$AMKR at 52-week highs: geopolitical hedge or valuation trap?

The market is pricing Amkor as an AI play when it should be valued as Taiwan insurance—and insurance policies have very different return profiles than growth stocks.

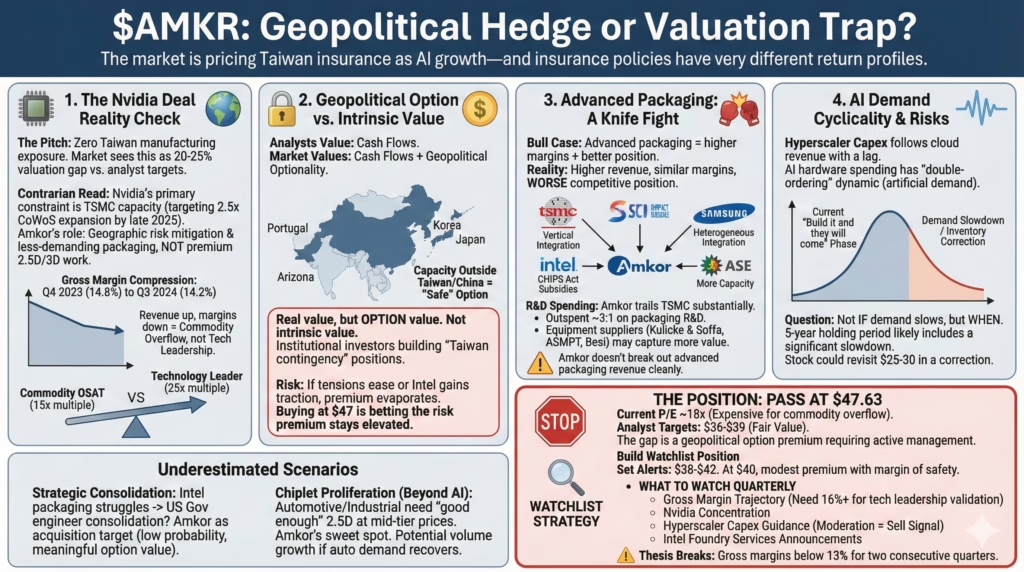

The pitch

Amkor is one of the only scaled Western-aligned advanced packaging companies with zero Taiwan manufacturing exposure. That’s a geopolitical hedge traditional DCF models can’t capture. The 20-25% gap between analyst targets ($36-39) and the current price ($47.63) isn’t stale research—it’s the market paying an option premium for “what if Taiwan gets disrupted.” If that premium persists or expands, Amkor delivers returns that have nothing to do with AI packaging volumes.

The friction

Gross margins have been flat to slightly down over the past two years despite supposedly winning advanced packaging business. That suggests Amkor is overflow capacity, not technology leader.

If geopolitical tensions ease or Intel’s U.S. packaging ambitions gain traction, the premium evaporates and the stock converges to analyst targets. That’s 20-25% downside from current levels.

Here’s what really drives this.

The Nvidia partnership is about diversification, not technology validation

The November rally treated the Nvidia news as proof Amkor can compete at the bleeding edge alongside TSMC’s CoWoS. The contrarian read: Nvidia’s primary constraint is TSMC capacity, and TSMC is expanding aggressively—targeting 2.5x CoWoS capacity by late 2025. Amkor’s role is almost certainly geographic risk mitigation and handling less-demanding packaging tiers. Not premium 2.5D/3D integration work that commands the highest margins.

The evidence supports this interpretation.

If Amkor were capturing premium advanced packaging, gross margins would already be inflecting upward. Instead, gross margins have compressed from 14.8% in Q4 2023 to 14.2% in Q3 2024. Revenue is growing, but the margin signature of commodity overflow is flat-to-down margins even as volume increases. This is the difference between a 15x earnings multiple (commodity OSAT with growth) and 25x (technology leader). Current price suggests the market is pricing closer to the latter.

Watch Q4 2024 and Q1 2025 margins closely. If gross margins don’t expand 50-100bps sequentially as Nvidia revenue ramps, the overflow thesis is confirmed. Amkor’s capex intensity also matters—if they’re reinvesting 80%+ of incremental revenue to maintain the relationship, shareholder returns will disappoint even with strong topline growth.

Analyst targets aren’t stale—they’re measuring something different

Wall Street analysts aren’t slow. They’re valuing cash flows while the market is valuing cash flows plus geopolitical optionality. Amkor has significant capacity outside Taiwan and China—facilities in Korea, Japan, Portugal, and an Arizona expansion underway. If Taiwan tensions escalate, or if customers simply want supply chain insurance, Amkor becomes dramatically more valuable as the “safe” option.

This is real value, but it’s option value, not intrinsic value. Options can expire worthless.

Institutional investors are increasingly building “Taiwan contingency” positions—hedging existing Taiwan-exposed portfolios rather than maximizing expected returns. This creates a bid under Amkor that isn’t visible in traditional valuation frameworks. The stock appears expensive on fundamentals because it’s serving a portfolio construction role that standard DCF ignores. Funny thing about geopolitical hedges—they work until suddenly everyone realizes they’ve been overpaying for insurance they didn’t need.

The risk: if geopolitical tensions ease, or Intel’s packaging services gain traction (eliminating Amkor’s “only Western alternative” status), the premium evaporates rapidly. A major Intel packaging win with a hyperscaler would be particularly damaging. Buying at $47 means betting the geopolitical risk premium stays elevated—that’s a different thesis than “AI packaging will grow.”

Advanced packaging is a knife fight with bigger competitors

The bull case assumes advanced packaging equals higher margins plus better competitive position. Reality may be messier: higher revenue plus similar margins plus worse competitive position.

TSMC is vertically integrating packaging. Intel is building packaging services with CHIPS Act subsidies. Samsung is pushing heterogeneous integration. ASE has more capacity and comparable technology. The “commoditized legacy” OSAT business actually had stable competitive moats; advanced packaging is an arms race against much larger, better-capitalized competitors.

Amkor’s R&D spending as a percentage of revenue trails TSMC substantially. If they’re being outspent 3:1 on packaging R&D, their technology position erodes regardless of current customer wins. The equipment suppliers—Kulicke & Soffa, ASMPT, Besi—may capture more value than the packaging providers themselves. This mirrors how ASML captured outsized returns in the fab equipment transition. Amkor’s capital intensity could increase faster than margins because they’re paying up for increasingly expensive equipment.

Customer concentration adds risk. If Nvidia becomes more than 15% of revenue, dependency increases substantially. And here’s the thing—Amkor doesn’t break out advanced packaging revenue cleanly. That’s itself telling. If it were growing rapidly and high-margin, management would trumpet it.

AI packaging demand is cyclical—just on a different cycle

Hyperscaler capex follows cloud revenue growth with a lag, and cloud revenue follows enterprise IT spending. The current “build it and they will come” phase doesn’t last forever.

AI hardware spending has the same double-ordering dynamic that plagued traditional semis: customers order more than needed to secure capacity, creating artificial demand that eventually corrects. The 2022-2023 semiconductor inventory correction caught many “secular growth” stories by surprise. The question isn’t if AI hardware demand slows, but when—and whether Amkor’s stock already embeds multiple years of growth that could compress into fewer years.

A 5-year holding period almost certainly includes at least one significant demand slowdown. Historical evidence shows OSAT operating leverage works both ways: margins compress sharply in downturns. Amkor could revisit $25-30 in a correction even if the long-term thesis remains intact.

Watch hyperscaler capex guidance from Meta, Microsoft, Google, and Amazon for 2025-2026. Any signal of moderation will hit AI hardware names regardless of Amkor-specific fundamentals. TSMC utilization rates remain the best leading indicator of advanced packaging demand.

The upside scenario: strategic consolidation or chiplet explosion

Two scenarios create asymmetric upside that bears underestimate.

First, if Intel’s packaging services struggle badly enough—likely given their challenges—the U.S. government faces a choice: let domestic packaging capability atrophy or engineer consolidation. Amkor, as the only other scaled Western-aligned option, becomes an obvious acquisition target. A government-blessed Intel acquisition at 40-60% premium is low-probability (20-30%) but meaningful option embedded in the current price.

Second, chiplet-based designs are proliferating beyond AI into automotive and industrial applications. These don’t need bleeding-edge CoWoS—they need “good enough” 2.5D integration at mid-tier price points. This is Amkor’s historical sweet spot: scaled, cost-effective, one or two nodes behind the frontier. Automotive and industrial customers sign longer-term contracts with more pricing stability than hyperscalers. If automotive semiconductor demand recovers in 2025-2026 and chiplet designs become standard for automotive compute… well, that’s volume growth from an unexpected direction that AI-focused analysts aren’t modeling.

The bear scenario matters too. Hyperscalers may bring packaging in-house for their highest-volume custom chips. Google has already made moves in this direction. Even the threat of vertical integration gives customers negotiating leverage that compresses margins.

The bottom line

Pass at current prices around $47.63.

The stock trades at approximately 18x forward earnings—reasonable for a technology leader but expensive for what’s likely an overflow capacity provider with flat margins. Analyst targets of $36-39 aren’t stale; they reflect fair value for the underlying business. The gap represents a geopolitical option premium that requires active management, not buy-and-hold conviction.

Build a watchlist position and set alerts for the $38-42 range. At $40, you’re paying a modest geopolitical premium while getting margin of safety if the option expires worthless. Alternatively, consider entering on any Q4 2024 earnings disappointment—if gross margins disappoint and the stock pulls back 15-20%, the risk/reward improves substantially.

Monitor quarterly: gross margin trajectory (need expansion to 16%+ to validate technology leadership), customer concentration (Nvidia exposure), hyperscaler capex guidance (any moderation is a sell signal), and Intel Foundry Services announcements. A major packaging win there invalidates Amkor’s “only Western alternative” thesis entirely. The thesis breaks completely if gross margins compress below 13% for two consecutive quarters—that confirms commodity overflow status with no path to margin expansion.