$HOOD is betting everything on one thing: that young people stay young at heart

The market sees a diversified fintech; the reality is a leveraged bet on retail speculation with a hidden $84 trillion option attached

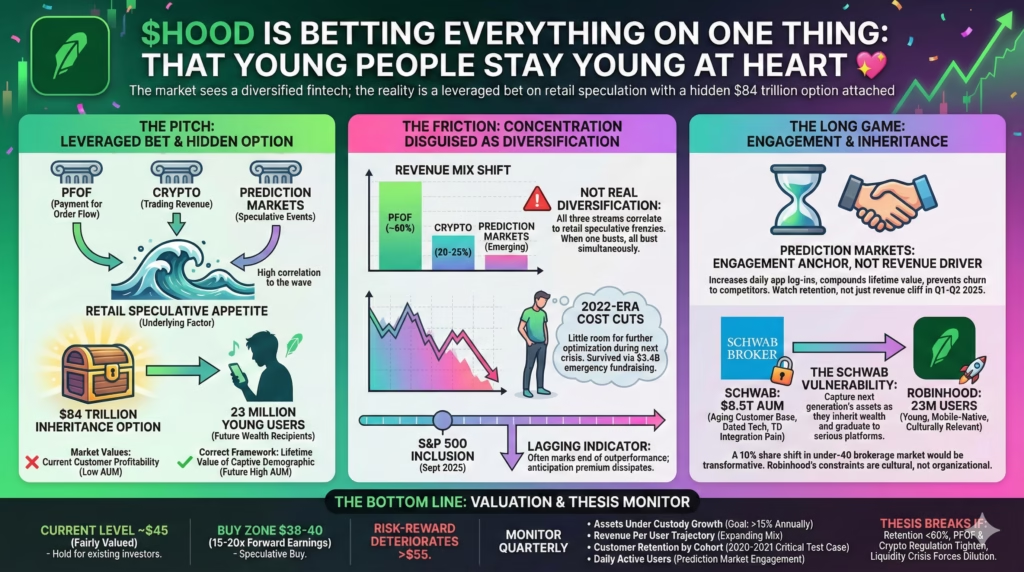

The pitch

Robinhood’s 220% rally prices in a turnaround that already happened. But it dramatically underprices the optionality on 23 million users who will inherit $84 trillion over the next two decades. Here’s the thing—the “diversification” into crypto and prediction markets isn’t actually diversification. It’s tripling down on retail speculation. That’s a feature, not a bug, if you believe speculative engagement compounds into lifetime customer value. The market values Robinhood on current customer profitability when the correct framework is lifetime value of a captive demographic that opened their first brokerage account on a pink confetti app.

The friction

Every revenue stream—PFOF, crypto, prediction markets—correlates to the same underlying factor: retail speculative appetite. When the next risk-off event hits, all three decline simultaneously, and Robinhood’s 2022-era cost cuts leave little room for further optimization. The company survived one liquidity crisis through $3.4 billion in emergency fundraising during peak euphoria. The next crisis arrives when investors are far less generous.

Time to dig into the details.

The diversification story is actually a concentration story

Wall Street celebrates Robinhood’s revenue mix shift from 81% PFOF dependence to roughly 60%, with crypto contributing 20-25% and prediction markets emerging as the “fastest-growing product ever.” This reads like textbook diversification.

It isn’t.

PFOF revenue spikes during retail trading frenzies. Crypto revenue spikes during retail speculation frenzies. Prediction market revenue spikes during high-engagement speculation events like elections. All three revenue streams are different expressions of the same underlying factor: retail speculative appetite dressed in different costumes.

The bull case acknowledges this correlation but argues it doesn’t matter because secular trends favor speculation. Smartphone penetration continues rising globally. Crypto is institutionalizing through ETF approvals. The generational wealth transfer brings trillions to Robinhood’s core demographic. These structural tailwinds mean the “speculation index” trends higher over time, even if it’s volatile quarter to quarter. Operating leverage magnifies this: incremental margins on trading revenue run 60-70%, meaning each speculative wave generates outsized profits on the now-lean cost base.

The bear case is straightforward: Robinhood trades at roughly 10x revenue with a portfolio of bets on the same underlying asset. A 2022-style environment where retail engagement collapses would hit all revenue streams simultaneously. The market assigns a “diversified fintech” multiple to what remains a levered bet on retail trading volumes. If prediction market revenue cliffs 50%+ post-inauguration (as political engagement normalizes) while crypto enters another winter, the revenue trajectory could disappoint badly.

The evidence suggests correlation is real but manageable. Robinhood survived 2022—barely—with the stock falling 82% from its highs. The company emerged leaner and proved it could reach GAAP profitability at normalized volumes. The question isn’t whether correlation exists; it’s whether the upside from correlated booms exceeds the downside from correlated busts. For a long-term holder, the asymmetry probably favors the bulls if the cost base stays disciplined.

S&P 500 inclusion marks an ending, not a beginning

Index inclusion in September 2025 after a 220% YTD run feels like validation. It’s actually a lagging indicator—one that historically marks the end of outperformance, not the beginning. The S&P 500 committee adds companies after they’ve demonstrated profitability and grown large enough to qualify. By definition, they’re adding after the easy money has been made. The passive flows argument is overstated: index funds already accumulated during the run-up as inclusion became anticipated, and the incremental buying from actual addition is a one-time event rather than ongoing support.

Bulls argue institutional credibility matters beyond mechanical flows. Robinhood can now appear in more institutional portfolios, attract corporate partnerships, and recruit talent with “S&P 500 company” status. The reputational rehabilitation from “meme stock casino” to “legitimate financial institution” opens doors previously closed. Management’s stated 10-year vision to become the “world’s leading financial ecosystem” gains credibility when you’re sitting alongside JPMorgan and Goldman in the index.

The bear case is simpler: companies added to the S&P 500 near multi-year highs frequently underperform the index over subsequent 12-24 months as the “anticipation premium” dissipates. Investors using index inclusion as a buy signal are essentially buying the news after smart money bought the rumor. The institutional investors who wanted HOOD exposure already have it. The ones who don’t aren’t waiting for index inclusion to change their minds.

Watch Q4 2025 and Q1 2026 13F filings closely. If institutional ownership doesn’t materially increase post-inclusion, the “credibility unlock” thesis weakens considerably.

Prediction markets are an engagement anchor, not a revenue driver

Management’s “fastest-growing product ever” language around prediction markets invites investors to model significant revenue contribution. This is probably wrong in the near term and possibly right in the long term—for reasons management hasn’t articulated clearly.

Prediction markets face a regulatory patchwork that severely caps realistic TAM. The CFTC has jurisdiction over event contracts, state gambling laws apply unevenly, and Kalshi’s ongoing legal battles demonstrate this space remains legally unsettled. More importantly, Robinhood launched prediction markets during a presidential election year—the single highest-engagement period possible. Q1-Q2 2025 revenue will cliff as political speculation normalizes, and the TAM for sports events is encumbered by licensed sports betting operators.

The bullish reframe: prediction markets might never contribute meaningful revenue, but they could be an extraordinary engagement anchor. Every new product—crypto, predictions, retirement accounts, credit cards—increases the probability that users log into Robinhood daily. High engagement compounds into higher lifetime value through cross-sell and reduced churn. A user checking prediction markets daily is a user not migrating to Schwab as they age into wealth accumulation. The correct framework prices prediction markets as an engagement multiplier on customer lifetime value, not a P&L line item.

The risk is regulatory: if the CFTC or state attorneys general crack down on event contracts, Robinhood loses both the modest revenue and the engagement benefit simultaneously. This isn’t a trivial risk given the political sensitivity of election betting. This reminds me of DraftKings’ regulatory whiplash circa 2015-2016—though that turned out fine eventually. Monitor Q1-Q2 2025 prediction market revenue closely. If it falls 60%+ from Q4 2024, the “engagement anchor” thesis needs validation through user retention data rather than revenue.

The $84 trillion inheritance option nobody’s pricing

Here’s what the market misses entirely: Robinhood isn’t competing for trading volume. They’re competing to be the default destination for inherited assets.

Over the next 20 years, Baby Boomers will transfer an estimated $84 trillion to younger generations. Gen Z and younger Millennials—Robinhood’s 23 million users—will be primary recipients. When a 28-year-old inherits $500,000 from a deceased parent’s Schwab account, where do they move it? The answer depends heavily on existing relationships, and Robinhood has already established that relationship.

The “first wallet” effect is powerful in financial services. Inertia is extreme. The platform where you open your first brokerage account captures disproportionate lifetime value. Robinhood’s current users are young and broke—average account size around $4,500 versus $100,000+ at Schwab. Looks terrible on current AUM metrics. But “young and broke” becomes “middle-aged and wealthy” becomes “inheriting parents’ assets” over a 20-year horizon. If Robinhood retains even 30-40% of their current user base as those users age and inherit wealth, assets under custody could 10x from current levels.

The bear case: customer retention is unproven at scale. Users burned by GameStop and the 2021-2022 drawdowns may harbor permanent resentment. As these users mature into serious wealth accumulation—retirement planning, estate planning, tax optimization—they may graduate to platforms with fuller service offerings. Robinhood’s brand, optimized for young speculators, may actively repel users as they age. The transition from “trading app for degenerates” to “serious wealth platform” requires difficult brand evolution that management hasn’t demonstrated they can execute.

This is the central tension: the inheritance option is real and potentially worth more than Robinhood’s current market cap. But capturing it requires customer retention through a 20-year journey, and the company has existed for only 12 years with meaningful scale for perhaps 5. The option is underpriced but far from certain.

The Schwab vulnerability nobody discusses

Charles Schwab manages $8.5 trillion across 35 million active accounts. The 800-pound gorilla of retail brokerage. But beneath the surface: their average customer is aging (large portion over 55), their technology stack is dated, and the TD Ameritrade integration has been painful. Schwab’s younger customers—attracted by commission-free trading post-2019—have relatively low assets and weak brand loyalty. They joined for price, not product. Which means they’re vulnerable to switching.

Robinhood doesn’t need to beat Schwab; they need to intercept the cohort Schwab should be nurturing. Every year, a cohort of Schwab’s young, low-AUM customers reaches the age where they start accumulating serious wealth. Robinhood is more familiar, more mobile-native, and more culturally relevant to this demographic.

Schwab’s size is also a liability: they can’t offer crypto, prediction markets, or edgier products without risking their core $8.5 trillion AUM base. This leaves market opportunities that Robinhood can capture while Schwab watches from the sidelines.

A 10% share shift in the under-40 brokerage market would be transformative for Robinhood’s trajectory. This isn’t about revenue today—it’s about which platform captures the next generation’s assets as they compound over decades. Schwab’s organizational constraints make it difficult to compete on product innovation. Robinhood’s constraints are cultural (can they mature without losing relevance) rather than organizational.

The bottom line

Monitor these metrics quarterly: assets under custody growth (need 15%+ annually to validate the wealth accumulation thesis), revenue per user trajectory (should be expanding as product mix shifts to higher-value services), and customer retention by cohort vintage—early users from 2020-2021 are the critical test case. The prediction market revenue cliff in Q1-Q2 2025 will test whether the “engagement anchor” thesis holds. Watch daily active users rather than revenue when that data releases.

Thesis breaks if: customer retention among 2020-2021 cohorts falls below 60%, PFOF and crypto regulation tighten simultaneously, or another liquidity crisis forces a dilutive capital raise at distressed pricing.

The stock remains a leveraged bet on retail speculation with an underpriced option attached. That option is worth something.

But not infinite patience if execution falters.