$COHR and the photonics bottleneck Jensen just made famous

The market sees a capacity crisis; the real opportunity is what comes after pluggables die

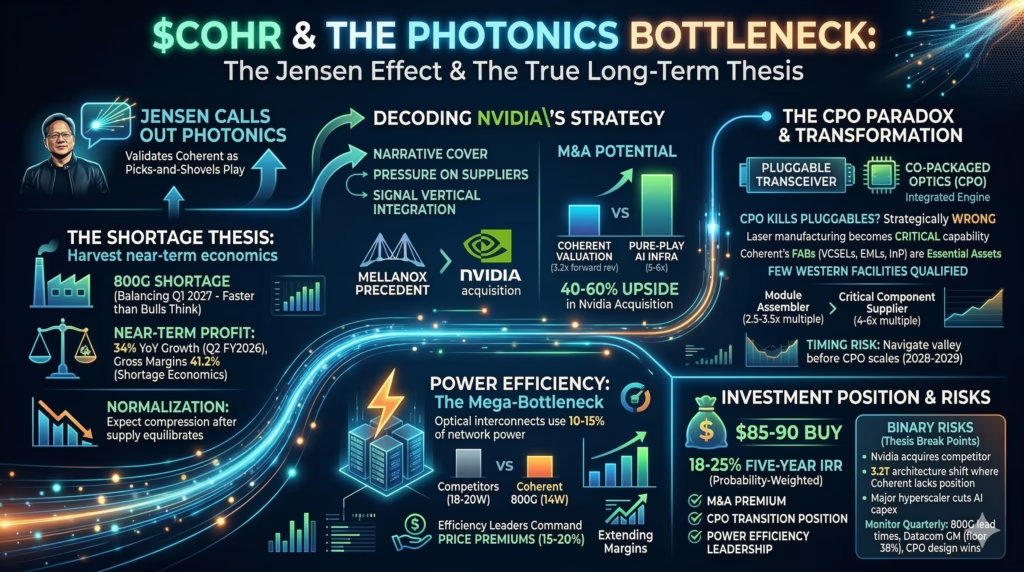

The pitch

Jensen Huang’s GTC 2026 call-out of photonics as NVIDIA’s binding constraint validates Coherent as the picks-and-shovels play on AI infrastructure scaling. But here’s the thing—the market is pricing in the wrong thesis. Coherent’s real value isn’t the current 800G/1.6T transceiver shortage (which eases by early 2027), but their indium phosphide and silicon photonics manufacturing capabilities that become essential when co-packaged optics replaces pluggables entirely. The bears think CPO kills Coherent; the contrarian reality is that CPO makes Coherent’s fabs strategic assets worth multiples of today’s pluggable-focused valuation.

The friction

The capacity shortage Jensen highlighted is a trailing indicator. Not a 3-year runway but a 12-18 month window before Lumentum, Broadcom, and others catch up.

If NVIDIA decides photonics is too strategic to leave to suppliers (their Mellanox playbook), Coherent’s “partner” status could become “acquisition target” or worse, “displaced vendor.” The 3.2T transition in 2027-2028 may require architectures where Coherent lacks positioning, turning today’s dominance into tomorrow’s commodity trap.

Time to examine what really drives this.

Why Jensen’s public call-out is strategic theater

Jensen Huang doesn’t make off-the-cuff comments about supply chains. His specific mention of photonics capacity serves three purposes: narrative cover for NVIDIA system price increases, pressure on optical suppliers to prioritize NVIDIA allocation, and potential signaling of deeper vertical integration to come.

When NVIDIA’s CEO publicly blames a component category, suppliers either get acquired, locked into long-term agreements, or face eventual displacement. The Mellanox precedent is instructive—NVIDIA identified networking as strategic, partnered initially, then bought the company for $7 billion in 2020. That pattern tends to repeat.

This creates an unusual risk/reward profile. Near-term, Coherent benefits from validation and likely preferential treatment from hyperscalers scrambling to secure supply. Medium-term, NVIDIA’s interest in “solving” the photonics problem could mean acquisition (bullish) or internal development (bearish). Current 800G transceiver lead times run approximately 16 weeks. If NVIDIA signs long-term supply agreements that guarantee Coherent capacity but cap pricing, the upside is limited. If they acquire a competitor instead, Coherent’s moat narrows.

The bull case here is M&A optionality—Coherent trades at roughly 3.2x forward revenue versus 5-6x for pure-play AI infrastructure names. An NVIDIA acquisition at even a modest premium to AI comps would generate 40-60% upside. The bear case is that NVIDIA’s attention accelerates competitive entry and commoditization. Watch for any NVIDIA patent filings, job postings, or investments related to photonics in the next two quarters.

The capacity shortage is real but shorter than priced

The mainstream bull thesis assumes photonics constraints persist through 2028, giving Coherent sustained pricing power and 40%+ gross margins on AI-related revenue. The evidence suggests a tighter timeline.

Jensen’s public acknowledgment is itself a signal—by highlighting the bottleneck at GTC, he’s telling his supply chain to ramp aggressively and giving hyperscalers cover to dual-source. Lumentum, Broadcom’s optical division, and legacy II-VI competitors are all adding capacity simultaneously.

Coherent’s datacom segment delivered 34% year-over-year revenue growth in Q2 FY2026, with gross margins expanding to 41.2% from 37.8% a year prior. These are shortage economics. But 800G transceiver supply-demand likely balances by Q1 2027—much faster than the 36-month runway bulls model. For context, the 400G shortage in 2022-2023 lasted approximately 14 months before capacity caught up and margins normalized. History suggests gross margins compress 300-400 basis points once supply equilibrates.

This doesn’t kill the thesis—it reframes it. The near-term is about harvesting shortage economics while they last. The 5-year thesis requires believing in something beyond the current bottleneck, which brings us to the co-packaged optics opportunity everyone is getting backwards.

The CPO paradox: why bears are wrong about Coherent’s obsolescence

Consensus bears argue that co-packaged optics—where optical engines integrate directly onto switch ASICs rather than plugging in as separate transceivers—represents an existential threat to Coherent’s pluggable business.

This analysis is directionally correct but strategically wrong.

When optics move from pluggable modules to integrated engines, laser manufacturing becomes the critical capability. Coherent’s VCSELs, EMLs, and indium phosphide epitaxy fabs—currently nice-to-have advantages in pluggables—become essential strategic assets. It’s a bit like the hard drive to SSD transition; the component suppliers who understood where the value was migrating did fine. The ones who didn’t… well, that’s a different story.

Broadcom and Marvell, the likely CPO architecture drivers, don’t manufacture lasers. They’ll need partners. Coherent’s fabs in Pennsylvania and Germany are among the few Western facilities qualified for high-volume photonic component production. Chinese suppliers face export control barriers for these exact components. The market values Coherent on pluggable transceiver revenue multiples (2.5-3.5x forward sales). A CPO transition should command semiconductor-like multiples (4-6x forward sales) because it transforms Coherent from a module assembler into a critical component supplier with limited substitutes.

The risk is timing. CPO reaches volume production in 2028-2029, meaning 18-24 months where pluggable margins compress before CPO revenue scales. Coherent must navigate this valley without destroying margins or losing design wins. Their recent announcements of silicon photonics partnerships with undisclosed hyperscalers suggest awareness of this transition. Management needs to articulate the CPO roadmap more clearly in coming quarters.

Chinese competition is bullish, not bearish

The reflexive concern about Innolight, Eoptolink, and other Chinese optical suppliers misreads the competitive dynamics. Yes, Chinese suppliers are ramping 800G capability and will eventually reach 1.6T. But they primarily serve Chinese demand—Huawei Ascend clusters, Baidu, ByteDance, Alibaba’s domestic AI infrastructure. Every transceiver going to Chinese hyperscalers is capacity not competing for NVIDIA or Western cloud provider supply.

Chinese AI infrastructure is growing at 45%+ annually according to industry estimates, absorbing massive optical capacity. Export controls specifically target the high-speed optical components where Coherent leads, creating a regulatory moat for Western hyperscaler business.

The more realistic competitive threat is Innolight winning non-Chinese hyperscaler business (AWS, Google, Meta)—which hasn’t happened at scale for 800G and faces significant qualification barriers.

Watch for any Innolight or Eoptolink design wins with Western hyperscalers. Until that happens, Chinese competition is actually tightening Western supply-demand by absorbing Asian manufacturing capacity. Coherent’s Malaysia and Thailand operations give them Asian cost structures without the geopolitical baggage.

Power constraints create unexpected pricing power

Datacenter power is emerging as the next mega-bottleneck after GPU supply. Optical interconnects consume 10-15% of total networking power budget. A 2x improvement in optical efficiency is equivalent to building new datacenter capacity without construction delays or utility negotiations. This shifts purchasing criteria from “lowest cost per gigabit” to “lowest power per gigabit”—a fundamentally different competitive dynamic.

Coherent has invested heavily in lower-power optical engines through their LPO (linear pluggable optics) technology and next-gen DSP designs. Their 800G transceivers run at approximately 14W versus 18-20W for some competitors. At scale—say, 100,000 transceivers per major hyperscaler deployment—that 4-6W difference translates to megawatts of datacenter power savings worth millions annually in electricity costs alone.

If power becomes 30% of total datacenter operating cost (up from roughly 20% today), optical suppliers demonstrating efficiency leadership can command 15-20% price premiums. This extends Coherent’s margin runway beyond the capacity shortage window. Microsoft and Google have both publicly discussed power constraints on AI buildout—the demand signal is there. Coherent’s efficiency positioning is undersold in current investor communications.

The bottom line

The market is pricing in pluggable transceiver leadership during a capacity shortage—a 12-18 month thesis worth perhaps 15-20% upside. The undiscounted optionality includes CPO transition positioning (worth 30-40% upside if Coherent captures meaningful optical engine share), M&A premium potential (NVIDIA or hyperscaler strategic interest adds 25-40%), and power efficiency leadership (extends margin runway 2-3 years beyond shortage economics). Combined probability-weighted upside supports a 5-year IRR of 18-25%.

Key metrics to monitor quarterly: 800G transceiver lead times (concern if below 10 weeks, signaling shortage easing), datacom gross margins (floor at 38%, target above 40%), any CPO design win announcements, and NVIDIA supply agreement disclosures. Revenue mix matters—AI datacom currently represents roughly 35% of revenue but needs to reach 50% by FY2028 for the growth thesis to work.

Look, the thesis breaks if NVIDIA acquires a competitor (Lumentum, Ayar Labs) rather than Coherent, signaling displacement. Or if the 3.2T architecture shifts to technologies where Coherent lacks positioning. Or—and this is the big one—if any major hyperscaler announces significant AI capex reductions. The stock deserves a 20-25% position size in an AI infrastructure basket, not a concentrated bet. The binary M&A and technology transition risks are real. But at current valuations, the asymmetry tilts in your favor.