$KDEF: Korea’s defense industry is building a global manufacturing empire, not just a geopolitical hedge

The market treats Korean defense as a tension trade—it’s actually a Samsung-style industrial revolution in military hardware

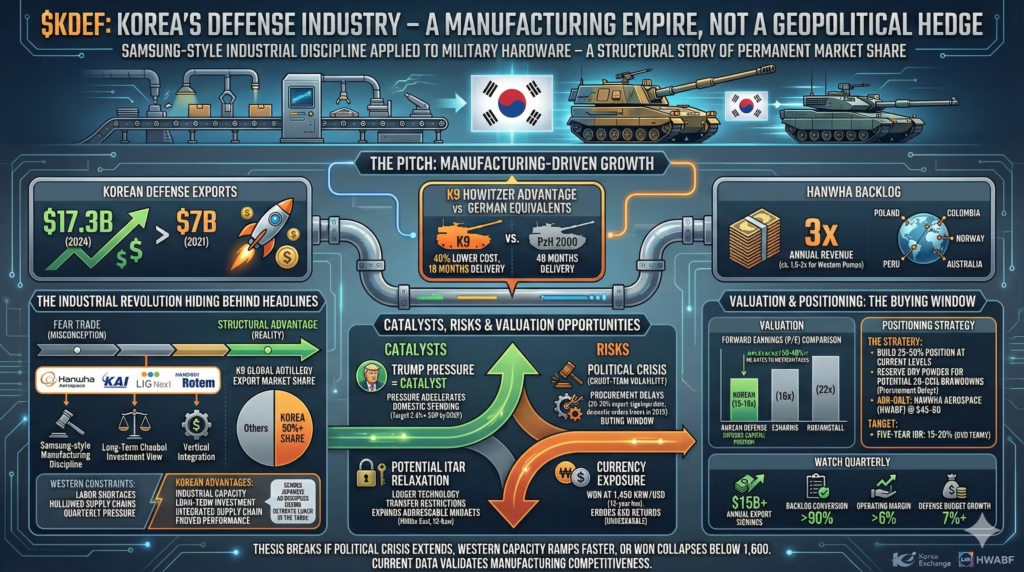

The pitch

Korean defense exports hit $17.3B in 2024, up from $7B just three years ago. Not driven by fear. Driven by manufacturing superiority—K9 howitzers cost 40% less than German equivalents and deliver in 18 months instead of 48. The market prices KDEF as a geopolitical volatility play when it’s actually a structural story: Korean chaebols applying Samsung-style industrial discipline to defense manufacturing, capturing permanent market share from capacity-constrained Western primes.

What consensus misses is that Trump’s alliance pressure, widely seen as negative, historically accelerates Korean defense spending and could loosen US technology restrictions as part of burden-sharing deals.

The friction

South Korea’s December 2024 political crisis—martial law, presidential impeachment, constitutional paralysis—has created procurement gridlock that could freeze domestic orders and delay export contract signings through much of 2025. The won has collapsed to 1,450 KRW/USD, meaning US investors face significant currency headwinds even if Korean stocks rise in local terms.

Hanwha Aerospace has already re-rated 3-4x from 2022 lows, so timing matters: buying into political chaos could mean 25-30% drawdowns before the structural thesis plays out.

Here’s what really drives this opportunity.

The manufacturing revolution hiding behind geopolitical headlines

Consensus treats Korean defense as a fear trade—buy when North Korea tests missiles, sell when diplomacy emerges. This framing completely misses the industrial transformation underway.

Hanwha, Korea Aerospace Industries (KAI), LIG Nex1, and Hyundai Rotem have applied the same manufacturing discipline that made Samsung and Hyundai global leaders to defense production. The K9 self-propelled howitzer now commands over 50% of the global artillery export market. Not because of North Korean threats, but because Korean production delivers comparable performance at dramatically lower cost and lead times.

The numbers reveal structural advantage, not temporary arbitrage. Korean defense gross margins have expanded as production scales—Hanwha Aerospace operating margins improved from 4.2% in 2021 to approximately 7.5% in 2024, with defense segment margins even higher. Order backlogs provide multi-year revenue visibility: Hanwha’s defense backlog exceeds 3x annual revenue, compared to 1.5-2x for typical Western primes. Poland’s $12B+ Korean defense contracts (K2 tanks, K9 howitzers, FA-50 jets) weren’t desperation purchases—Poland evaluated all options and chose Korea on merit.

The bear case argues Western capacity expansion will erase Korean advantages by 2026-2027. Rheinmetall and BAE are ramping production aggressively. But this view ignores structural constraints.

Germany and the UK face severe skilled manufacturing labor shortages with no near-term fix. Korean industrial workforce depth remains intact. Western defense supply chains were hollowed out by three decades of consolidation and just-in-time optimization—Rheinmetall’s expansion is bottlenecked by sub-tier suppliers who themselves lack capacity. Korean chaebols can take longer investment views with controlling family shareholders, while Western primes face quarterly earnings pressure. This dynamic reminds me of how Japanese automakers ate Detroit’s lunch in the 1980s—though the parallels aren’t perfect.

The evidence favors sustained Korean advantage. Track contract wins in low-threat markets like Colombia, Peru, and Norway—if Korea keeps winning where fear isn’t driving decisions, manufacturing competitiveness is validated. Current data shows exactly this pattern.

Why Trump pressure is a catalyst, not a headwind

The market interprets Trump’s December 2025 burden-sharing demands and troop cost renegotiations as creating uncertainty that damages Korean defense investment. Historical evidence suggests the opposite.

During Trump’s first term, pressure on South Korea to pay more for US military presence accelerated domestic defense spending and strengthened political support for indigenous weapons development. Korea’s defense budget grew at 7%+ annually through 2018-2020, outpacing prior trends.

The mechanism is straightforward: when American commitment appears conditional, Korean political consensus shifts toward self-reliance. Korea’s National Assembly has strong bipartisan support for defense spending increases when framed as reducing dependence on an unreliable ally. Current defense spending sits at approximately 2.8% of GDP; political pressure from both Trump’s rhetoric and North Korean threats is pushing toward 3.5%+ by 2027. That’s roughly $15B in additional annual spending over five years—material demand for domestic contractors.

The hidden upside: Trump’s transactional approach could actually relax technology transfer restrictions. A “deal” where Korea pays more for troop presence in exchange for looser ITAR controls would be transformative for Korean defense exports. Currently, Korean systems using US components face export constraints. Fewer restrictions would expand addressable markets significantly, particularly in the Middle East and Southeast Asia.

Watch the Korean defense budget announcement for 2026 (expected Q1 2025 despite political turmoil). If the budget shows 8%+ year-over-year growth despite domestic political crisis, the “Trump as catalyst” thesis is confirmed.

The political crisis creates a buying window, not a thesis break

South Korea’s December 2024 constitutional crisis—martial law declaration, presidential impeachment, parliamentary gridlock—is being treated as background noise by most analysts. This underestimates near-term impact while overestimating long-term damage.

Major defense procurement requires political leadership for strategic decisions. The country currently has none. Acting leadership cannot make binding international commitments. The National Assembly is paralyzed. International counterparties are uncertain whether contracts signed today will be honored tomorrow.

The practical implication: 2025 could see a procurement pause where domestic orders freeze and export contract signings slow 20-30% as buyers wait for political clarity. Constitutional court proceedings typically take 6+ months, followed by elections and new government formation. If political normalization extends into late 2025, Hanwha Aerospace 2025 revenue could miss consensus estimates by 15-20%. At current multiples, that translates to potential 25-30% stock price drawdowns.

The thing is, this is a timing issue, not a structural break. Korean defense fundamentals—manufacturing competitiveness, export order pipeline, backlog conversion—remain intact. Defense spending has bipartisan support regardless of which party ultimately governs. The crisis creates volatility and potential entry points for patient investors, but doesn’t alter the 5-year thesis. The key is avoiding full position sizing until political trajectory clarifies.

ETF mechanics and accessibility realities

The KDEF PLUS Korea Defense Industry Index ETF trades on the Korea Exchange (KRX), creating practical challenges for US and Canadian investors. Direct access typically requires a brokerage offering Korean market trading with associated foreign market fees, currency conversion costs, and potential tax complexity. ETF liquidity may be limited given niche thematic focus—verify average daily volume before sizing positions.

The ETF’s composition likely weights heavily toward the major Korean defense contractors: Hanwha Aerospace (defense systems, space, aircraft engines), Korea Aerospace Industries (FA-50 fighters, helicopters, satellites), LIG Nex1 (missiles, precision munitions, naval systems), Hyundai Rotem (tanks, armored vehicles, rail), and Hanwha Ocean (naval vessels, submarines). Hanwha Aerospace alone probably represents 25-35% of the index given its market cap dominance.

Alternative exposure for investors lacking Korean market access: Hanwha Aerospace trades as an ADR (HWABF) with reasonable liquidity. Individual Korean defense stocks can be purchased through international brokerages. Global defense ETFs like ITA or PPA have minimal Korean exposure but capture broader rearmament themes.

For investors specifically wanting Korean defense exposure, the ADR route may offer better liquidity and simpler tax treatment than the Korean-listed ETF. Though with concentration risk in a single company.

Currency exposure remains significant regardless of vehicle. The won at 1,450 KRW/USD sits near 15-year lows. Further depreciation would erode USD-denominated returns even if Korean stocks appreciate in local currency. Conversely, won stabilization or recovery would add a currency tailwind. This is unhedgeable for most retail investors—accept it as part of the risk profile.

Valuation anchoring on artificial lows creates opportunity

The “already expensive after 3-4x run” narrative anchors on 2022 lows that were themselves anomalous. Hanwha Aerospace traded at 6x earnings in late 2022 despite dominant global market positions and accelerating export growth—a generational mispricing driven by Korean market-wide dislocation rather than company fundamentals. The subsequent re-rating corrected an anomaly.

Current valuations around 15-18x forward earnings sit below comparable Western defense peers: Rheinmetall trades at approximately 22x, L3Harris at 18x, despite Korean companies showing superior growth profiles.

Backlog-to-valuation metrics reveal the gap more clearly. Korean defense companies trade at meaningful discounts to Western peers on EV/backlog ratios despite comparable or better backlog quality (firm contracts with creditworthy sovereigns). If Korean companies traded at Western peer multiples on backlog metrics—and there’s no fundamental reason they shouldn’t—the implied upside would be 30-40% from current levels.

The bear case on valuation emphasizes execution risk. Backlogs mean nothing if they don’t convert to revenue at profitable margins. Fair point. But Korean defense execution track record over 2022-2024 has been strong: contracts delivered on time, margins expanded with scale, customer relationships deepened (Poland ordering additional systems beyond initial contracts). Sell-side models typically apply heavy discounting to backlog conversion; if Korean companies continue executing, earnings revisions will follow.

The bottom line

KDEF offers exposure to a genuine structural growth story—Korean defense manufacturers achieving Samsung-style global competitiveness—wrapped in geopolitical noise that creates volatility and entry points. The 5-year thesis is compelling: Korean defense exports could reach $25-30B annually by 2028, domestic spending is accelerating toward 3.5% of GDP, and manufacturing advantages over Western competitors appear durable rather than temporary. Current valuations at 15-18x forward earnings for top holdings remain below Western peers despite superior growth.

The December 2024 political crisis creates meaningful near-term risk that the market hasn’t fully discounted though. Avoid full position sizing until political trajectory clarifies—likely mid-2025 at earliest.

For investors with Korean market access, start building a 25-50% position at current levels, with dry powder reserved for potential 20-25% drawdowns if 2025 earnings disappoint on procurement delays. For those limited to ADRs, Hanwha Aerospace (HWABF) around current levels (approximately $45-50) offers the cleanest exposure to the thesis, though with single-stock concentration risk.

Target 5-year IRR of 15-20% in USD terms, assuming won stability—currency adds both upside optionality and downside risk. Key metrics to monitor quarterly: Korean defense export contract signings (target: $15B+ annually to maintain momentum), Hanwha Aerospace backlog conversion rate (should exceed 90% of scheduled deliveries), operating margin trajectory (watch for compression below 6% as warning sign), and Korean defense budget growth (needs 7%+ annually to support domestic demand thesis).

Thesis breaks if: political crisis extends beyond 2025 and procurement freezes persist, Western capacity expansion proves faster than expected (Rheinmetall delivering on-time by late 2026), or won collapses below 1,600 KRW/USD. Any of those… well, that changes the math considerably.