Planet Labs (PL): The Time Machine That Can’t Pay Rent

Owning a live history of Earth, priced like a busted industrial

The Fast Orbit

Planet Labs is the rare company where the asset is world‑class and the business is mediocre.

On one side: a decade of daily, global imagery. A time‑stamped, independent visual record of Earth that no one else has and no one can recreate.

On the other: a cost structure closer to aerospace, revenue growth closer to ex‑growth SaaS, and a stock that trades under 1x EV/Sales because the spreadsheet refuses to lift off.

At today’s numbers, Planet needs roughly 85% more revenue just to hit operating break-even, while growth has slowed from the mid‑40s to roughly 10%.

The equity is not a bet on smooth compounding. It is an ugly, long‑dated call option on a future where regulation, war, climate litigation, AI fakery, and security panics suddenly make a planetary truth machine worth real money.

The core question isn’t “Is PL cheap?”

It’s: “Is this the tail risk worth owning?”

A Beautiful Asset, A Heavy Business

Planet built what every space startup pitch deck dreams about: more than 200 satellites imaging the entire land surface of Earth, every day, at a few meters’ resolution.

Design, manufacturing, launches, operations, downlink, processing, cloud delivery — all vertically integrated.

On paper, that looks like a moat. On the income statement, it looks like overhead with marketing copy.

The thesis was simple: the world would pay for daily global coverage. Insurance, agriculture, infrastructure, ESG, defense. Anyone who cares about “what changed where, today.”

Reality is duller. Most customers don’t need “every day.”

- Farmers are fine with weekly.

- Infrastructure with monthly.

- Many ESG and climate use cases with free, lower‑frequency government data.

Daily coverage is magical in a demo and overkill in a budget review.

Planet built for maximum temporal intensity; the market pays for “good enough.”

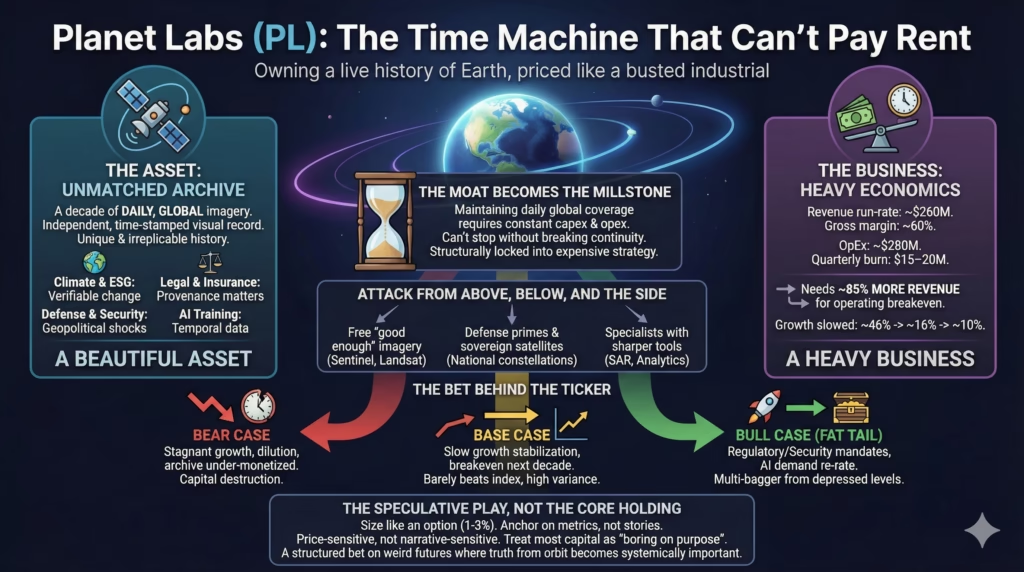

When the Moat Becomes the Millstone

Planet’s brag is also its trap: imaging the entire Earth’s landmass, every day.

Maintaining that continuity means:

- constantly replenishing satellites as they age and decay

- running global ground infrastructure

- processing and storing petabytes of imagery continuously

The fixed cost is relentless, but the incremental price customers are willing to pay for “every day” instead of “every few days” collapses quickly.

Worse: the company can’t just switch it off.

The truly unique thing Planet owns is not each day’s picture, but the unbroken time series. Stop imaging globally for six months and the one real moat — continuity — breaks.

So Planet is structurally locked into the expensive version of its own strategy.

The moat is real. It just has to be paid for every quarter.

The Math That Gravity Enforces

Recent numbers tell the story cleanly:

- Revenue run‑rate: roughly $260–270 million

- Gross margin: about 60%

- Annual operating expenses: roughly $275–280 million

- Quarterly operating loss: $25–30 million

- Cash burn (free cash flow): $15–20 million per quarter

- Cash pile: $350–400 million

At 60% gross margin, that cost base requires around $460 million of revenue to break even.

Current revenue is about $250 million.

So Planet needs something like 85% growth just to stand still on profit.

Meanwhile, growth has decelerated:

- ~46% → ~16% → ~10% over three fiscal years.

At 10% growth, break-even drifts into the early 2030s, assuming the cost base holds and no one demands fresh capital.

This is why the stock trades below 1x EV/Sales. The market is not debating survival, it is discounting time and dilution.

The physics bill arrives whether investors feel patient or not.

Attack From Above, Below, and the Side

If Planet’s economics were bad but the market was empty, the story would be simpler. It isn’t.

Pressure comes from three directions:

Free “good enough” imagery

Sentinel‑2 (ESA) and Landsat (NASA/USGS) pump out huge volumes of open imagery. Resolution is lower, revisit slower, but for many use cases — crop monitoring, deforestation, basic ESG — it’s fine.

Startups and incumbents alike build commercial products on top of free government pixels. Each one is a customer that never needs a Planet subscription.

Defense primes and sovereign satellites

The richest buyers — defense and intelligence agencies — already work with Maxar, L3Harris, Lockheed, Northrop, and local primes. These players:

- bundle imagery into multi‑billion programs

- build “national” constellations

- sell governments on sovereignty, not subscriptions

As launch costs fall, more countries decide they would rather own their own eyes than rent someone else’s.

Specialists with sharper tools

SAR constellations see through clouds and at night. Analytics‑heavy players tune products for real‑time defense use cases. Chinese providers flood price‑sensitive markets.

Planet’s pitch of “we image everything, every day” collides with a blunt customer question:

“Do you give exactly what is needed, when it is needed, with the right analytics?”

Too often the answer is “almost.” Almost is hard to budget for.

The Archive You Can’t Rebuild

Here is the twist: despite the ugly unit economics, Planet quietly owns something that money can’t buy retroactively.

A decade‑long, daily, global visual log of Earth from roughly 2014 onward.

- Not cherry‑picked.

- Not only where customers pointed.

- A systematic time‑lapse of a chaotic decade: war, climate, construction, borders, deforestation, glacial retreat.

No one can go back and reimage 2017, or 2020, or 2022.

This matters in domains where history and provenance matter more than pixel count:

- Climate and ESG disclosure rules needing verifiable baselines and change over time.

- Legal disputes and insurance claims asking what was where, and when.

- Sanctions enforcement and trade surveillance.

- A world of synthetic media that needs trusted chains of custody.

Regulators are tightening climate disclosure (EU CSRD, ISSB standards). Courts and international bodies are nudging toward higher evidentiary standards. Insurers are leaning harder on long‑term data to price risk.

In that world, a neutral, continuous, third‑party record starts to look less like “cool space startup” and more like infrastructure for truth.

Most competitors can offer imagery. Very few can offer ten years of daily context.

Why “Someone Will Just Buy It” Is Weak Comfort

The standard bull line for wounded growth stories is: “a bigger player will scoop them up.”

For Planet, the fantasy is a defense prime, hyper‑scale cloud, or geo‑analytics platform paying a fat premium for the archive and folding operations inside a larger stack.

Maybe. But as a downside floor, the argument is fragile.

A rational buyer sees:

- A unique archive, yes — but also

- A business that must keep launching satellites and burning cash to keep that archive continuous

- Capabilities that can be partly replicated with a smaller, cheaper constellation tuned to specific needs

DigitalGlobe, the closest comparable, sold around 5x revenue back in 2017. Planet trades under 1x.

Apply 5x to Planet’s current revenue and the theoretical “takeout” EV lands near $1.25 billion, which roughly equates to $2.50–3.00 per share after cash and shares — not far from where the stock has already traded.

M&A is upside optionality, not a safety net. Treating it as a floor is wishful thinking.

What Has to Go Right

For PL to justify more than dead‑money status, the future has to kink, not glide.

Roughly, that looks like one or more of:

- Regulation mandates satellite‑verified reporting. Climate, forestry, shipping, agriculture, methane — choose a sector. Once verification is written into law, budgets appear automatically. Archival coverage becomes less “nice” and more “non‑negotiable.”

- Security regimes escalate. A geopolitical shock pushes commercial Earth‑observation into the heart of defense planning. Planet’s existing ties with US agencies deepen into larger, longer, more strategic contracts.

- AI makes the archive a core training set. Rich, labeled temporal data becomes must‑have raw material for computer vision models. Tech giants dislike depending on single‑source suppliers they don’t control; owning the tap suddenly looks attractive.

- Product focus tightens. Planet shifts from “image the planet, sell subscriptions” to deeply vertical, high‑value products in a few industries, even if headline growth slows. Less vanity coverage, more money per pixel.

Each of these paths is plausible, none are guaranteed. The current valuation, however, prices in very little of this fat‑tail upside in a market that routinely overpays for middling SaaS.

The More Likely Grind

Markets often choose the dull outcome over the dramatic.

A more probable path for Planet looks like:

- Growth drifts to mid‑single digits.

- Gross margins stall around 60–62%.

- Cost cuts nibble at burn but never transform the economics.

- Occasional equity raises and stock‑based compensation slowly dilute holders.

- Investor attention migrates elsewhere while PL trades in a low single‑digit band for years.

The risk is not just losing money. It is losing time while capital sits in something that doesn’t compound.

With T‑bills above 4% and broad equity indices historically compounding around 8–10%, any risky single name has to clear a higher bar now.

A realistic probability‑weighted view of PL might land in high‑single‑digit annualized returns if things go moderately right — barely above passive alternatives, with far more variance and hassle.

The Bet Behind the Ticker

Strip away the romance and the trade looks roughly like this:

- Bear case (material probability)

Growth stagnates, pricing pressure builds, regulation arrives slower than hope, and dilution continues. The archive remains under‑monetized. Equity drifts toward irrelevance; capital destruction is large. - Base case (most probable)

Growth stabilizes in the low‑to‑mid teens. Costs are trimmed but not transformed. Break-even lands early next decade. The stock doubles over many years, but through a long, choppy road that barely outperforms an index. - Bull case (fat tail)

One or more non‑linear catalysts — regulatory mandates, defense mega‑contracts, AI training gold rush, authenticity infrastructure — re‑rate the entire category. Sales multiple expands to something like 3–5x; the stock becomes a multi‑bagger from depressed levels.

That is the actual shape of the distribution: a wide, flat middle, painful left tail, and a right tail that depends on the world getting stranger and more litigious.

The Speculative Play, Not the Core Holding

For a real‑world portfolio, Planet Labs fits a very specific slot.

It is not a core holding.

It is not retirement capital.

It is a structured bet on weird futures.

A disciplined stance looks something like:

- Size it like an option, not a belief system.

Keep exposure small — on the order of 1–3% of a total portfolio at most. Large enough to matter if the right tail pays off. Small enough that a zero is survivable and forgettable. - Anchor on hard metrics, not stories.

Track four things ruthlessly over time:

- Revenue growth trend (does it hold >15% or sink toward low single digits?)

- Gross margins (do they creep toward 65%+, or stagnate around 60%?)

- Operating cash flow (is there a real path to self‑funding?)

- Share count (is dilution staying modest or quietly compounding?) Pre‑commit to exit or cut if these trend the wrong way for several quarters in a row. No loyalty to logos, only to math.

- Be price‑sensitive, not narrative‑sensitive.

Enter or add when valuation is washed out and fundamentals are at least stable. Avoid chasing on AI or defense‑related hype spikes; that is when the optionality is most expensive and the risk‑reward worst. - Treat most capital as “boring on purpose.”

For long‑term wealth, broad equity funds, high‑quality cash‑generating businesses, and safe yield instruments remain far better foundations than exotic space stocks. Planet is dessert, not dinner. - Take a side, not a slogan.

For curious, risk‑tolerant investors, a small, consciously speculative position in PL is defensible as a bet that truth from orbit becomes systemically important — in law, finance, security, and AI. For everyone else, the cleaner move is simple: enjoy the story from the sidelines, let indexes and defense primes carry the space exposure indirectly, and allocate serious money to assets that compound without needing the world to break in exactly the right way.