‑year horizon, for an aggressive but not suicidal allocation, looks something like this (rough ranges, not prescriptions):

- 20–25% CAE — core compounder, best risk/reward

- 15–20% C‑COM — deep value with asymmetry

- 15–20% MDA — strategic, stable growth at a fair but not insane price

- 15–20% Kraken — high‑quality tech, sized below the consensus hero worship

- 10–15% Magellan — boring ballast tied to aircraft build cycles

- 5–10% LUNR — lunar call option with real downside if the story cracks

- 0–10% FTG — niche electronics exposure, depending on taste

- 0–5% Draganfly — only if total loss is acceptable

A few practical, slightly unromantic recommendations:

- Refuse to be the exit liquidity for consensus trades

- If everyone in your feed owns LUNR and PNG at 30% weights, your job is not to out‑enthuse them

- Trim those to single‑digit or low‑teens weights and re‑deploy into CAE, C‑COM, and Magellan

- Use volatility to your advantage, not as entertainment

- These are thin names; they will overshoot both up and down

- Pre‑set buy zones (for example: CAE below C$25, C‑COM below C$1.60, Kraken closer to C$3) and respect them

- Don’t chase spikes after a single contract headline

- Watch the non‑obvious signals

- Insurance terms on future lunar missions

- Denmark’s defense budget and Kraken’s geographic diversification

- Regulatory moves on lunar licensing, underwater standards, and satcom spectrum

- Evidence that CAE is actually lifting margins in defense, not just promising to

- Treat “lottery tickets” like scratch cards, not a retirement plan

- If Draganfly works, a 3–5x on a 5% sleeve moves the portfolio

- If it dies, the portfolio shrugs

- What the portfolio cannot survive is 50% LUNR + 30% PNG going wrong together

- Accept that some of the best trades feel embarrassing at the start

- Owning cash‑rich C‑COM while everyone tweets SpaceX memes will feel wrong

- Adding to CAE on another dull quarter will feel like ignoring better stories

- That discomfort is usually where excess return actually comes from

The space and defense build‑out is real and likely multi‑decade, the question is not whether to invest so much as how much to pay, where to take the risk, and how long to let the compounding actually work without getting shaken out by every contract headline.

Right now, the smart money move is almost painfully simple:

Tilt away from the popular moonshots, load up selectively on the boring cash‑generators and mispriced misfits, and let time — not Twitter — do the compounding.

This isn’t exactly rocket science, except when it literally is, but the market somehow forget.