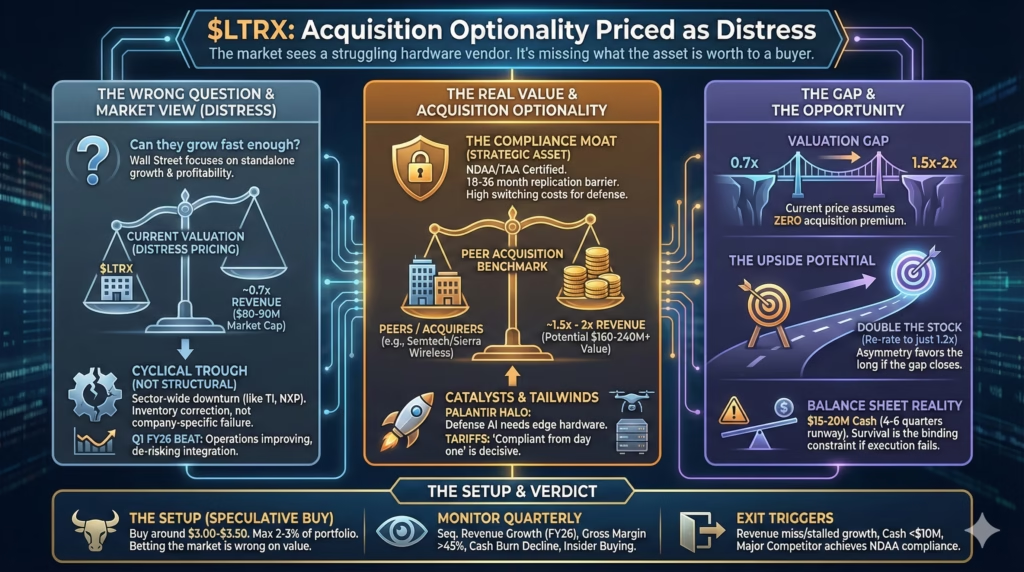

$LTRX: The micro-cap everyone’s analyzing wrong

Lantronix isn’t a growth story or a turnaround—it’s acquisition optionality priced as distress

What Lantronix actually does

Lantronix manufactures edge computing hardware—the physical devices that connect industrial equipment, IoT sensors, and defense systems to networks and enable them to process data locally rather than sending everything to the cloud. Think of them as the specialized networking boxes that let a factory machine talk to a control system, or allow a military drone to run AI algorithms in the field without an internet connection.

Their product portfolio includes IoT gateways (devices that aggregate sensor data), console managers (hardware that lets IT teams remotely access servers and network equipment), and edge AI devices (small computers that run machine learning models at the point of data collection). The critical detail: their products are certified for U.S. defense procurement through NDAA/TAA compliance, meaning the supply chain meets strict government requirements for country-of-origin and security standards.

Revenue runs around $120M annually across three segments: embedded IoT modules that get built into other companies’ products, infrastructure management hardware for data centers and industrial facilities, and edge AI gateways for defense and smart city deployments. They’re not a household name because they sell to OEMs and system integrators rather than end users—you’ve probably used systems with Lantronix components inside without knowing it.

The pitch

Lantronix trades at 0.7x revenue while comparable defense-adjacent hardware acquisitions have closed at 2x or higher—Semtech paid $1.2B for Sierra Wireless at roughly that multiple. The company’s NDAA/TAA compliance certifications represent an 18-36 month head start that competitors cannot replicate quickly, creating structural protection in a market where the current administration has made defense AI spending a national priority.

The market sees a subscale hardware vendor struggling toward profitability. It’s missing that the compliance moat and design win relationships are worth more to a strategic acquirer than to public market investors pricing organic growth alone.

The friction

Quarterly revenue sits at roughly $28-30M with persistent GAAP losses, and the path to standalone profitability likely requires scaling to $150M+ annually—a hurdle this company has never cleared. Customer concentration risk is real but underexplored: if one or two OEM relationships representing 30-50% of revenue shift, the thesis breaks overnight. Micro-cap liquidity means any risk-off episode or delayed design win can crater the stock 30-40% before institutional capital even notices.

Here’s what actually drives this opportunity.

The acquisition math Wall Street ignores

The dominant debate—can Lantronix grow revenue fast enough to reach profitability?—is the wrong question.

M&A activity in defense-adjacent edge hardware tells a different story. When Semtech acquired Sierra Wireless in 2023, it paid approximately $1.2B for a company with $600M in revenue, representing a 2x revenue multiple. Digi International trades at roughly 1.5x revenue despite similar profitability challenges. Lantronix, at an $80-90M market cap on $120M trailing revenue, trades at 0.7x—less than half the peer acquisition benchmark.

The strategic rationale for consolidation is strengthening. Defense primes like L3Harris need certified edge solutions without the 24-month compliance timeline. Industrial automation giants want IoT connectivity without building from scratch. Post-COVID supply chain redesigns have made “buy vs. build” calculations favor acquisition for certified platforms. The Q1 FY2026 beat—$0.04 EPS versus -$0.02 estimated—doesn’t matter because Lantronix is suddenly profitable. It matters because improving operations de-risk integration for acquirers evaluating the asset.

The bear counterargument is valid: no acquisition is guaranteed, and betting on M&A is speculative. But the counter-counter is that current valuation already prices zero acquisition premium. If LTRX simply re-rates to 1.2x revenue (still below peer multiples), the stock doubles. The asymmetry favors the long position.

Watch for 13D filings showing strategic accumulation, management commentary on “exploring alternatives,” or board composition changes signaling sale preparation.

Why the compliance moat is deeper than a checkbox

Bulls mention NDAA/TAA compliance as a positive attribute. They understate how much it matters.

Obtaining these certifications isn’t paperwork—it requires complete supply chain documentation, country-of-origin verification for every component, and often physical manufacturing restructuring. For a Chinese competitor or a company currently manufacturing in Shenzhen, this process takes 18-36 months after deciding to pursue it. Most never bother because the addressable market looks small relative to commercial volumes.

Lantronix is already designed into drone platforms and defense programs. Once embedded in a program of record, switching costs become bureaucratic rather than technical. Re-qualification requires new security reviews, testing cycles, and program office approvals that can delay deployments by years. The U.S. government doesn’t switch edge hardware vendors to save 15% on unit costs.

The tariff environment amplifies this protection. Trump’s 2025 tariff escalation—25%+ on Chinese electronics—hurts importers while Lantronix’s supply chain is already structured for compliance. Competitors scrambling to reshore face cost increases that Lantronix has already absorbed. For risk-averse procurement officers, “tariff-compliant from day one” becomes a decisive factor.

Bears correctly note that larger players could eventually replicate this position. But “eventually” is 2-3 years minimum, during which Lantronix accumulates design wins that create their own switching costs. The moat isn’t permanent, but it doesn’t need to be—it needs to last until acquisition or until enough design wins convert to create revenue escape velocity.

The cyclical timing everyone’s missing

FY2025 showed revenue decline and GAAP losses. This looks like company-specific deterioration until you check what happened across the sector.

Texas Instruments revenue fell 13% in 2024. NXP Semiconductors declined 5%. Microchip Technology dropped 10%. The entire edge computing and IoT hardware industry experienced an inventory correction as customers digested COVID-era over-ordering. Evaluating Lantronix on trough-cycle fundamentals is like judging a retailer’s Q1 results—you’re measuring the seasonal low and extrapolating failure.

The thing is, the Q1 FY2026 beat suggests the cycle is turning. More importantly, Lantronix maintained R&D investment and launched new products (5G-ready AI gateways, SmartEdge.ai devices) through the downturn. They didn’t slash their way to a beat—they invested through the trough and are positioned for the upturn. If edge AI and defense IoT spending are real secular trends (and capex data confirms they are), current operational metrics matter less than portfolio positioning for the recovery.

The risk is that the cycle doesn’t turn, or that Lantronix loses share during the upturn to better-capitalized competitors. Q2 and Q3 FY2026 results will be decisive.

The Palantir halo and defense AI legitimization

Palantir’s 300%+ run in 2024-2025 changed how markets value defense-adjacent AI companies. PLTR proved government AI isn’t a niche—it’s a premium category. But Palantir is software. Their Artificial Intelligence Platform needs hardware for deployment in disconnected, tactical environments where cloud round-trips aren’t possible. Drones, forward operating bases, industrial facilities—these require edge compute that can run inference locally.

This reminds me of how the picks-and-shovels plays during the cloud buildout got ignored until AWS started naming suppliers. Different dynamic, but similar pattern of capital flow eventually finding the unglamorous hardware layer.

Lantronix doesn’t need to be Palantir. It needs to benefit from the spending wave Palantir has catalyzed. Defense primes and CFOs who were skeptical about “edge AI” budgets now see Palantir’s results and approve hardware procurement. The SmartEdge.ai positioning directly addresses this opportunity. A re-rating from 0.7x revenue to 1.5x revenue—still far below software multiples, but reflecting “defense AI hardware” premium—implies 100%+ upside without any fundamental improvement.

The bear case is that Lantronix hasn’t explicitly captured this association through partnerships or customer announcements. They’re underexploiting the narrative connection. If CES 2026 product launches don’t generate meaningful customer traction in the defense AI segment, the Palantir halo remains theoretical rather than fundamental.

Balance sheet reality check

Micro-cap bulls often ignore survival math. Lantronix’s most recent quarter showed cash burn improving but not eliminated. Total cash position sits around $15-20M with minimal debt, providing roughly 4-6 quarters of runway at current burn rates. This isn’t distressed—the company won’t need emergency dilution next quarter—but it’s not comfortable either.

A 20% revenue miss for two consecutive quarters would pressure the balance sheet enough to force unfavorable financing or accelerate sale discussions from a weak negotiating position.

The good news is that improving operational performance extends runway without dilution. The Q1 beat wasn’t a one-time accounting trick—it reflected genuine cost discipline and favorable mix. If Q2 confirms the trend, balance sheet concerns recede. If Q2 disappoints… well, this becomes the binding constraint that overrides all the strategic optionality arguments.

Insider behavior provides a signal worth monitoring. If management and board members are buying shares personally, they’re signaling confidence that runway extends long enough for the thesis to play out. Net insider selling would be a red flag suggesting internal skepticism about near-term execution.

The bottom line

Buy LTRX at current levels around $3.00-3.50 as a speculative position sized appropriately for micro-cap risk—no more than 2-3% of a diversified portfolio. The stock trades at 0.7x revenue when peer acquisitions close at 2x, creating 100%+ upside if strategic M&A interest emerges or if the company simply re-rates toward sector averages. Current valuation prices zero acquisition premium and assumes structural rather than cyclical weakness—both assumptions look wrong given the compliance moat, design win positioning, and sector consolidation dynamics.

Key metrics to monitor quarterly: revenue trajectory (needs to show sequential growth through FY2026), gross margin stability (must stay above 45% to support operating leverage), and cash burn trajectory (must decline toward breakeven by Q4 FY2026). Watch for 13D filings, insider buying, defense contract announcements naming Lantronix specifically, or management language shifts toward “strategic alternatives.”

Thesis breaks if: Q2 FY2026 revenue misses and sequential growth stalls, customer concentration disclosure reveals 40%+ dependence on a single OEM, cash position falls below $10M without clear path to profitability, or a major competitor achieves NDAA compliance and begins winning Lantronix’s design pipeline. Any of these triggers warrants immediate exit regardless of price.

Look, this isn’t a safe play. It’s a calculated bet that the market is valuing Lantronix as a struggling standalone when it should be valued as acquisition inventory with a compliance moat. That gap either closes—or it doesn’t. Position accordingly.