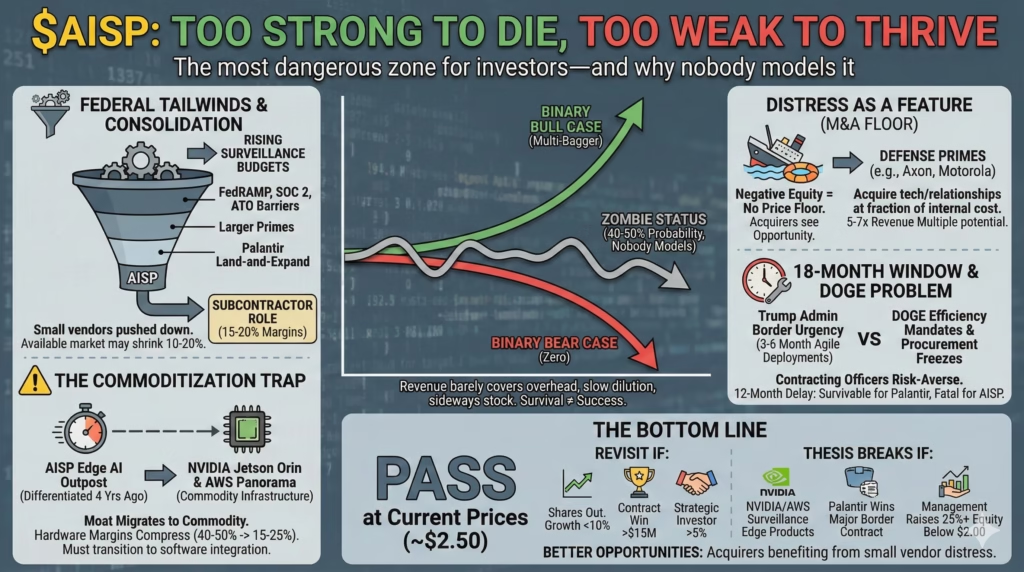

$AISP: the surveillance AI stock that probably survives but disappoints

Airship AI sits in the most dangerous zone for investors—too strong to die, too weak to thrive

The pitch

Airship AI holds $11 million in backlog with a larger validated pipeline while trading at just 5x revenue—already within typical acquisition range for distressed defense tech assets. The Trump administration’s border security push creates an 18-month procurement window where small, agile vendors can deploy surveillance tech faster than slow-moving defense primes.

Here’s what the market misses: AISP’s financial fragility makes them more attractive as an acquisition target, not less. That creates a potential floor on equity value even if standalone execution falters.

The friction

Negative equity and cash burn create dilution risk that could erode shareholder value by 20%+ annually before any thesis plays out. Edge AI processing—supposedly AISP’s core differentiator through Outpost AI—faces rapid commoditization as NVIDIA’s Jetson platform and AWS Panorama democratize the capability within 24 months. Federal procurement freezes under DOGE could delay 30-40% of 2025 pipeline conversions regardless of technical merit.

Let’s examine what really drives this.

The “muddle through” outcome nobody models

Wall Street frames AISP as a binary bet: contracts convert and it’s a multi-bagger, or cash runs out and it zeros. The contrarian reality is messier.

Government contractors rarely die quickly. They enter zombie status where revenue barely covers overhead, equity holders experience slow dilution death, and the stock trades sideways for years. This middle outcome carries perhaps 40-50% probability—yet no analyst models it because it lacks narrative appeal.

The evidence is hiding in plain sight. AISP’s revenue declined year-over-year in recent quarters despite supposedly favorable AI tailwinds. Not collapsing. Not breaking out either. Management can likely raise small equity tranches, win occasional contracts, and cut costs enough to survive indefinitely. Survival isn’t the same as success.

Track shares outstanding over the next four quarters. If share count increases more than 20% annually while revenue grows less than 30%, the muddle-through scenario is playing out. You’re not buying cheap optionality—you’re buying an option with severe theta decay as dilution erodes your stake. The expected value calculation changes dramatically when you include “survives but disappoints for a decade” alongside the binary outcomes.

Federal tailwinds don’t flow downhill equally

The bull case assumes rising federal AI and surveillance budgets will lift AISP alongside established primes. The procurement reality runs opposite.

Federal acquisition is actively consolidating toward fewer, larger platforms. FedRAMP authorization, SOC 2 compliance, and existing Authority to Operate requirements create barriers that are increasing, not decreasing. Small vendors get pushed into subcontractor roles capturing 15-20% margins on pass-through work rather than 70%+ software margins as primes.

Examine AISP’s contract announcements carefully. Look for the word “subcontract” or partnership language indicating they’re working under a prime. If more than half of new contract value comes as a subcontractor, the business model differs fundamentally from what investor presentations suggest. The margin structure of a subcontractor resembles a staffing firm more than a software company.

Palantir compounds this problem through aggressive state and local government expansion. Their land-and-expand playbook involves deploying at low or no cost initially, resetting customer expectations for pricing. Agencies that might have paid AISP fair value now expect Palantir-style pilot programs that AISP cannot fund. The thing is, the relevant question isn’t whether the surveillance market grows—it’s whether the market available to AISP grows. That market may be shrinking 10-20% annually even as overall spending rises.

Why financial distress might be a feature, not a bug

For potential acquirers, AISP’s negative equity represents opportunity. A well-capitalized defense prime like L3Harris or General Dynamics IT could acquire AISP’s technology stack and customer relationships at a fraction of internal development cost precisely because AISP lacks negotiating leverage. Negative book value means no floor on price. Management’s awareness of this dynamic might make them receptive to acquisition discussions.

This reminds me of what happened to a dozen small defense tech firms in 2018-2019—acquired quietly at 5-7x revenue while retail investors waited for breakthroughs that never came. Different companies, same playbook.

Defense primes face pressure to demonstrate AI capabilities for next-generation contracts, but their organic AI development moves slowly. The 2025-2026 window creates unusual M&A conditions where acquiring surveillance AI capabilities lets primes demonstrate technological currency. Strategic acquisitions in adjacent spaces have occurred at 4-8x revenue. AISP already trades at 5x, meaning limited downside if acquisition interest materializes. A 50% premium on a strategic deal would deliver 50%+ returns—not a moonshot, but meaningful if acquisition probability exceeds 20%.

Watch for strategic partnership announcements with defense primes who might be testing before buying. Track whether PE-backed defense consolidators add surveillance software to stated acquisition criteria. Monitor 13D filings for strategic investor accumulation above 5%. The paradox: worse stock performance makes AISP more attractive as an acquisition target, creating a perverse floor on equity value.

The 18-month border security window

Trump administration border priorities create a specific procurement opportunity favoring agile small vendors. DHS and CBP face intense political pressure to deploy surveillance capabilities faster than normal acquisition cycles allow. Large primes require 18-36 month integration timelines. Small vendors can demonstrate capability in 3-6 months.

This temporary window makes AISP’s size an advantage—they can staff a major deployment with their whole company while Lockheed creates a new program office. A $20-50 million border surveillance contract in 2025-2026 would transform AISP’s trajectory even as one-time revenue rather than recurring.

The question is whether management recognizes this window and pivots sales motion accordingly, or continues chasing smaller, more competitive opportunities. Competitors like Anduril and Skydio have better Thiel-Trump network connections. Real execution risk even if the opportunity exists.

The DOGE paradox cuts against this timing. Government efficiency mandates create procurement freezes across agencies. Contracting officers become risk-averse, delaying awards pending guidance on which programs survive. A 12-month delay in a $30 million contract is survivable for Palantir but potentially fatal for AISP. Career procurement officials grow reluctant to award contracts to companies that might subsequently fail—biasing decisions toward established vendors. AISP’s 2025 pipeline could experience 30-40% conversion delays regardless of technical merit.

The commoditization trap closing on Outpost AI

AISP’s edge processing capability through Outpost AI was genuinely differentiated three to four years ago. Today? NVIDIA’s Jetson Orin platform provides turnkey edge inference any competent systems integrator can deploy. AWS Panorama offers cloud-connected edge analytics as a service. The moat is migrating from proprietary technology to commodity infrastructure.

AISP’s value proposition shifts from “we do edge AI” to “we integrate edge AI specifically for surveillance”—a much narrower and more competitive positioning. Hardware margins on edge devices are compressing from 40-50% to 15-25% as white-box alternatives proliferate. If AISP’s current revenue model includes significant hardware resale, margin structure could compress substantially even if revenue grows.

NVIDIA has explicitly stated edge AI democratization as a strategic priority. AWS Panorama launched specifically to commoditize this capability. The technical differentiation moat erodes faster than AISP can build a customer relationship moat.

Within 24 months, edge AI processing will not constitute competitive advantage. AISP must derive value from software and integration alone—requiring a business model transition they haven’t yet demonstrated capability to execute.

The bottom line

Pass at current prices around $2.50 per share.

The risk-reward skews negative when properly weighting the 40-50% probability of “muddle through” dilution alongside binary outcomes. AISP trades at 5x revenue, which sounds cheap until you recognize revenue declined year-over-year, edge AI differentiation faces commoditization within 24 months, and shares outstanding likely increase 20%+ annually through survival financing. The acquisition floor provides some downside protection—strategic buyers have paid 4-8x revenue for similar assets—but hoping for a takeout isn’t an investment thesis.

Revisit if three conditions emerge: shares outstanding growth slows below 10% annually indicating reduced dilution pressure, a contract win exceeding $15 million demonstrates ability to capture the border security window, or a strategic investor takes a 5%+ position signaling acquisition interest. Monitor quarterly revenue trajectory—two consecutive quarters of 20%+ year-over-year growth would indicate the thesis is inflecting.

Thesis breaks decisively if edge AI commoditization accelerates through NVIDIA or AWS announcements targeting surveillance specifically, if Palantir wins a major border security contract that would have been AISP’s opportunity, or if management announces an equity raise exceeding 25% of shares outstanding at prices below $2.00.

Look, the speculative upside exists but requires too many variables to align while capital erodes through dilution. Better opportunities exist in surveillance AI through acquirers like Axon or Motorola Solutions who benefit from small vendor distress rather than suffering from it.