Beyond Scott Galloway’s 2026 predictions: where the real value hides

When consensus catches prophecy, alpha migrates to the blind spots

Scott Galloway’s 2026 tech theses have shifted from contrarian hot takes to institutional gospel. Once a vision becomes an investment product, excess returns move elsewhere.

The opportunity now is not to contradict his direction, but to get paid where narrative and pricing quietly diverge.

Executive summary: Galloway’s framework vs. market reality

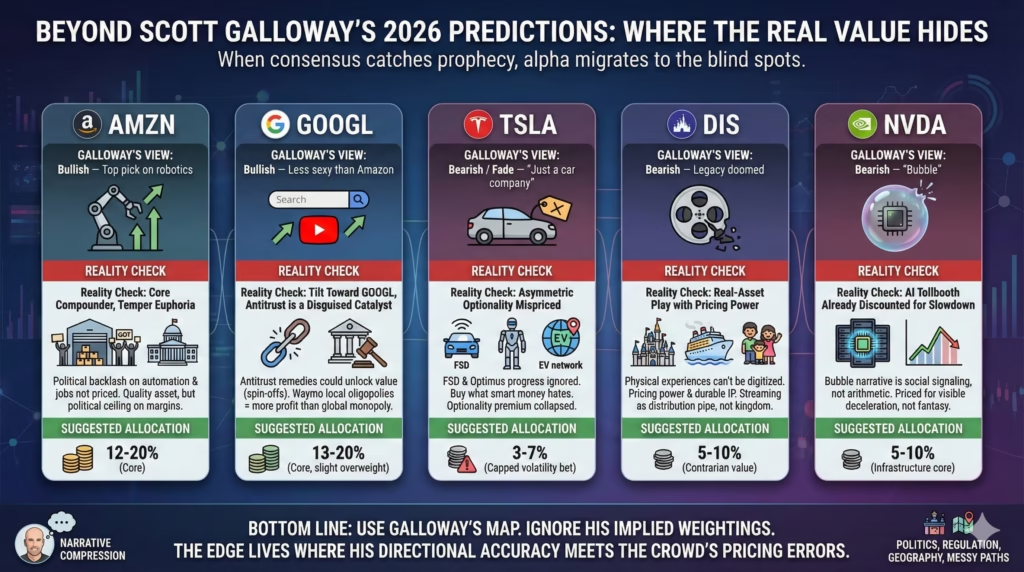

For readers in a hurry, here’s where Galloway’s predictions meet pricing reality:

AMZN Bullish — top pick on robotics Core compounder, but temper robotics euphoria. Political backlash on automation not priced. 12–20% (Core)

GOOGL Bullish — but less sexy than Amazon Tilt toward GOOGL over AMZN. Antitrust is a disguised catalyst, not just risk. 13–20% (Core, slight overweight)

TSLA Bearish / Fade — “just a car company” Asymmetric optionality mispriced. Buy what smart money hates. FSD + Optimus progress ignored. 3–7% (Capped volatility bet)

DIS Bearish — legacy doomed Real-asset play with pricing power. Physical experiences can’t be digitized. Buy what finance ignores. 5–10% (Contrarian value)

NVDA Bearish — “bubble” AI tollbooth already discounted for slowdown. Bubble narrative is social signaling, not arithmetic. 5–10% (Infrastructure core)

Bottom line: Use Galloway’s map. Ignore his implied position sizes. The edge lives where his directional accuracy meets the crowd’s pricing errors.

Why Galloway changes the game (and why it matters now)

Scott Galloway built his media empire on a rare ability: compressing complex trends into punchy theses that markets can digest. His tech calls are no longer outsider views — they now structure institutional allocations.

His 2026 framework looks like an unwritten ETF:

Amazon wins through warehouse robotics.

Alphabet dominates with Waymo and “cheap” AI.

Tesla is just an overvalued car company.

Disney is a legacy media relic doomed to extinction.

Nvidia embodies the AI bubble.

Directionally, these theses are largely correct.

Financially, most are already fully owned, preached, and priced.

Alpha has migrated to the uncomfortable nuances that Galloway himself mentions but his disciples ignore:

- Amazon’s robotics upside is real, but political backlash on destroyed jobs is too.

- Waymo’s best outcome isn’t global domination, but messy local oligopolies.

- Tesla’s optionality remains massive, while the optionality premium has quietly collapsed.

- Disney generates its real cash where AI can’t digitize: physical experience.

- Nvidia looks less like a bubble than a growth stock markets are already discounting for brutal slowdown.

The ranking that follows isn’t about who “wins” Galloway’s story.

It’s about who still pays for the risk taken, after his narrative became consensus:

- Quality compounders with irritants: AMZN, GOOGL

- Hated or ignored optionality: TSLA, DIS

- Over-owned but misunderstood tollbooth: NVDA

The trade is simple:

Use Galloway’s map. Ignore his implied weightings.

When a thesis becomes an asset class

Galloway’s talent is narrative compression.

Markets love clean stories. Allocators need them. Media amplifies them.

Eventually, a narrative crosses an invisible line:

From “non-consensus insight”…

To “consensus framework”…

To “product”.

“Long AMZN for robotics, long GOOGL for Waymo and AI, fade TSLA, dismiss legacy media, call NVDA a bubble” — this is now a packaged intellectual product.

At that stage:

- First-order trades are mostly done.

- Easy multiple expansions are harvested.

- Skepticism itself becomes crowded.

What remains:

- Where the story overshoots reality (politics, regulation, geography).

- Where the story ignores the messy path (local vs global, oligopoly vs monopoly).

- Where disgust, boredom, or moral judgment created pricing blind spots.

The most interesting trades aren’t where Galloway is “wrong”.

They’re where he’s right on direction and the crowd is wrong on payoff.

Amazon: robots, margins, and pitchfork risk

The Amazon bull case is now standardized in every pitch deck:

- Increasingly robotized warehouses.

- Labor cost per package falling.

- Retail margins climbing from thin to respectable.

- AWS printing cash in the background.

This is no longer secret alpha. It’s in every sell-side model.

Robotics already appears in the numbers:

Throughput up. Errors down. Margins better.

Low-teens revenue growth. ~30 forward P/E. Quality multiple for quality asset.

The missing line in most models: political entropy.

If Amazon “wins” robotics hard by 2026:

- Fewer humans per cubic meter of warehouse.

- Higher profits per region.

- Earnings calls openly celebrating “productivity.”

Then the other side arrives:

- Local TV segments about lost warehouse jobs.

- Union campaigns built around “robot taxes.”

- Mayors and governors demanding concessions for permits and incentives.

Congress doesn’t need to understand CUDA to tax a robotic warehouse.

Automation is popular in markets and deeply unpopular in local politics.

This doesn’t break Amazon.

It simply caps the terminal margin fantasy that underpins the wildest robotics takes.

Add AWS: still dominant, but no longer mythic.

- Azure grew faster, powered by OpenAI connection.

- Google Cloud is now a real business, not a hobby.

- AWS is a high-margin oligopolist, not a monopoly.

So in 2026, Amazon is:

- A logistics + cloud oligopolistic platform.

- With real automation upside.

- And a growing regulatory target.

This is a core hold, not a secret rocket.

The edge is not mentally overpaying for robots everyone already knows about — and respecting the political ceiling on how perfect those margins can get.

Galloway’s implicit position: Bullish — top pick

Reality adjustment: Core compounder, but temper robotics euphoria

Alphabet: cheap empire, expensive remedies

Alphabet’s core is brutally simple according to Galloway:

- Global ad machine (Search + YouTube).

- Net cash fortress.

- Cluster of AI/autonomy options.

The market gives this maybe a high-teens forward multiple.

That’s low for:

- This cash flow quality.

- This growth vs GDP.

- This balance sheet.

The reason is also simple: antitrust is no longer background noise.

Most investors behave as if the path were:

- “Google gets a slap on the wrist.”

- “Default payment terms change.”

- “Business as usual resumes.”

But there’s a non-zero probability of structural remedies:

- Partial spin-offs (YouTube, ad stack, Chrome).

- Forced separations of data, distribution, or bidding systems.

The twist Galloway rarely mentions: some “punishments” could increase value.

YouTube standalone at mature, realistic revenue multiples can support a huge portion of Alphabet’s current cap on its own.

Spin-offs + reduced regulatory heat + clearer narratives = often higher combined valuations than one opaque conglomerate.

So the real antitrust range is:

- Mild remedies = modest annoyance.

- Structural remedies = medium risk, but also medium chance of forced value unlock.

Waymo follows the same pattern.

The best economic outcome for Alphabet isn’t a perfectly global, uniform autonomy platform.

It’s balkanization:

- Waymo dominates a handful of high-value cities.

- Other regions develop local champions.

- Standards remain fragmented. Interoperability remains messy.

Global monopoly = more politics, more commoditization, more copying.

Local oligopolies = less utopia, more profit.

On AI: the “Google missed AI” story is stale.

- Gemini improves fast.

- TPUs and data centers are serious infrastructure.

- Search + Workspace + YouTube give native embed points for models.

Alphabet in 2026:

- A cash gusher at a market multiple.

- With AI and autonomy upside.

- And a legal overhang that is as much a feature as a bug for long-term holders.

This belongs near the top of almost any concentrated large-cap tech portfolio.

Under-owned relative to quality. Over-penalized for courtroom noise.

Galloway’s implicit position: Bullish, but less sexy than Amazon

Reality adjustment: Tilt toward GOOGL over AMZN — antitrust is a disguised catalyst

Tesla: the hate-owned call option

The current Tesla script that Galloway hammers:

“It’s just a car company at a tech multiple, run by an erratic CEO.”

Accurate enough to sound smart.

Incomplete enough to be mispriced.

Break Tesla into parts:

- Auto (EVs).

- Energy (storage, solar, grid).

- Autonomy (FSD, robotaxi).

- Robotics (Optimus).

At scale, an 8M unit auto business with ~$8–10K profit per car supports a serious car-co valuation.

That alone doesn’t explain today’s market cap.

The rest is optionality. The striking part is how much that optionality has already deflated:

- At peak mania, the market priced non-auto dreams at something like $700–800B.

- Today, implied optionality looks closer to $300–400B, depending on assumptions.

Meanwhile, FSD and Optimus haven’t stalled.

Software improved. Hardware iterated. Data compounded.

Markets now effectively say:

- “Some of this might work, but probably not fully, and definitely not soon.”

That’s very different from:

- “This can’t fail.”

When technical progress outpaces belief, asymmetry appears.

FSD is messy, but it scales in the right dimension: miles.

Waymo runs beautiful robotaxis in geofenced zones.

Tesla runs imperfect autonomy software across millions of cars in unconstrained environments.

If Tesla pushes FSD toward reliable L4 in even a slice of use cases, the math for:

- Robotaxis, or

- High-value driver assistance subscriptions

becomes non-linear.

Failure is largely in the price.

Partial success is not.

Optimus is similar.

Humanoids aren’t elegant robotics theory.

They’re elegant industrial pragmatism:

- Walk into existing factories.

- Use existing tools and layouts.

- Replace tasks, not entire systems.

If Optimus reaches “boring, reliable, safe” at a tolerable cost curve, the value isn’t in sci-fi.

It’s in a shift in the long-run cost of certain types of labor.

Most models assign that a very low probability and a very long runway.

Reasonable, but probably too conservative for a company that already proved execution in hardware-plus-software at global scale.

Governance risk is obvious and fully broadcast:

- Musk distractions.

- Board concerns.

- Political cross-currents.

This is already in the discount.

Which is exactly why TSLA belongs in any serious contrarian basket.

By 2026, Tesla looks less like a car name and more like:

A volatile, macro-sensitive call option on autonomy + robotics, collateralized by a global EV business.

Sizing is everything.

Wrong as a 20% conviction bet.

Potentially compelling as a 3–7% position where downside is “good car company” and upside is “parts of the optionality actually work.”

Galloway’s implicit position: Bearish / Fade

Reality adjustment: Asymmetric optionality mispriced — buy what smart money hates

Disney: the physical world refuses to die

The Disney narrative Galloway propagates is lazily linear:

Legacy media dies → streaming saturated → cord-cutting kills ESPN → Disney is toast.

Reality is more layered.

Most of Disney’s durable value sits where bits can’t easily go:

- Parks and resorts.

- Cruises.

- Experiences.

- IP monetization in the physical world.

A single family trip to Disney is now a multi-year savings event for many households.

Once there, a 10–20% price hike on tickets or food is tolerated more often than not.

That’s real pricing power.

Recent years have shown:

- Parks and experiences revenue growing nicely.

- Operating income in that segment compounding.

- Cruises scaling with strong demand.

No LLM can recreate a five-year-old’s meltdown on Main Street.

No deepfake can replace the social currency of “we took the kids to Disney.”

Streaming is no longer an arms race; it’s a margin repair job.

- Disney+ shifted from “burn cash for subs” to “charge more, churn less.”

- Bundles with Hulu and ESPN+ add stickiness.

- Content spending is becoming disciplined.

Streaming for Disney is a distribution pipe, not the kingdom.

The kingdom is the IP and physical footprint.

ESPN sits in between:

- Cord-cutting hurts the old bundle.

- Live sports still command top-tier ad dollars.

- Future direct-to-consumer offerings and new bundles are optionality, not lifelines.

If ESPN were public standalone, it would likely trade at a solid multiple of its contracted cash flow.

Inside Disney, it’s treated as a liability in a “legacy media trash” basket.

Disney’s IP library ages like an asset, not a cost:

- Frozen still monetizes a decade later.

- Marvel and Star Wars still drive toys, costumes, cruises, and park lands.

Content at Disney isn’t just a P&L line. It’s a set of nodes in an experience network.

By 2026, Disney looks like:

- A real-world experiences oligopoly with inflation leverage.

- A now-sane streaming business.

- A misperceived sports cash engine.

- A deep, global IP reservoir.

Valuation in the high-teens forward P/E range for that mix is closer to “value with call options” than “media hospice.”

This is the anti-hype name in a hype-drunk market.

Galloway’s implicit position: Bearish — legacy doomed

Reality adjustment: Real-asset play with pricing power — buy what finance ignores

Nvidia: bubble narrative, cash-flow reality

Calling Nvidia a bubble is social signaling now, notes Galloway in his more nuanced segments (which his fans ignore).

It sounds cautious and sophisticated.

It often ignores arithmetic.

Look at the rough shape of numbers through 2024:

- Data center revenue exploded.

- Margins in that segment ran in the 70%+ range.

- Free cash flow scaled with it.

A 40–50x P/E looks expensive in isolation.

Against triple-digit growth, it produces a PEG ratio around or under 1.0.

That’s not a “tulip” profile.

It’s the profile of a market that:

- Knows the current growth rate is unsustainable.

- Already assumes a sharp slowdown.

If growth decelerates, but not as violently as feared, the “bubble” quietly melts into an over-discounted growth compounder.

China’s model flood doesn’t break this.

It may support it.

Models and compute are separate layers:

- Open models compress model economics.

- They expand usage, experimentation, and inference.

- All of that eats compute.

Cheap Chinese models could reduce cost per query and increase query volume.

That’s a compute story more than a model story.

Export controls are a real constraint.

But the market repeats the narrative louder than the numbers justify.

- Nvidia already designed China-specific SKUs.

- Growth outside China has offset much of the lost upside.

- Policy can tighten, but that tail risk is partly embedded in the multiple.

Custom silicon from hyperscalers is rational:

- It reduces dependence on a single vendor.

- It optimizes for internal workloads.

- It still co-exists with Nvidia for external workloads and cutting-edge research.

CUDA and Nvidia’s tooling ecosystem are deeply entrenched.

Switching costs in software and talent are real.

By 2026, Nvidia is:

- A cyclical, dominant AI compute supplier.

- Priced for visible deceleration, not fantasy.

- Sitting where AI capex, national security, and corporate strategy intersect.

The key question isn’t “is this a bubble?”

It’s “does AI capex keep compounding globally over the decade?”

If yes, Nvidia doesn’t need to be perfect to justify a premium.

It only needs to stay central.

Galloway’s implicit position: Bearish / Bubble

Reality adjustment: AI tollbooth already discounted for slowdown — buy fear, not euphoria

The real setup for 2026: beyond the podcast

The meme conclusions of Galloway’s framework are the least interesting trades:

- “Amazon wins automation” is consensus.

- “Waymo better than Tesla” is consensus.

- “Nvidia bubble” is consensus skepticism.

Alpha rarely hides in consensus conclusions.

It hides in how those conclusions are implemented.

The sharper inversions:

- Tesla is most interesting precisely because every sophisticated investor feels virtuous trashing it.

- Disney is most mispriced because finance is obsessed with streaming spreadsheets and blind to physical experiences.

- Nvidia’s biggest risk isn’t valuation, but long-term AI capex. Valuation is simply the language fear speaks.

The portfolio question for 2026 isn’t “who’s right, the professor or his critics?”

The better question:

- What mix of these imperfect giants pays most, net of their narratives, politics, and cycles?

The answer is less exciting than a podcast prediction.

More useful too.

Concrete positioning

Positioning for this landscape looks less like hero calls and more like weighted exposure.

1. Anchor in AMZN and GOOGL, but tilt toward GOOGL

- Treat both as core compounders, not moonshots.

- Size them together in the 25–40% range for a concentrated large-cap tech sleeve.

- Tilt slightly toward GOOGL over AMZN:

- Alphabet carries antitrust noise, but also forced value-unlock upside.

- Amazon’s robotics story is fully socialized; politics is not.

Use real antitrust panic in GOOGL as buy-the-fear events unless remedies clearly crush Search economics.

2. Use TSLA as a capped-size, high-vol optionality bet

- Cap Tesla at ~3–7% of total equities.

- Accept 40–50% drawdown risk without leverage.

- Make peace with governance chaos as the cost of owning:

- FSD moving from impressive to monetizable.

- Optimus moving from demo to boring industrial tool.

The moment the market starts liking Tesla again without commensurate progress, the asymmetry fades.

The thesis here is “improving tech, discounted belief,” not “Musk infallibility.”

3. Accumulate DIS as stealth real-asset + inflation hedge

- Think of Disney as a hybrid of:

- Global theme park / experiences REIT with pricing power.

- IP royalty machine.

- Streaming / sports distribution leg.

- A 5–10% allocation fits investors who value cash flow and can tolerate narrative negativity.

Treat streaming-related selloffs as entry or add points if:

- Parks stay full.

- Free cash flow trends up.

- Debt stays manageable.

4. Hold NVDA as an AI tollbooth, add only on real fear

- Size Nvidia in the 5–10% range as an AI infrastructure core.

- Add only during genuine panics:

- AI “winter” headlines.

- Macro squeezes on capex.

- Policy shocks that look scary but leave the global capex trend intact.

Don’t chase parabolic extensions.

Let volatility do the work.

Focus on data center revenue, not social sentiment.

5. Think in weights, not winners

The sharper stance for 2026:

- Overweight: GOOGL, AMZN as core.

- Targeted contrarian: TSLA, DIS as mispriced optionality.

- High-quality growth tollbooth: NVDA as AI infrastructure.

And one final, unfashionable view:

The edge over the next cycle will come less from predicting which soundbite ages best.

It will more likely come from owning the unpopular but cash-generative,

and sizing the beloved but risky with discipline —

while everyone else trades the narrative instead of the payoff.

Galloway gives you the map. You choose the route — and the size of your bet.