Thermon (THR): The Oilfield Plumber That Might Become Climate Infrastructure

The market sees a dusty pipe-heating vendor. The hidden asset is the data stream wrapped around those pipes.

Thermon looks like an unsexy small-cap industrial chained to old energy. Underneath, it might be quietly building a compliance tollbooth for a more regulated, electrified world — and the market is only paying you for the boring part.

Why This Ticker Deserves Another Look

Thermon Group Holdings (THR) is not a story stock. It’s a mid‑$400m–$500m revenue industrial selling heat tracing, controls, and electric boilers so pipes don’t freeze, gum up, or blow up.

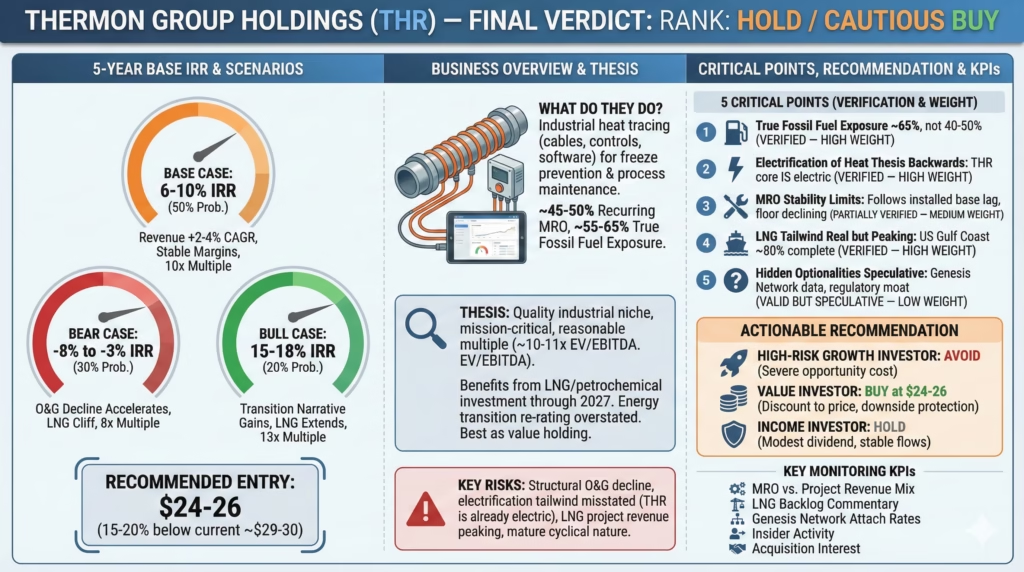

At ~9–10x EBITDA, modest leverage (about 1–1.5x), and high‑teens to low‑20s EBITDA margins, you’re paying a fair price for a competent, cash‑generative niche player.

The consensus view splits in two: optimists see an “energy transition enabler” industrial that deserves a better multiple; skeptics see a low‑growth, slowly eroding franchise leaning on acquisitions to mask stagnation.

Both are looking in the right place — the hardware — and still missing the most interesting piece: the networked monitoring layer, Genesis, that could morph from nice‑to‑have uptime insurance into de facto compliance infrastructure.

You don’t need to believe the Genesis upside to justify watching THR. You just need a price where the dull base case pays for itself and the optionality is free.

We’re not quite there. But we’re closer than the market narrative suggests.

Pipes, Not PowerPoints

Thermon’s core is industrial housekeeping, not innovation theater.

In cold or hazardous environments, process lines must stay within tight temperature bands. Thermon wraps these lines in electric heat tracing cables, sensors, controllers, and, increasingly, electric boilers via its Vapor Power acquisition.

The business splits into two rhythms:

Project work is cyclical and lumpy: refineries, LNG terminals, chemical and power plants, plus some food, rail, and “new energy” projects. It’s competitive and engineering‑heavy.

MRO — maintenance, repair, operations — is the quiet stabilizer. Once a plant is wired with Thermon gear, it needs spares, upgrades, emergency fixes. That’s higher‑margin, less cyclical, and emotionally priced at 3 a.m. in February when a line is freezing and every hour of downtime burns millions.

The numbers are solid, not exciting:

Revenue: mid‑$400m to low‑$500m.

EBITDA margin: high teens to low 20s.

Balance sheet: clean, low leverage, no obvious time bomb.

This is industrial plumbing with a decent parts habit, not a moonshot.

Filed In The Wrong Drawer

Thermon’s stigma comes from its origin story.

It grew up in refineries, petrochemical plants, and pipelines — all the places ESG decks now skip over. So investors reflexively toss THR into the “oilfield services hangover” bucket.

Meanwhile, the underlying mix has been drifting:

Less pure upstream oil & gas.

More LNG, chemicals, general industrial.

More “clean‑adjacent”: biofuels, battery materials, hydrogen pilots, carbon capture.

More electrified heating via its electric boilers and heat tracing.

The bulls’ story is simple:

Experience in dirty environments is transferable to new “clean” ones.

An installed base and spec status create inertia.

Peers like nVent trade richer; Thermon should close some of that gap as the “energy transition” label sticks.

If that’s all you see, THR is a low‑drama small‑cap industrial that might compound at low‑double‑digit returns from here.

The problem is that the bear case isn’t lazy — and it bites into that story.

The Bear With A Point

Start with growth.

Strip out acquisitions and price increases, and Thermon’s organic volume growth has often been flattish. Mid‑single‑digit “growth” looks less impressive if 3–4 points are pricing and the rest is bought.

Then the moat.

The old pitch of a practical duopoly in Western markets, protected by certifications, is aging badly. Asian competitors have spent a decade climbing the ladder, securing ATEX/IECEx/FM approvals and narrowing price gaps from ~40–50% discounts to more like 15–25%.

Post‑COVID, procurement teams are mandated to dual‑source. That means the lower‑cost certified supplier gets into the door, even if engineers still prefer Thermon. Every maintenance order becomes a more contested event.

MRO also isn’t a software subscription. Thermon’s products have gotten more durable; replacement intervals for modern cables can stretch to 20–25 years. Better engineering for customers ironically stretches the revenue cadence for the vendor.

Electrification, meanwhile, doesn’t explode the addressable market. Heat tracing is ancillary. Replacing huge gas‑fired boilers with electric ones is a big TAM, but Thermon is a niche electric boiler player, not Siemens or ABB.

Add it up and the skeptical view is: fair business, modest moat, tepid organic volume growth, facing slow competitive squeeze. A 9–10x EBITDA multiple is not a gift; it’s a reasonable price for that risk.

Annoyingly, much of this is right.

Which is exactly why the overlooked piece matters.

The Data Exhaust Nobody Is Pricing

Somewhere inside Thermon’s catalog sits the Genesis Network: a digital platform that monitors and controls heat tracing circuits, logging temperatures, failures, energy usage.

Today it’s sold as operational convenience: see your system remotely, avoid downtime, save energy. Nice, but not life‑changing.

That framing is outdated.

Industrial regulation is being slowly rewritten around continuous, auditable data:

The EU’s Carbon Border Adjustment Mechanism (CBAM) forces importers of carbon‑intensive goods to report embedded emissions with real data.

The Corporate Sustainability Reporting Directive (CSRD) drags thousands of companies into detailed, audited emissions disclosures, many needing granular energy‑use telemetry from suppliers and infrastructure.

Climate disclosure regimes in the US, UK, and elsewhere — even watered down — are pushing investors, insurers, and lenders to demand harder risk and emissions data.

If you run a high‑risk or energy‑intensive plant, “we think we used about this much energy” is dying. Continuous, time‑stamped telemetry is where the world is drifting. Not for fun. For liability.

In that world, a networked heat tracing system with embedded sensors is no longer just uptime insurance. It’s a node in your compliance stack.

The same wiring that keeps pipes in spec is also generating:

Temperature and performance logs.

Fault histories and incident data.

Energy‑use profiles that can be rolled into emissions accounting.

That data can feed regulators, auditors, insurers, banks, and internal risk dashboards. And once your compliance apparatus is wired into a specific monitoring layer, the cost of swapping vendors stops being “cheaper cable” and starts being “rebuild your data and audit trail.”

Compliance infrastructure has different economics:

It’s sticky because extricating it requires regulatory, not just technical, work.

It can carry recurring fees — monitoring, analytics, reporting — over and above hardware margins.

It can become a de facto standard if a few large operators consolidate on one or two platforms.

Nobody is valuing Thermon as if Genesis could become that.

Management barely talks about it. Bulls mention it as “digital upside.” Bears dismiss it as marketing.

But squint 5–10 years out:

A regulator, insurer, or major client quietly makes continuous monitoring compulsory for specific high‑risk facilities.

Auditors demand automated logs for process heating systems in emissions reports.

Global operators standardize on a single platform to simplify compliance globally.

Under those conditions, Genesis stops being a footnote and starts looking like a tollbooth on a narrow road.

This outcome is far from guaranteed. Customers could roll their own monitoring layers. A software‑native competitor could build a better platform. Regulators could stay toothless.

But the option exists. And today’s multiple charges basically nothing for it.

Moats Built From Bad Weather And Bureaucracy

Even if Genesis never escapes “nice add‑on” status, Thermon has a few unglamorous defenses.

First, certifications and scar tissue.

All those hazardous‑environment approvals — ATEX, IECEx, FM — represent decades wandering through refineries and petrochemical plants that regularly try to kill you.

Now, the “clean” frontier looks suspiciously similar. Hydrogen is leaky and explosive. Battery materials can be toxic and unstable. Carbon capture and synthetic fuels operate under harsh, unforgiving conditions.

The inconvenient reality for some ESG decks: the people who spent 40 years keeping crude and solvents from freezing or exploding are exactly the ones you need to keep hydrogen and exotic chemistries in line. Certification regimes do not move quickly, and field experience cannot be copy‑pasted.

There’s a plausible path from “oil & gas stigma discount” to “competence premium” as clean‑adjacent industries mature and regulators harden.

Second, MRO inertia.

Bears are right: maintenance spend is contestable, not contractually recurring. But the on‑the‑ground psychology matters.

Plant operators like single‑throat‑to‑choke vendors.

They hate surprises more than they love saving 15% on components.

Emergency logistics and support at 3 a.m. in terrible weather are hard to duplicate from halfway across the world.

The moat is not invincibility; it’s being the least risky phone call when things are going sideways.

Third, the installer/spec flywheel.

Heat tracing is installed by certified electricians and specialized contractors who get used to a particular vendor’s gear, controllers, and quirks.

More Thermon‑trained installers mean more comfort using Thermon gear.

More comfort means engineers spec Thermon more often by default.

More specs grow the installed base, which justifies more installers training on Thermon.

Management hasn’t fully weaponized this into a formal ecosystem strategy, but it quietly hums in the background.

None of these moats are heroic. But they are non‑zero — and they’re underappreciated next to the simplistic “duopoly vs. commoditization” debate.

Adults In Charge, Vision Optional

Thermon’s management team are solid operators, not prophets.

They’ve integrated acquisitions like Vapor Power without blowing up the balance sheet.

They’ve diversified away from pure upstream exposure.

They generally do what they say, with fewer “one‑time” excuses than many small caps.

Capital allocation has been boring, in a good way: small bolt‑ons, moderate leverage, no empire‑building.

Where they fall short is ambition around the assets that could change the company’s trajectory:

Seeing Genesis as a strategic platform, not brochureware.

Understanding that compliance, data, and software talent might matter as much as more sales reps.

Treating the installer/spec ecosystem as a network to cultivate, not a static channel.

That doesn’t kill the thesis. It just lowers the base probability that Thermon will unlock the “tollbooth” potential on its own, without a shove from the board or an acquirer who thinks in platforms instead of products.

The Distribution You’re Really Buying

To own THR, you’re implicitly buying a distribution of outcomes.

Base case:

Organic volumes grow low‑ to mid‑single digits.

Margins stay in the high‑teens/low‑20s EBITDA range.

M&A adds some growth but not magic.

Genesis is a helpful differentiator, not a separate profit engine.

At ~9–10x EBITDA, that supports something like 8–12% annualized returns over a 5‑year span, assuming no serious multiple compression and maybe a bit of re‑rating closer to peers.

Bull case:

Electrification and “clean‑adjacent” projects keep the order book healthy for a long time.

Thermon becomes a default choice for hazardous process heating in hydrogen, CCS, battery materials, LNG.

Genesis evolves into a real, high‑margin, monitoring and compliance platform, generating recurring revenue and raising switching costs.

Management (or an acquirer) leans into the software + regulation angle.

In that world, you could plausibly see faster growth, a richer multiple, and something closer to 20–25% IRRs.

Bear case:

Asian competition erodes pricing and share more than expected.

Replacement cycles stretch; project work gets sporadic; capex cycles turn against you.

M&A destroys value.

Regulation stays mushy; Genesis stalls at “nice-to-have dashboard” status.

There, you clip low single‑digit returns or worse, with downside amplified by multiple compression in a recessionary industrial downturn.

The current price doesn’t scream “mispriced,” but it does underwrite the base case while giving you a cheap call on the compliance upside — if you insist on buying with a margin of safety.

How To Hold A Ticket On The Quiet Optionality

If you want exposure here, you’re not betting on a miracle. You’re buying a functional industrial with hidden upside, and insisting on a price that pays you even if the upside never shows.

Three practical moves:

First, be price‑sensitive, not story‑sensitive.

Thermon is tied to industrial capex. When global growth wobbles, orders slow, and the stock sulks. That’s your friend.

The better entry is not when slides about “energy transition” are hot. It’s when:

A soft quarter or macro scare knocks the stock into the low‑20s.

Analysts complain about “order softness” and remind everyone it’s “just” a small‑cap industrial.

Around $22–25, the base‑case 8–12% IRR starts looking more like a floor, and the Genesis upside becomes close to free.

Second, size it like optionality, not conviction.

Too many externalities — regulation, competition, management’s software IQ — sit outside your control.

In a diversified portfolio, THR is a 2–3% position:

If the base case plays, it compounds quietly.

If the compliance tollbooth emerges, it punches above its weight.

If the bear case hits, it stings but doesn’t define your year.

Third, track the few signals that matter.

Don’t get hypnotized by every quarterly wobble. Watch:

Mix and margins: is MRO holding up? Are margins stable or creeping higher without obvious discounting?

Digital traction: do they start breaking out monitoring / software revenue? Is Genesis adoption discussed with real metrics instead of adjectives? Are they hiring software, data, and regulatory talent?

Regulatory drift: concrete moves in the EU, UK, US, or from major insurers that make continuous monitoring effectively mandatory in certain facilities.

Competitive chatter: any signs that major customers are pushing volume to cheaper certified rivals in a way that dents pricing power.

Finally, keep your exit discipline.

If, 3–5 years in, Genesis is still a footnote, organic volumes are flat, and pricing is under pressure, the thesis didn’t evolve. You collected your industrial returns; you didn’t get the tollbooth. Move on.

The real upside here is not faith in management’s storytelling. It’s the quiet asymmetry between what the market sees — a competent, slightly stigmatized hardware vendor — and what the world is drifting toward: industrial systems where the data exhaust is often more valuable than the steel.

Thermon’s pipes may stay boring. Its data stream doesn’t have to.