AeroVironment: the “wait for a crash” thesis is already costing you money

When everyone agrees a stock is highest quality but too expensive, someone’s math is wrong

The Pitch:

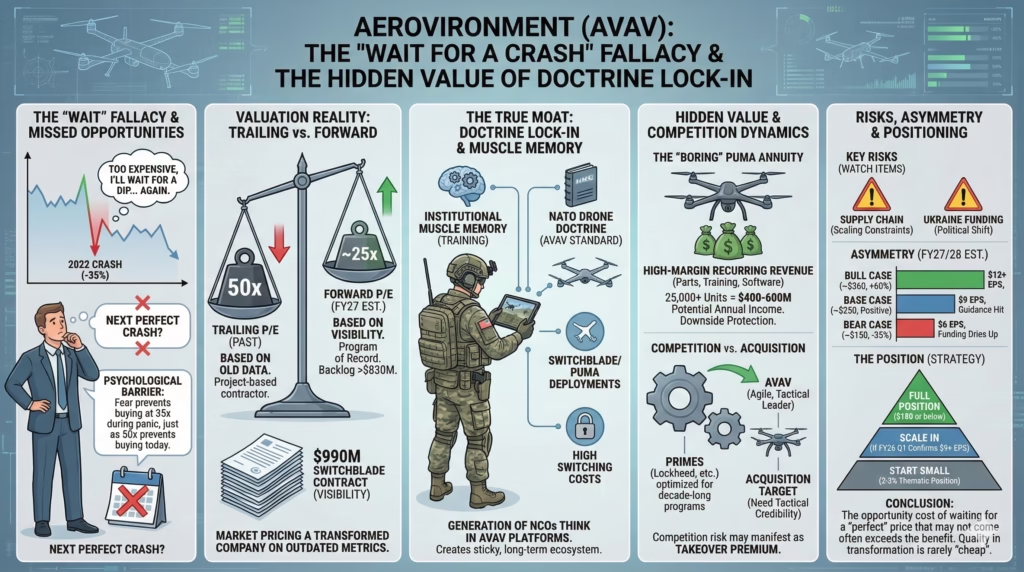

AVAV trades at 50x trailing earnings, triggering every disciplined investor’s “wait for a better entry” reflex. But the crash you’re waiting for already happened—and you didn’t buy then either.

The purgatory of admired stocks

AeroVironment sits in that uncomfortable space reserved for stocks everyone admires but nobody owns enough of. Purest play on tactical drone warfare. Combat-proven in Ukraine. ITAR-protected from Chinese competition. Program-of-record status with the U.S. Army.

The quality case writes itself. And yet.

At ~$230 per share and 50x trailing earnings, the plan becomes elegant: acknowledge quality, admire from afar, back up the truck when a crash delivers a 30-40% haircut.

Here’s the thing—that crash already happened. It was called 2022. AVAV fell 35% while fundamentals improved. If you didn’t buy when headlines screamed recession and defense stocks sold off with everything else, what makes you confident you’ll buy during the next panic?

The same psychological barriers preventing you from buying at 50x today will prevent you from buying at 35x when the world feels like it’s ending.

The valuation problem that isn’t

AVAV at 50x forward earnings sounds priced for perfection. Except that framing uses the wrong denominator.

Backlog exceeds $830 million. Management guides 17-20% organic revenue growth through FY2026. The $990 million Switchblade contract provides visibility tactical drone companies simply didn’t have two years ago. This isn’t a project-based contractor anymore—it’s a program of record with recurring characteristics.

Run the numbers forward. At FY2027 EPS of $8.50-9.50, AVAV trades at 24-27x earnings two years out. For ITAR-protected supply chains, 90%+ customer retention, and infrastructure-level importance to NATO drone doctrine, that’s reasonable. Not cheap. But not the nosebleed the “50x” headline suggests.

The market is using trailing metrics to value a company whose forward visibility has fundamentally transformed. This is pricing Netflix on DVD economics while streaming accelerated.

The doctrine lock-in nobody talks about

Bulls talk about Switchblade effectiveness. Bears talk about prime contractor competition. Both are focused on hardware.

Wrong lens.

The durable moat is that AVAV is becoming the de facto training and procedures integrator for NATO small-drone warfare. Every Puma certification, every Switchblade deployment, every Jump 20 mission creates institutional muscle memory nearly impossible to displace.

This is Palantir applied to physical systems: once your platform defines how soldiers conceptualize the mission, switching costs become astronomical.

The $990 million Army contract isn’t primarily about Switchblade revenue. It’s about locking in a generation of NCOs who think in AVAV platforms. When a 22-year-old infantry sergeant learns drone warfare on Switchblade, she carries that mental model for her entire career. She trains subordinates on AVAV systems. She writes doctrine assuming AVAV capabilities.

By 2027, AVAV could have 50,000+ trained operators across U.S. and allied forces. The consumables and support revenue from that installed base alone could justify 40% of current market cap in perpetuity. New hardware is gravy on an annuity.

Why 2022 doesn’t repeat

The pattern-matching objection: “AVAV fell 35% in 2022 despite improving fundamentals. I’ll wait for the next selloff.”

This contains a critical flaw. AVAV entered 2022 at 70x+ earnings on speculative Ukraine euphoria with zero contract visibility. The selloff was multiple normalization from absurd levels, not fundamental derating.

Today’s setup is inverted. AVAV sits at 50x trailing but ~25x on FY2027 estimates, with program-of-record backlog. Replicating 2022 requires the stock to first spike to 70x, then crash. That’s not a crash—that’s a round trip through a bubble that doesn’t exist.

In a 2025-2026 recession, AVAV’s government backlog becomes a relative safe haven. The stock might compress with the market, but less than consumer-facing growth names.

Why competition fears run backwards

Bears worry Northrop, Lockheed, and Raytheon will enter tactical drones at scale. This misunderstands prime contractor incentives.

A $50 million Switchblade program is a rounding error to companies optimized for $500 million+ aircraft programs. Their overhead structures and procurement processes are designed for decade-long development cycles, not 18-month platform refreshes. They’ve tried. They’ve failed. Repeatedly.

The real prime risk isn’t competing with AVAV—it’s being locked out of the tactical layer entirely as drone warfare becomes fundamental to ground combat.

This creates acquisition pressure where AVAV is target, not victim. If Lockheed needs tactical drone credibility for future Army contracts, AVAV is the obvious acquisition at 5-7x revenue. That’s $8-12 billion enterprise value versus today’s $6.3 billion. Competition risk may manifest as takeover premium.

The hidden revenue stream

Everyone focuses on Switchblade growth. Meanwhile, the 20-year-old Puma platform quietly generates AVAV’s most valuable asset: high-margin, low-volatility recurring revenue from parts, training, and software.

With 25,000+ Puma units across 50+ countries, each generating $15-25K annually in aftermarket revenue, the math points to $400-600 million in annuity-like income. This is the Gulfstream model: sell aircraft at modest margin, earn 3x the price over its life in support.

Even if Switchblade disappoints, the boring Puma business probably supports $4-5 EPS indefinitely. That’s downside protection embedded in a growth story.

What could actually break

Two risks deserve serious weight.

Supply chain constraints. Scaling from hundreds to thousands of Switchblade units requires proportional scaling of single-source sensors, guidance systems, and warheads. AVAV’s new Arizona facility addresses final assembly, but if a tier-2 supplier can’t scale, the company faces Boeing-style constraints. A single supplier failure could delay $200M+ in revenue.

Ukraine fatigue. The past two fiscal years benefited from ~$500 million in Ukraine supplemental funding. If U.S. politics shift toward “Europe funds its own defense” and supplementals shrink, that’s a 15-20% revenue headwind when the market expects acceleration. Allied orders are growing but probably not fast enough to offset a sharp Ukraine reduction.

These argue for scaling in rather than going all-in immediately.

The asymmetry

Bull case: Switchblade achieves standard NATO infantry status, counter-drone scales, AVAV becomes an acquisition target. At $12+ EPS by FY2028 and 30x multiple: $360. Roughly 60% upside.

Base case: Management hits guidance, operating leverage materializes. At $9 EPS by FY2027 and 28x: $250. Modest positive returns.

Bear case: Ukraine funding dries up, supply chain constrains scaling. At $6 EPS and 25x: $150. Roughly 35% downside.

More upside than downside. But bear case is real enough that sizing matters.

The position

Current price is reasonable for a thematic position. Not back-up-the-truck. Not hold-your-nose. The market’s valuation hesitation—driven by backward-looking multiples—creates a window before narrative catches math.

Start at 2-3% of portfolio. Double if FY2026 Q1 guidance (August 2025) confirms $9+ EPS trajectory. At $180 or below, move to full position. The $140 level some investors want probably requires a recession severe enough you won’t buy anyway.

Watch three things: supply chain commentary (any “challenges” or “delays” is a yellow flag), Ukraine funding developments in Congress, and prime contractor acquisition activity in tactical drones.

Everyone agrees AVAV is highest quality. Everyone waits for a better price. That price probably isn’t coming unless fundamentals deteriorate—at which point the quality thesis weakens anyway.

Sometimes the highest-quality name in a transforming sector is correctly priced as such. The opportunity cost of waiting may exceed the benefit of a slightly lower entry.