$TSE:CCO Cameco and the uranium bull market’s uncomfortable truth

The stock is simultaneously overvalued for 2026 and undervalued for 2029—patience determines who wins

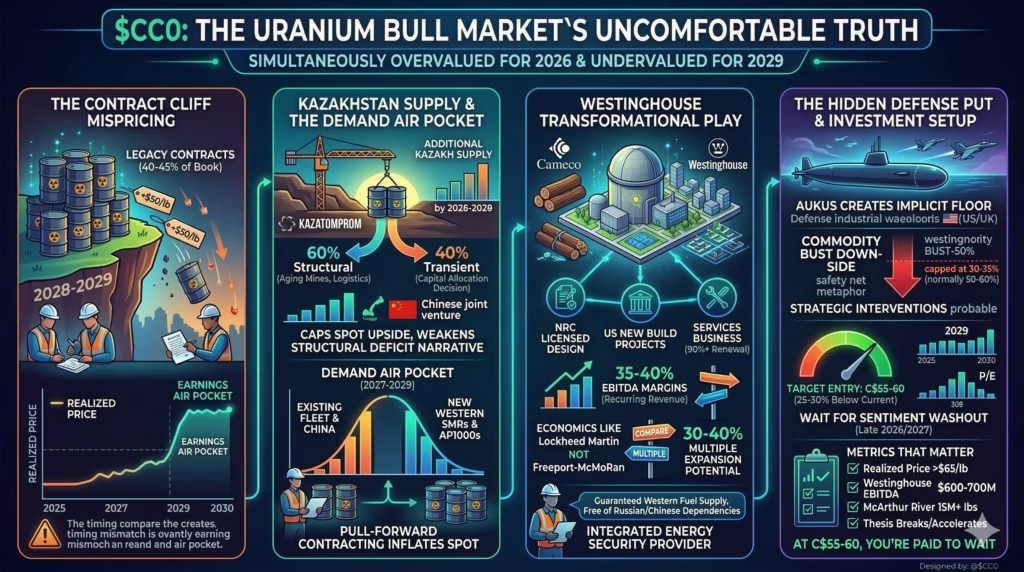

The pitch

Cameco owns the world’s highest-grade uranium deposits at a time when Western utilities are panic-buying fuel security. Good setup. But the market has completely mispriced the timing—40-45% of the contract book carries legacy pricing below $50/lb that doesn’t roll off until 2028-2029, creating an earnings “air pocket” that patient investors can exploit.

The Westinghouse acquisition transforms this from a commodity play into something closer to a defense contractor, with 35-40% EBITDA margin services revenue that no competitor can replicate. Wall Street is pricing smooth execution at 25-30x earnings while actual realized prices suggest the real inflection is 18-24 months away.

The friction

Kazatomprom’s production issues are 40% transient. If uranium sustains above $80/lb for another 24 months, expect 8-12M lbs of new Kazakh supply to hit the market by 2028. China’s domestic uranium production is targeting 35,000 tU by 2030—roughly triple 2020 levels—potentially transforming the world’s largest buyer into a net exporter. The 25-30x forward multiple leaves no margin for error on McArthur River’s ramp-up, which has already disappointed twice.

Here’s what really drives this investment case.

The contract book cliff nobody’s modeling correctly

Conventional wisdom says Cameco’s average realized price will steadily converge with $80+ spot uranium as legacy contracts roll off. The reality is far more binary.

Approximately 40-45% of committed volume through 2028 carries price ceilings established during the 2017-2021 trough—some reportedly as low as $40-45/lb. These contracts don’t roll off gradually. They cliff in 2028-2029 when several major utility agreements reach term simultaneously.

The practical math: Cameco’s average realized price likely improves from roughly $58/lb in 2025 to only $65-68/lb by 2027. Then it jumps to $78-85/lb in 2029-2030 as the book recontracts at current market rates. Management’s disclosures obscure this timing, but competitor Kazatomprom’s more detailed contract breakdowns confirm the industry-wide pattern. Utilities locked in decade-long supply agreements post-Fukushima when sellers were desperate.

This creates a specific problem for current shareholders. Investors expecting a steady earnings ramp will face disappointment through 2027. The stock could compress from current levels even as the long-term thesis strengthens. For new money, this timing mismatch is potentially a gift—but only if you buy after the sentiment washout, not before.

The evidence to watch: if Q1-Q2 2026 realized prices remain below $62/lb, the contract drag thesis is confirmed, and a better entry point lies ahead.

Westinghouse changes the math entirely

The market’s biggest analytical error is treating Westinghouse as dilutive to Cameco’s uranium leverage. The opposite is true.

Westinghouse transforms Cameco from a commodity price-taker into an integrated energy security provider with economics closer to Lockheed Martin than Freeport-McMoRan. Consider what Cameco now controls: the only NRC-licensed design for new US reactors (AP1000), three domestic new-build projects in various stages, and a services business with 90%+ contract renewal rates. This reminds me of how Halliburton evolved from pure oilfield services into something stickier—though that comparison only goes so far.

The services segment—refueling, maintenance, digital I&C upgrades—generates 35-40% EBITDA margins on recurring revenue. This isn’t mining economics. It’s enterprise software economics attached to 40-year reactor operating lives. When Vogtle Units 3 and 4 operate for their full licensed term, Westinghouse captures fuel fabrication, technical services, and component supply revenue measured in billions.

More critically, Westinghouse gives Cameco strategic leverage no competitor can match. The pitch to utilities becomes: “We guarantee your fuel supply from mine to reactor, entirely within Western supply chains, free of Russian or Chinese dependencies.” In a world where AUKUS submarine programs require reliable enrichment capacity and European utilities are scrambling to de-risk from Rosatom, this integrated offering commands premium pricing.

If the market eventually re-rates Cameco as energy infrastructure rather than commodity producer, there’s 30-40% multiple expansion available—independent of uranium spot prices. The trigger to watch: Westinghouse EBITDA contribution needs to reach $600-700M at Cameco’s 49% share by 2027 for this thesis to crystallize.

Kazakhstan’s supply isn’t as broken as the bulls need

The uranium bull case requires Kazatomprom’s production problems to be permanent. They’re not.

The breakdown is roughly 60% structural, 40% transient. Structural factors include aging ISR wellfields with declining grades, genuine sulfuric acid logistics constraints given Kazakhstan’s landlocked geography, and regulatory uncertainty around subsoil use extensions. These won’t reverse quickly. But the transient 40% represents a capital allocation decision, not a physical constraint. Kazatomprom could build more sulfuric acid capacity. They’ve chosen to conserve cash and let prices rise instead.

If uranium sustains above $80/lb for another 24 months, expect investment in acid capacity—likely with Chinese JV partners like CGN and Sinohydro who have strong incentives to secure supply. The math suggests 8-12M lbs/year of additional Kazakh production could return by 2028-2029.

This doesn’t break the long-term uranium thesis, but it does cap the upside on spot prices. The market has priced Kazakhstan’s roughly 10M lb/year underperformance as permanent. If half returns, the “structural deficit” narrative weakens materially. Cameco’s contract book becomes relatively more valuable—locked-in demand at good prices—but the spot price support erodes.

Watch Kazatomprom’s 2026 capex guidance for any acid capacity announcements. That’s your leading indicator.

The demand “air pocket” between 2027 and 2029

Nuclear demand follows a barbell distribution, not the smooth growth curve in analyst models.

The current surge is driven by three sources: existing fleet life extensions (immediate), China’s aggressive reactor program (ongoing), and new Western orders for SMRs and AP1000s (future). Here’s the problem—there’s a potential demand gap in 2027-2029 as these sources hand off.

Existing plants are already contracted for fuel. China’s domestic production is ramping faster than Western analysts appreciate—CNNC’s target of 35,000 tU domestic output by 2030 represents a tripling from 2020. And Western new-builds face 4-7 year construction timelines before they actually need fuel. The demand justifying current $80+ spot prices is partially pull-forward contracting by anxious utilities building strategic inventory, not immediate consumption.

If utilities complete their inventory builds by late 2026, the urgency premium in spot markets could deflate even as long-term fundamentals remain strong. This creates a confusing scenario where Cameco’s average realized price is finally rising—as legacy contracts roll off—just as spot prices are softening. The market could easily misread this as thesis deterioration rather than timing noise.

Track utility RFP volumes in H2 2026: if they decline 30%+ from 2025 levels, the air pocket is forming.

The hidden defense contractor “put option”

The AUKUS submarine program creates an implicit floor under Cameco’s business that almost no one is pricing.

AUKUS requires highly enriched uranium for naval reactors. While civilian reactors use low-enriched uranium, the supply chains overlap substantially at the mining and conversion stages. The US and UK defense establishments now have strategic interest in maintaining viable Western uranium mining, conversion, and enrichment capacity.

This isn’t speculation—it’s how defense industrial policy works. Steel, semiconductors, shipbuilding. If commercial uranium prices decline enough to threaten Western mining capacity, intervention becomes probable: strategic reserve purchases, production subsidies, or long-term defense contracts that cover civilian assets to maintain industrial capability. Cameco, as the only significant Western producer with operating tier-one assets, becomes “strategically important” in ways that create downside protection independent of commercial dynamics.

The asymmetry changes the risk calculation. In a normal commodity bust, Cameco’s stock might fall 50-60% from current levels. With the implicit defense put, downside is more likely capped at 30-35%—the point where strategic intervention becomes probable. This doesn’t guarantee returns, but it does improve the risk-adjusted math for patient capital willing to average into weakness.

The bottom line

Build a watchlist position and wait for the sentiment washout—likely comes in late 2026 or 2027 when the “air pocket” becomes visible and impatient uranium bulls capitulate. Target entry: roughly 25-30% below current (150$).

The metrics that matter: average realized uranium price (needs to break above $65/lb to confirm contract roll timing), Westinghouse EBITDA at Cameco’s 49% share (target $600-700M by 2027), and McArthur River production run-rate (must hit 15M+ lbs annually to meet delivery obligations without buying spot pounds). Monitor Kazatomprom’s capex announcements quarterly. Any sulfuric acid capacity investment signals the supply picture is shifting.

Thesis breaks entirely if: China becomes a net uranium exporter by 2030 (ceiling on prices at $60-70/lb), Westinghouse integration fails to generate promised synergies (EBITDA below $400M at 49% share by 2028), or a nuclear accident outside the Western fleet triggers regulatory contagion that delays new reactor orders. Conversely, the thesis accelerates dramatically if hyperscalers—Microsoft, Amazon—sign anchor tenant agreements for new Westinghouse reactors. That transforms Cameco from commodity cyclical to contracted infrastructure.