$BNTX – BioNTech’s $17 billion question

The market values the entire oncology pipeline at less than zero—either catastrophic capital destruction looms, or this is a historic mispricing

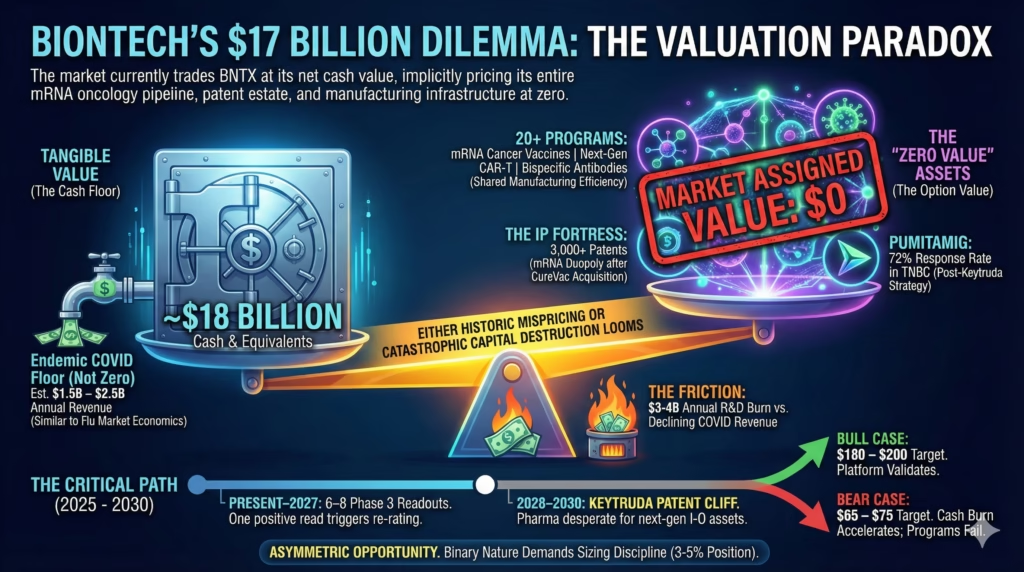

The Pitch: BioNTech trades at net cash value. That means the market assigns zero value to 20+ clinical oncology programs, 3,000 mRNA patents, and one of only two commercial-scale mRNA manufacturing platforms on Earth.

The math that doesn’t add up

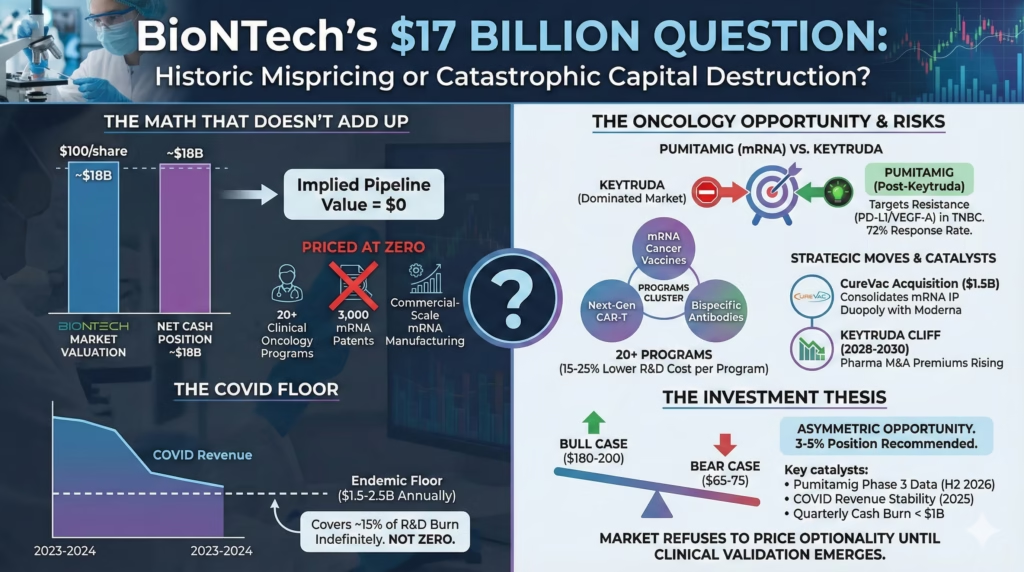

At roughly $100 per share against an $18B cash position, BioNTech’s pipeline is priced at zero. The entire oncology portfolio. The manufacturing infrastructure. The patent estate. All of it.

The CureVac acquisition just consolidated mRNA intellectual property into a duopoly with Moderna. Pumitamig’s 72% response rate in triple-negative breast cancer represents the first real evidence that mRNA transfers beyond vaccines.

One positive Phase 3 readout—and BioNTech has 6-8 shots through 2027—could trigger violent re-rating. The kind that took Moderna from $70 to $400 when its platform thesis crystallized.

The friction is real: $3-4B annual R&D burn while COVID revenue declines 40-50% yearly. No mRNA cancer therapeutic has achieved regulatory approval anywhere. The entire oncology thesis remains scientifically unvalidated.

The COVID floor everyone ignores

The market extrapolates 2023-2024’s 80% revenue collapse into perpetuity. This misunderstands endemic respiratory virus economics.

Flu vaccines generate $7-8B annually despite decades of availability and modest efficacy. COVID remains more severe in elderly and immunocompromised populations. The floor sits around $1.5-2.5B annually—not zero.

At $1.5B with 30% margins, that’s $450M in annual profit covering 15% of R&D spend indefinitely.

Bears correctly note vaccine fatigue is real. But they’re confusing declining growth with terminal decline. Different trajectories entirely.

Pumitamig isn’t fighting Keytruda

The consensus frames Pumitamig as entering a crowded, dominated market. Look closer at the trial design.

The 72% response rate included second-line patients who had already progressed—meaning patients for whom Keytruda failed. The dual PD-L1/VEGF-A targeting addresses resistance that develops after anti-PD-1 treatment.

BioNTech doesn’t need to beat Keytruda. They need to become what oncologists try when Keytruda stops working.

That patient population grows as Keytruda adoption increases. Counter-intuitive demand dynamics.

The bear case has merit: 62% confirmed versus 72% overall suggests some responses are unstable. Duration data remains immature. Oncologists are notoriously conservative—the inertia is brutal.

Twenty programs aren’t desperation

Bears characterize the sprawling pipeline as spray-and-pray capital destruction. Examine the architecture.

Programs cluster around three platforms: mRNA cancer vaccines, next-gen CAR-T, and bispecific antibodies. Each tests 3-4 indications using shared manufacturing. This mirrors how Genentech built its franchise before Avastin and Herceptin changed the narrative.

The key insight: BioNTech’s R&D spend per program runs 15-25% below industry average due to platform leverage. Marburg and Mainz manufacturing, built for COVID scale, now serves oncology trials at marginal cost.

If 2-3 programs succeed, the 4th through 6th become dramatically cheaper to commercialize.

Platform correlation cuts both ways. If mRNA cancer delivery proves fundamentally flawed, multiple programs fail simultaneously. Base rates suggest 85-90% of oncology programs fail Phase 3.

CureVac was about patents

The $1.5B acquisition looks like throwing good money after bad. The strategic logic is different.

CureVac holds foundational mRNA patents that could have been weaponized by competitors or trolls. BioNTech now controls two of the three largest mRNA patent portfolios globally. Any pharma wanting mRNA oncology capabilities must now partner with or acquire from this duopoly.

The $1.5B represented roughly 0.5x CureVac’s peak cash—not a desperate premium.

IP moats matter only if the technology works. If mRNA oncology broadly fails, BioNTech owns monopoly rights to nothing valuable.

The Keytruda cliff changes everything

Merck’s Keytruda loses patent exclusivity in 2028-2030. Major pharma companies are desperately seeking next-generation immuno-oncology assets. This timeline aligns with BioNTech’s Phase 3 readouts.

M&A premiums for de-risked oncology assets have increased 40% since 2022. Pfizer/Seagen at $43B. Merck/Prometheus at $10.8B.

Pumitamig alone, if successful in TNBC, could command $5-10B deal value. BioNTech becomes the Kite Pharma of mRNA oncology in this scenario.

Partnership premium requires clinical success. If lead programs miss endpoints by 2027, the thesis evaporates. BioNTech becomes a cash shell with unvalidated technology.

And yet. The option value exists.

The position

BioNTech represents asymmetric opportunity at $95-105. Bull case: $180-200 if the platform validates. Bear case: $65-75 if cash burn accelerates and programs fail.

This is a 3-5% position, not a core holding. The binary nature of clinical catalysts demands sizing discipline.

Watch Pumitamig Phase 3 data in H2 2026—need confirmed response rate above 55% and duration exceeding 8 months. Monitor COVID revenue for sequential quarterly growth in 2025. If quarterly cash burn exceeds $1B consistently, timeline pressure becomes real.

Thesis breaks if Pumitamig shows no improvement over Keytruda, two additional lead programs miss endpoints before 2027, cash falls below $10B, or mRNA delivery to solid tumors proves fundamentally limited.

The 53% analyst upside isn’t a value trap signal. It reflects genuine optionality the market refuses to price until clinical validation emerges.

That’s the opportunity. Whether it materializes is a different question.