FintechWerx (WERX): A $2 Million Asymmetric Option on Survival

A fragile business, a constrained asset base, and a very specific kind of speculation

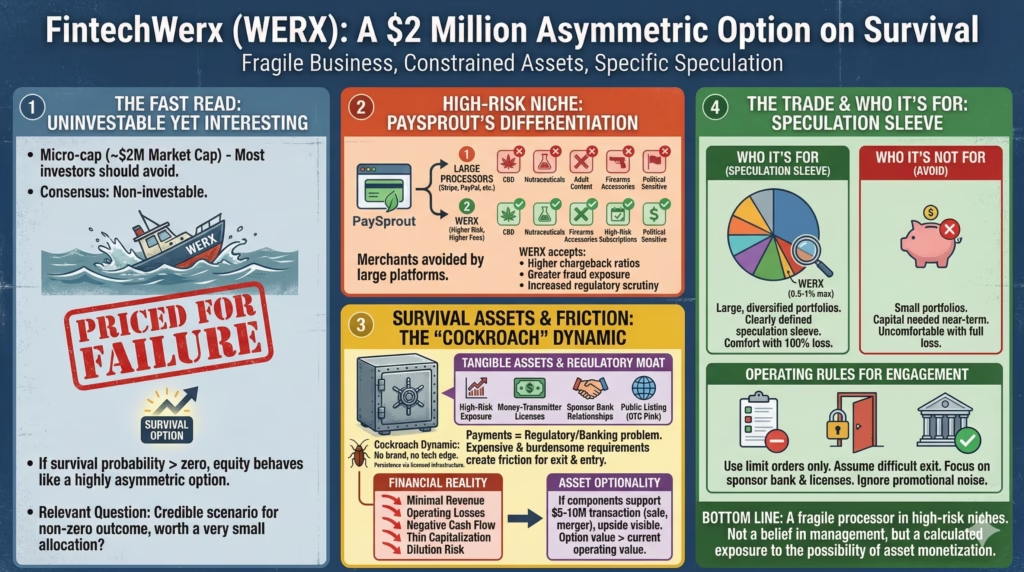

The Fast Read

FintechWerx (WERX) is a micro-cap payment processor most investors will reasonably consider non-investable. For the vast majority, that assessment is probably correct.

That same consensus, however, is what creates the only source of interest here.

With a market capitalization around ~$2M, the stock trades as if failure is close to inevitable. If the actual probability of survival is even modestly higher than what the price implies, the equity behaves less like a conventional stock and more like a highly asymmetric option on regulatory and operational continuity.

WERX’s PaySprout platform serves merchants that large processors like Stripe, Square, PayPal, and Shopify often avoid: CBD, nutraceuticals, adult content, firearms accessories, higher-risk subscription models, and certain politically sensitive use cases.

The company’s tangible assets are limited, but include:

- Exposure to high-risk payment processing

- Whatever money-transmitter licenses and sponsor bank relationships remain in place

- A functioning public listing

The underlying business is weak: low revenue, negative cash flow, recurring dilution, and very limited liquidity.

The key question is not, “Is this a good company?”

The relevant question is: “Is there a credible scenario where this does not go to zero — and is that scenario worth a very small allocation within a diversified portfolio?”

For most investors, the answer remains no.

For a small subset managing a tightly controlled speculation sleeve, WERX represents a narrowly defined survival-option trade.

When “Uninvestable” Becomes the Starting Point

Markets tend to misprice optimism more often than pessimism.

The prevailing view on WERX is straightforward:

- Nano-cap

- OTC Pink Sheet

- Ongoing dilution

- Extremely illiquid

- Weak operating fundamentals

Most disciplined investors stop there, appropriately. But when consensus converges this strongly, the price can begin to reflect near-certainty of failure, rather than merely elevated risk.

At that point, the analytical frame shifts. The question is no longer:

- “Can this compound capital?”

It becomes:

- “Is the probability of a non-zero outcome meaningfully above zero?”

WERX trades as if extinction is the base case. If the outcome ends up being “barely survives” rather than “fully fails,” the repricing effect on a $2M equity can be material.

This setup does not require belief in the business model. It relies on understanding how asymmetry behaves near the lower bound of valuation.

Operating Where Large Processors Decline

PaySprout’s surface-level description — gateways, onboarding, POS, e-commerce — is unremarkable. The differentiation lies elsewhere.

It lies in merchant selection.

Large payment platforms maintain extensive prohibited-use lists:

CBD products, certain supplements, adult content, firearms accessories, elevated chargeback subscription models, and some political fundraising.

Demand from these merchants persists, but flows to smaller, higher-risk processors and independent sales organizations willing to absorb:

- Higher chargeback ratios

- Greater fraud exposure

- Increased regulatory scrutiny

In exchange, these processors earn higher fees. While mainstream payment processing often produces 10–20% gross margins, high-risk acquiring can reach materially higher levels.

Given the scale of U.S. card volumes, even a very small share of “orphaned” transactions represents a meaningful addressable niche.

WERX does not need to capture much of this flow for the economics to look different relative to a $2M market cap. There is no clear evidence it has done so yet — but this niche explains why companies like this can persist longer than expected.

Licenses, Sponsor Banks, and Survival Friction

Payments is fundamentally a regulatory and banking problem, not a technology one.

Operating at scale typically requires:

- Money-transmitter licenses across relevant states

- An active sponsor bank relationship

- Card-network compliance

- Ongoing KYC, AML, and PCI infrastructure

These requirements are expensive and operationally burdensome. As regulation has tightened and banks have de-risked, many smaller processors have exited simply by losing sponsorship or failing compliance thresholds.

The operators that remain are rarely impressive. They are, however, difficult to dislodge.

This is the core of the “cockroach” dynamic:

- No brand advantage

- No technological edge

- No operational excellence

Only the fact that maintaining licensed, bank-sponsored infrastructure creates friction for both exit and entry.

WERX’s speculative case rests entirely on this persistence:

If it maintains sponsor relationships and enough of its license footprint while competitors disappear, the residual infrastructure may have value exceeding today’s equity price.

This is not a growth narrative. It is a salvage and survival narrative.

Financial Reality Remains Poor

The reported financials are unambiguous:

- Minimal revenue

- Ongoing operating losses

- Negative cash flow

- Thin capitalization

- Continued dilution risk

On any conventional metric, WERX fails. That is expected. This is not a quality or value investment in the traditional sense.

The framing therefore shifts from operating performance to asset optionality:

- A struggling processor

- With licenses, sponsor relationships, and merchant contracts

- Inside a public shell

If those components together support a $5–10M transaction in a sale, merger, or restructuring scenario, the upside relative to current valuation becomes visible. There is no assurance of such an outcome — only the possibility.

At this scale, option value can outweigh current operating value.

Illiquidity as a Structural Feature

WERX trades infrequently, often with wide spreads. This limits participation.

Institutions cannot engage due to liquidity, compliance, and reputational constraints. The shareholder base consists primarily of small retail participants, legacy holders, and occasional niche funds.

As a result:

- Price discovery is uneven

- Single buyers or sellers can move the stock

- News events can create outsized moves

For investors requiring liquidity, this is prohibitive. For a deliberately small, long-duration speculation, interim liquidity matters less than terminal outcomes.

This does not mitigate the risk. It defines it.

A Scenario-Based Lens

Discounted cash-flow analysis is not meaningful here. Scenario analysis is.

1. Gradual Erosion (Most Likely)

- Business continues at low scale

- Cash pressure persists

- Dilution continues

- Equity trends toward negligible value

2. Survival and Asset Monetization (Lower Probability)

- Acquisition for licenses, merchant base, or shell

- Or modest revenue stabilization leading to re-rating

- Potential transaction value in the $5–10M+ range

3. Abrupt Failure

- Loss of sponsor bank

- Regulatory intervention

- Capital exhaustion

Expected value remains negative. That is why this is not “cheap” in a traditional sense. The appeal, if any, lies entirely in tail outcomes.

The Public Shell Consideration

U.S. micro-cap shells occasionally become vehicles for reverse mergers. In such cases:

- The existing business may be sidelined

- New assets are injected

- Valuation resets independently of legacy operations

This outcome is uncommon, but it represents an additional non-zero exit path.

Context Within Fintech

For investors seeking standard fintech exposure, there are clear alternatives:

- Nu Holdings (NU)

- SoFi (SOFI)

- Global X FinTech ETF (FINX)

These offer scale, liquidity, transparency, and conventional growth paths.

WERX is not a discounted substitute. It is a different instrument entirely — a speculative position tied to regulatory survival and asset optionality.

Who This Is — and Is Not — For

Most investors should avoid this entirely.

It is inappropriate for:

- Small portfolios

- Capital needed for near-term use

- Investors uncomfortable with full loss scenarios

The only reasonable audience:

- Large, diversified portfolios

- A clearly defined speculation sleeve

- Comfort with 100% loss on individual positions

Even then, WERX belongs at the margin: 0.5–1% at most, mentally written down at entry.

Operating Rules for Engagement

If one chooses to engage:

- Use limit orders only

- Assume exit will be difficult

- Focus on sponsor bank status, licensing continuity, and cash runway

- Ignore promotional noise

On the upside, predefined profit targets matter. In option-like structures, harvesting gains after a 2–3x move is often rational.

Bottom Line

Stripped of narrative:

- WERX is a fragile payment processor

- Operating in high-risk niches

- With weak financials

- Potentially holding regulatory and structural assets that exceed current valuation

For most investors, ignoring it entirely is the correct decision.

For a small minority, it is a narrowly scoped survival option — not a belief in management or execution, but a calculated exposure to the possibility that the company persists long enough for its remaining assets to be monetized.

Whether that exposure belongs in a portfolio is a design decision, not a conviction play.