KRKNF / PNG.TO – Kraken Robotics at ~USD $6.30 / CAD $8.60: Pricing Ottawa, Missing Europe?

A small-cap subsea surveillance specialist caught between Canadian rhetoric and European urgency

What Kraken Actually Does — And Why This Moment Matters

Kraken Robotics (KRKNF in the U.S., PNG on the TSXV) designs and manufactures advanced subsea technologies, primarily Synthetic Aperture Sonar (SAS), autonomous underwater vehicle (AUV) systems, and subsea batteries. Its flagship systems — including KATFISH and AquaPix — are used for mine countermeasures, seabed mapping, infrastructure inspection, and naval surveillance.

This is not a diversified defense conglomerate. Kraken operates in a narrow but technically demanding segment: high-resolution subsea imaging optimized for small and mid-sized unmanned platforms. The differentiation lies less in raw scale and more in SWaP optimization — size, weight, and power efficiency — allowing deployment on smaller UUVs where larger prime systems are not practical.

Subsea infrastructure has moved up the strategic priority stack following Baltic Sea cable incidents and broader NATO reassessments of undersea vulnerability. Offshore wind, fiber cables, energy interconnectors and naval mine countermeasures all sit inside that same ecosystem.

The question for investors is not whether subsea matters. It clearly does. The question is whether Kraken’s positioning translates into durable contracts — and whether the current stock price already assumes that translation.

The pitch

Kraken operates in a strategically relevant niche at a time when NATO members are reassessing underwater surveillance gaps. Smaller unmanned systems are proliferating faster than large submarine-scale programs, and that dynamic favors suppliers optimized for modular deployment rather than massive platform integration.

Large incumbents such as Kongsberg and Thales dominate high-end and large-scale programs. However, not every procurement decision centers on maximum system scale. In specific cases — mine countermeasures, rapid seabed mapping, infrastructure inspection — deployment speed and modularity matter.

The market narrative currently emphasizes Canadian domestic procurement tailwinds. That may prove relevant over time, but the timeline likely extends beyond immediate budget cycles. European demand dynamics could evolve faster, but that path is conditional rather than embedded.

The friction

At ~USD $6.30 / CAD $8.60, Kraken trades at a growth multiple. Depending on which trailing revenue base is used, price-to-sales sits in the high-teens to low-20s range.

That valuation implies sustained double-digit revenue expansion with controlled margin normalization.

Execution risk centers on three areas:

- Margin compression during scaling from smaller production runs to higher volume output

- Customer concentration exposure

- Working capital expansion as inventory and receivables scale

Hardware businesses rarely scale in a straight line. Revenue growth can outpace operational efficiency improvements during expansion phases, temporarily compressing margins.

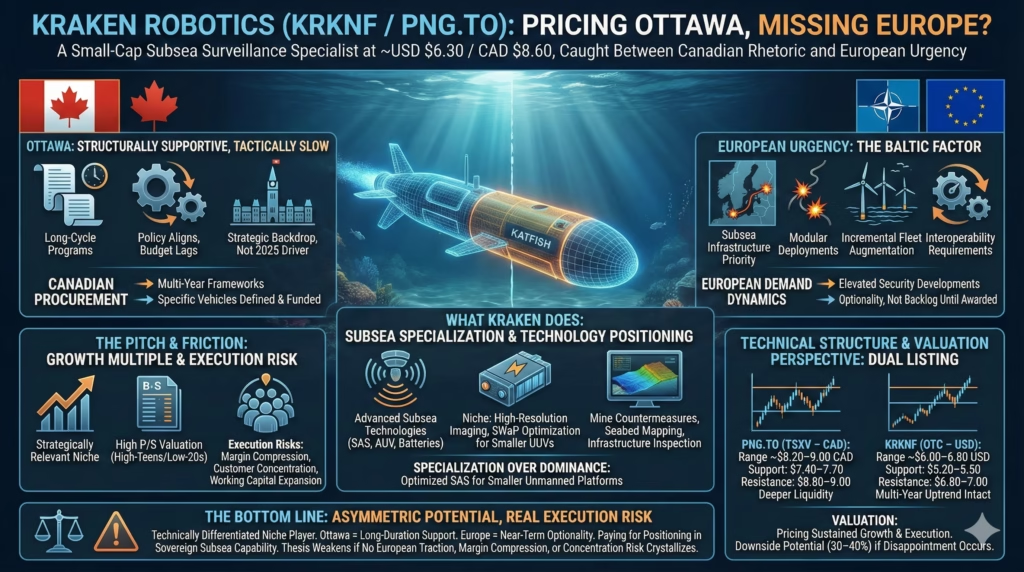

Ottawa: structurally supportive, tactically slow

Canadian defense policy signals greater domestic participation. That directionally supports national suppliers.

However, Canadian procurement operates within multi-year frameworks. Large naval and infrastructure programs remain embedded in long-cycle structures. Even when policy intent aligns, budget allocation and contract award velocity often lag public announcements.

For Kraken to derive material revenue from Canadian DND programs, specific vehicles must be defined, funded and executed. That is possible — but unlikely to represent a near-term catalyst.

Ottawa functions as a strategic backdrop, not a 2025 earnings driver.

The Baltic factor: acceleration, not bypass

European security developments have elevated subsea monitoring priority. However, emergency procurement does not eliminate interoperability requirements, alliance certification processes, or vendor qualification structures.

Where opportunity exists is in modular deployments, supplemental capability purchases, and incremental fleet augmentation rather than wholesale system replacement.

A meaningful European contract would validate Kraken’s position within NATO ecosystems. But until formally awarded, this remains optionality rather than backlog.

The technology positioning: specialization over dominance

Kraken’s moat is specific: optimized SAS integration for smaller unmanned platforms.

That does not position the company as a universal SAS leader across all naval programs. Instead, it situates Kraken within a fast-growing segment of smaller UUV proliferation — mine countermeasures, cable inspection, offshore energy, and coastal monitoring.

The addressable market expands as smaller autonomous systems become more common. Competitive intensity is lower than in submarine-scale programs, but so is total market size.

This is a defensible niche, not a broad-spectrum monopoly.

Defense spending dynamics: not purely zero-sum

The argument that subsea competes directly against AI, cyber, space or air defense oversimplifies budget structure.

Subsea infrastructure protection increasingly overlaps with national security and economic resilience categories, not purely conventional military allocations.

Autonomous underwater systems are themselves software-enabled platforms. AI integration is complementary, not competitive.

Spending flows shift across domains, but subsea has structurally moved higher on strategic priority lists.

Technical structure — dual listing (USD & CAD)

The structural trend is identical across both listings, but liquidity and execution differ.

Primary Trend (Both)

- Multi-year uptrend intact

- 50-day moving average above 200-day

- Higher highs and higher lows preserved

- No confirmed weekly breakdown

Current behavior resembles consolidation after a strong expansion phase rather than distribution.

KRKNF (OTC – USD)

Current range: ~$6.00–6.80 USD

- Major support: $5.20–5.50

- Secondary support: $4.20–4.40

- Resistance: $6.80–7.00

A weekly close above $7.00 on expanding volume would suggest continuation toward $8.00+. A weekly break below $5.20 would weaken structure.

PNG.TO (TSXV – CAD)

Current range: ~$8.20–9.00 CAD

- Major support: $7.40–7.70

- Secondary support: $6.00–6.40

- Resistance: $8.80–9.00

A weekly close above $9.00 could open extension toward $10.50–11.00. Breakdown risk increases below $7.40.

The Canadian listing provides deeper liquidity. The OTC listing may display wider spreads and sharper volatility reactions.

Entry and risk framework

Canadian investors (PNG.TO):

- Staggered entry: $7.60–8.20 CAD

- Pullback accumulation zone: $6.20–6.50 CAD

U.S. investors (KRKNF):

- Pullback entry: $5.30–6.00 USD

- Momentum confirmation entry: weekly close above $7.00 USD

Trend invalidation:

- Below $7.40 CAD

- Below $5.20 USD

Valuation perspective

At current levels, the market assumes sustained growth and operational discipline.

If margins normalize toward 40–45% and revenue growth moderates below 25%, multiple compression is plausible.

If revenue sustains 30%+ compounding with credible contract diversification, current valuation may prove justified.

This is not a distressed asset. It is a growth stock pricing execution.

In a disappointment scenario, downside of roughly 30–40% is plausible given historical small-cap hardware multiple compression cycles. Structural collapse is not implied, but volatility should be expected.

The bottom line

Kraken Robotics is a technically differentiated, niche defense technology company operating in a strategically relevant domain.

Ottawa provides long-duration narrative support. European developments provide nearer-term optionality.

The stock reflects execution expectations but does not fully embed confirmed European backlog.

This is a specialized growth exposure with asymmetric potential and real execution risk.

Position sizing and discipline matter.

The thesis weakens materially if:

- No meaningful European contract traction develops over the next several quarters

- Margins compress sustainably below 40%

- Customer concentration risk crystallizes without diversification

You are paying for positioning in sovereign subsea capability. That can justify exposure. It does not remove risk.