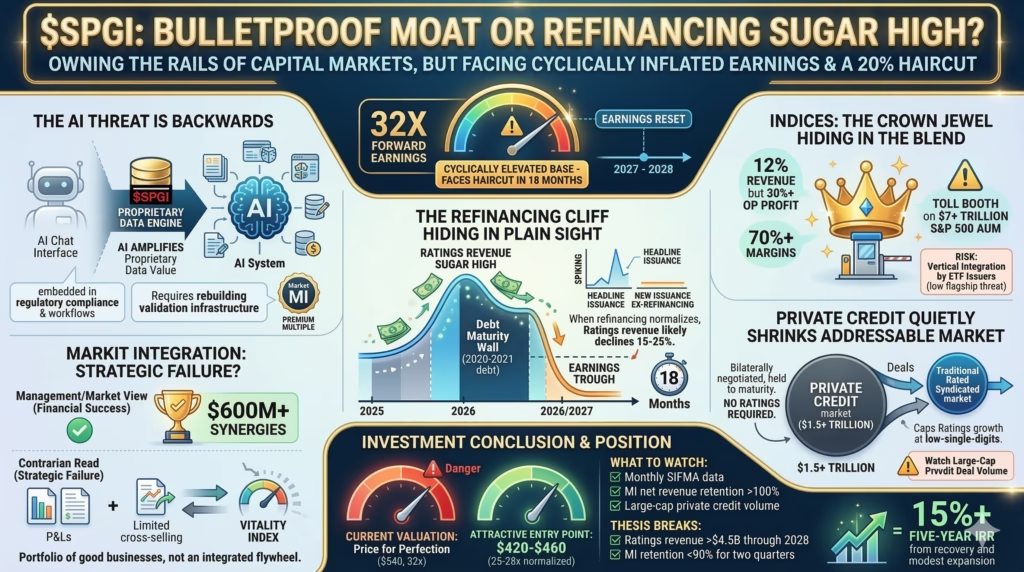

$SPGI at 32x earnings looks bulletproof, but the refinancing sugar high ends in 18 months

The market correctly loves the moat but is capitalizing cyclically inflated earnings that face a 20% haircut when the 2020-2021 debt wall finishes rolling over

The pitch

S&P Global owns the rails that global capital markets run on—credit ratings embedded in regulation, indices that define passive investing, and proprietary datasets that become more valuable as AI makes them queryable. The IHS Markit integration delivered $600M+ in synergies. The company now generates $5B+ in free cash flow annually with 45%+ operating margins. What the market misses: the “AI threat” to Market Intelligence is actually backwards—AI amplifies the value of proprietary data, and SPGI’s 50 years of credit histories and supply chain mappings are the training data moat, not the terminal interface everyone worries about.

The friction

Current Ratings revenue is artificially inflated by 20-30% from the historic refinancing wave of 2020-2021 vintage debt—$2.5 trillion that had to roll over. When this normalizes in 2027-2028, EPS likely drops 15-20% from peak levels.

At 32x forward earnings on a cyclically elevated base, the stock is priced for perfection with no margin of safety for the coming revenue cliff.

Here’s what really drives this.

The AI moat everyone has backwards

Consensus treats generative AI as an existential threat to Market Intelligence’s $5B+ terminal business. Bloomberg’s AI assistant, FactSet’s Mercury, and a parade of startups supposedly threaten to disintermediate SPGI’s data delivery.

This analysis inverts causality.

AI doesn’t compete with data—it amplifies the value of proprietary datasets. Anyone can build a chat interface. Almost no one has SPGI’s corporate credit histories spanning five decades, supply chain mappings from Markit’s procurement data, or evaluated pricing across 10,000+ commodity benchmarks. The terminal is increasingly legacy infrastructure. SPGI’s data already flows through APIs and feeds embedded in customer workflows. As financial institutions build AI-powered internal tools, they need more SPGI data feeds, not fewer.

Track “Data & Analytics” revenue growth within Market Intelligence versus Desktop revenue. If Data & Analytics accelerates while Desktop flattens—which early indicators suggest—the AI-as-tailwind thesis validates. Market Intelligence’s 95% net revenue retention should rise above 100% as AI features roll out.

The bear case points to interface commoditization driving pricing pressure. Customer CFOs under cost pressure can demand better terms regardless of switching costs. The counterargument: SPGI’s data is embedded in regulatory compliance and audit trails—ripping it out requires rebuilding validation infrastructure, not just swapping vendors.

Market Intelligence deserves a premium multiple, not a disruption discount. The segment is likely undervalued in SPGI’s sum-of-parts.

The refinancing cliff hiding in plain sight

Record 2025-2026 Ratings revenue isn’t evidence of competitive dominance—it’s a transitory sugar high.

Roughly $2.5 trillion of corporate debt issued during 2020-2021’s zero-rate environment has matured and refinanced over the past 24 months. This isn’t organic growth; it’s pull-forward activity leaving a hole in 2027-2028. SPGI’s own maturity wall data shows this clearly: five-year paper from 2020-2021 vintage required action in 2025-2026. Funny thing about debt walls—everyone sees them coming, but the market still manages to act surprised when they arrive.

Underlying new debt-funded M&A remains suppressed by elevated rates. Strip out refinancing activity from headline issuance data via SIFMA/Dealogic breakdowns: new issuance ex-refinancing is roughly flat while total issuance runs 20%+ above trend.

When refinancing normalizes, Ratings segment revenue likely declines 15-25% from 2026 peaks. At 32x forward earnings, the market capitalizes this elevated base as if it’s sustainable.

Bulls argue M&A will recover as rates stabilize, backfilling the refinancing hole. Some offset is likely. But the timing mismatch creates a 12-18 month earnings trough regardless. Ratings normalization is the highest-probability catalyst for a meaningful drawdown. The 2027-2028 earnings reset is baked in; only timing remains uncertain.

The Markit integration succeeded financially but failed strategically

Management declared victory: $600M+ synergies achieved ahead of schedule. The market moved on, treating the 2022 acquisition as fully digested and accretive.

The contrarian read: the synergy math worked but the strategic vision failed.

The original thesis combined S&P’s front-office data with Markit’s middle/back-office workflow tools to create an end-to-end platform. Reality delivered separate P&Ls with limited cross-selling. The “Vitality Index”—revenue from cross-sold products—featured prominently in 2022-2023 earnings presentations. It has quietly disappeared from recent disclosures. The Mobility segment (from Markit’s automotive data) grows below corporate average at mid-single-digits versus peers like Experian Auto posting low-double-digits.

The thing is, SPGI bought financial engineering—cost cuts plus multiple arbitrage—not transformative capabilities.

The bull case argues integration takes time and cross-segment opportunities will compound. Perhaps. But if multi-segment customer metrics never appear in disclosure, the platform thesis failed. SPGI trades at a “platform premium” it may not fully deserve. The company is a portfolio of good businesses, not an integrated flywheel with compounding network effects. Future M&A likely repeats this pattern: accretive on paper, strategically underwhelming.

The Indices business is the crown jewel hidden in the blend

Indices represents roughly 12% of revenue but generates 30%+ of operating profit at 70%+ margins. This is the highest-quality business inside SPGI: pure royalty stream on $7+ trillion of S&P 500-tracking AUM, growing automatically with passive investing adoption and market appreciation. No sales force required. No delivery cost. Just the toll booth.

The risk scenario worth monitoring: vertical integration by ETF issuers.

BlackRock already runs iShares factor and active ETFs on proprietary indices. At 3 basis points licensing cost on products targeting 5 basis points total expense ratios, the math eventually gets uncomfortable. BlackRock, Vanguard, and State Street collectively manage $15T+. If “BlackRock Large Cap” starts displacing “S&P 500” for institutional mandates—and this remains a real if distant possibility—the narrative of permanent index royalties cracks.

For flagship benchmarks, this threat remains low-probability. “Tracking the S&P 500” has brand value that alternatives can’t replicate. For factor, ESG, and thematic indices where S&P’s brand advantage is weaker, disintermediation already occurs.

Indices deserves a standalone multiple above the blended company. Watch for any major ETF issuer launching competitive large-cap benchmarks though.

Private credit quietly shrinks the addressable market

The $1.5 trillion+ private credit market—Ares, Blue Owl, Apollo, Blackstone—doesn’t use traditional ratings agencies. These deals are bilaterally negotiated, held to maturity, and require no ratings for distribution. As private credit takes share in middle-market lending, leveraged buyouts, and increasingly investment-grade financing (Apollo’s investment-grade private origination grew 40% in 2025), the volume of rated securities grows slower than total credit creation.

This is a slow bleed, not a cliff.

Private credit won’t displace public markets for mega-deals or investment-grade corporate issuance. But it caps Ratings growth at low-single-digits even if total credit creation runs at 5%+. The high-teens EPS growth consensus expects becomes mathematically difficult without margin expansion or aggressive buybacks.

Bulls argue private credit is complementary—sponsors eventually need public markets for exits. True for equity, less true for credit where refinancing can stay private. Watch large-cap private credit deals. If Apollo and Ares start financing $10B+ LBOs privately… well, the traditional rated syndicated market faces genuine structural pressure.

The bottom line

But 2027-2028 brings a near-certain earnings reset as the refinancing wave completes. A 15-20% EPS decline on any multiple compression creates 25-35% drawdown potential.

Wait for the Ratings normalization narrative to emerge in late 2026 earnings calls.

Key metrics to monitor: Monthly debt issuance data from SIFMA breaking out refinancing versus new issuance. Market Intelligence net revenue retention crossing above 100% validates the AI-as-tailwind thesis. Any disclosure of cross-segment customer revenue would confirm Markit integration finally delivering. Track large-cap private credit deal volume for the structural threat to Ratings addressable market.

Thesis breaks if: Ratings revenue sustains above $4.5B through 2028 (refinancing cliff doesn’t materialize), or Market Intelligence net revenue retention falls below 90% for two consecutive quarters (AI disruption thesis wins).