EnerSys: The Battery Play Everyone Wants to Love But Probably Shouldn’t

When the slides shout AI + IRA and the math whispers 2–5% a year

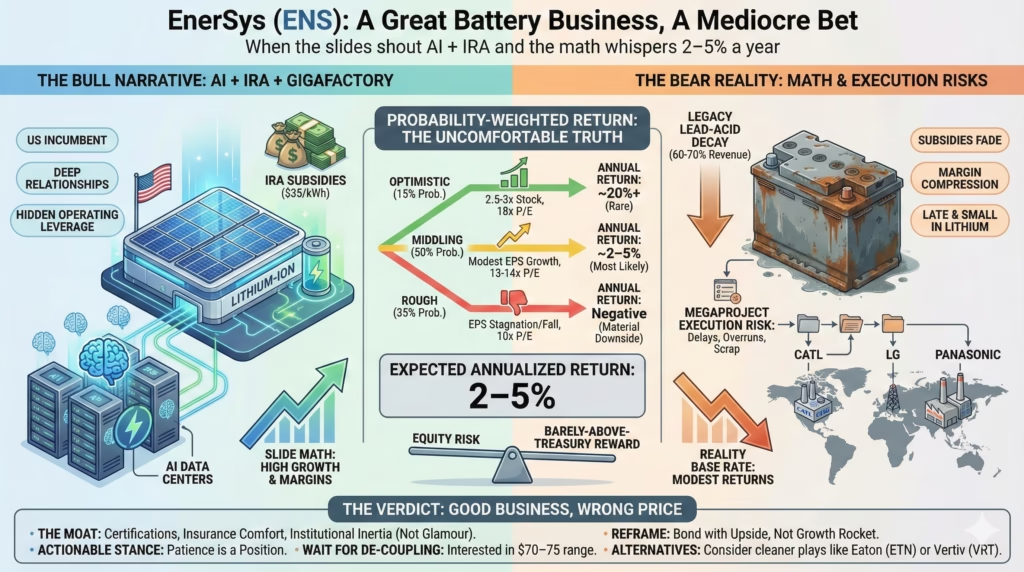

EnerSys looks like the perfect 2020s stock: batteries, AI data centers, a U.S. gigafactory, and fat subsidies. Underneath the narrative, it’s an excellent niche industrial… priced like a bond with volatility.

The Fast Read on EnerSys

EnerSys is the kind of company institutions love: boring, certified, reliable, hard to fire for choosing.

Roughly two‑thirds of its revenue and most of its profit still come from lead‑acid batteries — a legacy chemistry facing slow structural decline. The “future” is a planned $500M+ lithium‑ion gigafactory, heavily reliant on Inflation Reduction Act (IRA) subsidies and built in a market already dominated by giants like CATL.

On the surface, the stock looks fine: about $95 a share, around 13–14x recent earnings, a modest dividend, a clean balance sheet. It screens like a cheap way to own AI infrastructure and energy storage.

Run the numbers with realistic probabilities, and the picture changes: the 5‑year expected return clusters in the 2–5% range. That is equity risk for barely‑above‑Treasury reward.

EnerSys is not a bad business. In some ways, it is an excellent one. The moat, however, lives in certifications, insurance comfort, and institutional inertia — not in battery chemistry or gigafactory glamour. At the current price, the story is better than the stock.

Three Stories, One Problem

Most investor conversations about EnerSys orbit one of three narratives.

First: the bullish compounder story. Industrial batteries are essential for AI data centers, warehouses, telecom, and defense. EnerSys is a U.S. incumbent with deep relationships and an IRA‑blessed domestic lithium plant on the way. At ~13x earnings, the pitch is “misunderstood compounder with hidden operating leverage.”

Second: the secular‑loser story. EnerSys is chained to lead‑acid, late and small in lithium. Asian behemoths already own global lithium scale. By the time the gigafactory ramps, margins in both legacy and new tech are under pressure. The “pivot” just slows decline.

Third: the cynical but accurate story. The stock is not about batteries at all; it’s about slow institutions. Telecoms, militaries, and warehouse giants buy “career protection,” not watt‑hours. EnerSys sells permission — being on the certified vendor list, inside the insurance playbook, and pre‑approved by regulators.

Each contains truth. None, by itself, justifies paying up for ENS at today’s price.

What EnerSys Really Sells

On paper, EnerSys sells industrial batteries, chargers, and service to warehouses, telecoms, data centers, and defense.

Economically, it sells something else: blame avoidance.

If a hyperscale data center goes dark and the backup system was supplied by a long‑standing, certified, defense‑approved vendor, it’s bad luck. If it fails because procurement chose an unproven import to save 7% on capex, it’s a career event.

EnerSys sits inside that psychology. Over decades it has accumulated:

- UL files and telecom approvals embedded in RFP templates

- MIL‑SPEC qualifications that take years to replicate

- A service workforce with site‑specific knowledge and safety credentials

- A track record that makes underwriters and regulators comfortable

This “institutional permission” does not show up as goodwill on the balance sheet, but it behaves like a moat. Competitors can match chemistry faster than they can match trust.

That is the real business. Not “lead vs lithium”, but “outsider vs pre‑approved insider.”

The Lead‑Acid Gravity Well

The awkward truth: EnerSys is still a lead‑acid company with lithium aspirations.

Management has consistently indicated that roughly 60–70% of revenue is tied to lead‑acid products, likely an even higher share of gross profit. This is the cash engine being used to fund the lithium future.

Lead‑acid is not disappearing; it is decaying. In many backup and motive power applications, lithium wins over time on energy density, cycle life, and footprint. The best customers tend to move first.

Transitions like this rarely follow the tidy curves in investor models. They follow power‑law dynamics:

- Premium customers shift early to the new tech and take the fattest margins with them.

- What remains in the legacy pool skews toward cost‑sensitive, late‑adopting, low‑margin demand.

- Fixed costs spread over fewer units, amplifying margin compression.

Think Kodak’s film vs digital, or wireline vs wireless. Revenue doesn’t gently glide down. It falls in steps as key customer cohorts flip.

Even with lead‑acid volumes shrinking mid‑single digits annually and lithium growing 20%+ from a small base, lead‑acid still dominates the mix five years out. It doesn’t vanish. It just gets uglier.

EnerSys is using a structurally weakening legacy engine to finance a complex, capital‑intensive tech leap. That can work, but the margin for error shrinks every year the old cash cow erodes.

Lithium Dreams, Megaproject Reality

The South Carolina lithium‑ion gigafactory is the glossy centerpiece of the bull case.

The outline: ~$500M of capex, targeted 3–5 GWh of annual capacity, domestically produced cells that qualify for lucrative IRA 45X credits. The slide math is intoxicating: high utilization, subsidies layered on top of margins, a smooth ramp.

Reality has a different base rate. Industrial megaprojects:

- Run over budget and behind schedule with startling consistency

- Demand new capabilities in process engineering, supply chain, and quality control

- Punish mistakes through scrap, recalls, and reputational damage

EnerSys runs good factories. But running a big, integrated lithium cell plant is not the same game as running mature lead‑acid lines and assembling packs from outsourced cells.

The competition has been learning this the hard way for years: Tesla, LG, Northvolt, SK, Panasonic. Their bugs, recalls, and overruns are the tuition bill for building true scale.

EnerSys is showing up late to a class where the front row is already filled with giants sitting on an order of magnitude more capacity. While EnerSys battles first‑time execution risk, CATL can add another Nevada‑sized plant as an incremental project.

IRA credits soften the blow, but complexity does not respect subsidies.

Subsidies That Eat Themselves

Section 45X of the Inflation Reduction Act is the sugar rush under the lithium story: up to $35 per kWh in credits for domestic cell manufacturing, plus additional module incentives. For a 3–5 GWh plant, the cumulative numbers look enormous.

But subsidies in competitive, capital‑intensive industries tend to follow the same script:

- Early plants earn fat margins.

- Capital floods in to capture the subsidy.

- Capacity overshoots demand.

- Prices fall, margins normalize, equity returns disappoint.

Solar panels. Ethanol. Wind turbines. The pattern repeats: the subsidy ultimately accrues to end customers and politicians’ talking points, not to shareholders.

EnerSys is not in a position to dictate industry pricing. Once domestic capacity from LG, SK, Panasonic, and assorted upstarts ramps, all of them will be chasing the same hyperscale and industrial demand, armed with the same subsidies.

In that world, IRA credits are a 3–5 year margin bridge, not a permanent structural uplift. After the bridge, competition resumes on cost and reliability — in a market still dominated by global giants and Chinese scale, with or without direct Chinese imports.

If the investment case leans heavily on a U.S. tax credit outlasting politics and competition, it is exposed on two flanks that equity investors do not control.

Where the Quiet Edge Lives

With all that risk, it is easy to miss what actually makes EnerSys interesting.

The edge is not chemistry; it is entrenchment.

EnerSys is wired into:

- Procurement checklists at Fortune 500s

- Defense and telecom standards

- Insurance models for fire and downtime risk

- Local regulatory comfort with known vendors and procedures

As AI data centers proliferate and warehouse automation deepens, risk management tightens. Insurers, regulators, and boards get more conservative about fire, downtime, and cyber‑physical failures.

In that environment, “known good” vendors quietly gain leverage. Not explosive pricing power, but the right to stay on the short list and charge industrial, not commodity, margins.

Geopolitics may further reinforce this moat. Rising U.S.–China friction effectively narrows the field of acceptable vendors for critical infrastructure. Chinese battery supremacy matters less if Chinese batteries become politically unbuyable in sensitive verticals.

On top of that, EnerSys carries a relatively conservative balance sheet for its ambitions. If the IRA gold rush ends with a graveyard of overlevered battery startups, EnerSys could pick up tech, capacity, or talent at distressed prices.

None of this turns ENS into a 10x story. It does, however, justify calling it a durable industrial with a slow‑burn moat — at the right price.

Pricing the Probability Tree

At roughly $95 per share, EnerSys trades around 13–14x recent EPS of about $7–7.50, with operating margins in the low‑teens helped by mix and some subsidy tailwind.

Think in scenarios over five years:

- In an optimistic world, revenue grows mid‑single digits, IRA credits flow, the gigafactory ramps cleanly, lead‑acid declines prove manageable, and operating margins drift toward the mid‑teens. EPS could roughly double, the market might award an 18x multiple to a “proven compounder,” and the stock could 2.5–3x. Call that a 15% probability.

- In a middling world, lithium grows but never fully offsets faster lead‑acid erosion, IRA uplift is mostly competed away, and margins hover around current levels. EPS ends up modestly higher than today. The multiple stays about where it is for a solid but challenged industrial. Call that a 50% probability.

- In a rough world, the gigafactory overruns, lead‑acid margin compression bites harder, and the market re‑rates ENS as a structurally shrinking legacy play. EPS stagnates or falls, and the multiple compresses toward 10x. The stock is down materially. Call that a 35% probability.

Blend reasonable numbers under those weights and the expected annualized return falls into the 2–5% band.

That is the core problem. The bull path exists and is meaningful. The bear path is very real. The base case is okay but unexciting. Weighted together, they do not clear a rational equity hurdle when risk‑free yields sit near mid‑single digits and broad equities offer long‑term 7–9% expected returns.

A good business can be a bad bet at the wrong price.

The Move From Here

EnerSys is not a fraud, a fad, or a terminal dinosaur. It is a solid, strategically located niche industrial trying to cross a dangerous bridge from legacy tech to subsidized future.

As an operating company, that setup can work. As a stock at $95, the odds are not generous.

A disciplined stance looks something like this:

- Treat ENS at current levels as unattractive new money. The expected 2–5% return profile does not compensate for technology, execution, and policy risk. This is not an obvious place to stretch for upside.

- Get interested only if price and narrative de‑couple. In the $70–75 range, the character of the bet changes. At ~9–11x mid‑cycle earnings, legacy lead‑acid turns from “headwind” into “downside buffer,” and lithium/IRA become low‑cost call options rather than central to the thesis.

- If already long, reframe ENS as a bond with upside, not a growth rocket. Modest position size is key. Adding aggressively above $90–95 makes sense only if hard evidence emerges of durable margin expansion beyond subsidy effects. Strength north of $110, driven by AI/IRA headlines rather than fundamentals, is a reasonable place to trim.

- For “AI infrastructure + electrification” exposure, consider cleaner vehicles. Scale players like Eaton (ETN) or higher‑beta data center names like Vertiv (VRT) offer more direct leverage to the theme with less dependence on a single risky megaproject.

Practically, the watchlist for ENS should focus on three trip‑wires:

- Lead‑acid margins: a sustained step‑down would signal that the cash engine is degrading faster than the lithium story can repair it.

- Gigafactory execution: delays beyond ~2 years or 30–40% capex overruns would justify a structurally lower multiple.

- Institutional moat erosion: repeated large contract losses in telecom or hyperscale to newer vendors would mean the “permission rents” are no longer secure.

Until price, execution, or both reset the odds, EnerSys sits in an uncomfortable zone: a good company, a fashionable narrative, and a mediocre bet. Patience is a position. In this case, it is the better one.